Meta Platforms: The $135 Billion Bet

Analyzing Zuckerberg’s massive infrastructure bet and the path to a $1.8 Trillion "AI Sovereign"

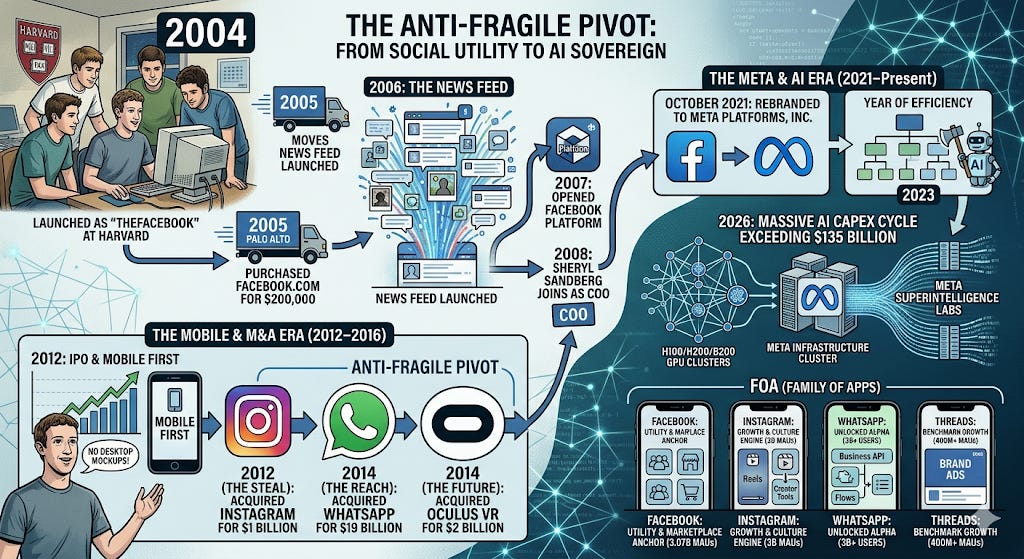

The Anti-Fragile Pivot

Few companies in history have been declared “dead” as often—and as prematurely—as Meta Platforms. From the 2012 mobile transition crisis to the 2022 $600 billion market cap “Dark Year,” Mark Zuckerberg has faced repeated existential threats, only to emerge with a more efficient and dominant machine. Today, Meta is no longer just a collection of social apps; it has evolved into an AI-driven arbitrage powerhouse. With a 2026 Capex cycle exceeding $135 billion, Zuckerberg is making the largest infrastructure bet in corporate history, aiming to pivot the company from a social utility to a “Sovereign AI” powerhouse. For the long-term compounder, the question is no longer whether people will keep scrolling, but whether Meta can successfully own the operating system of the next decade.

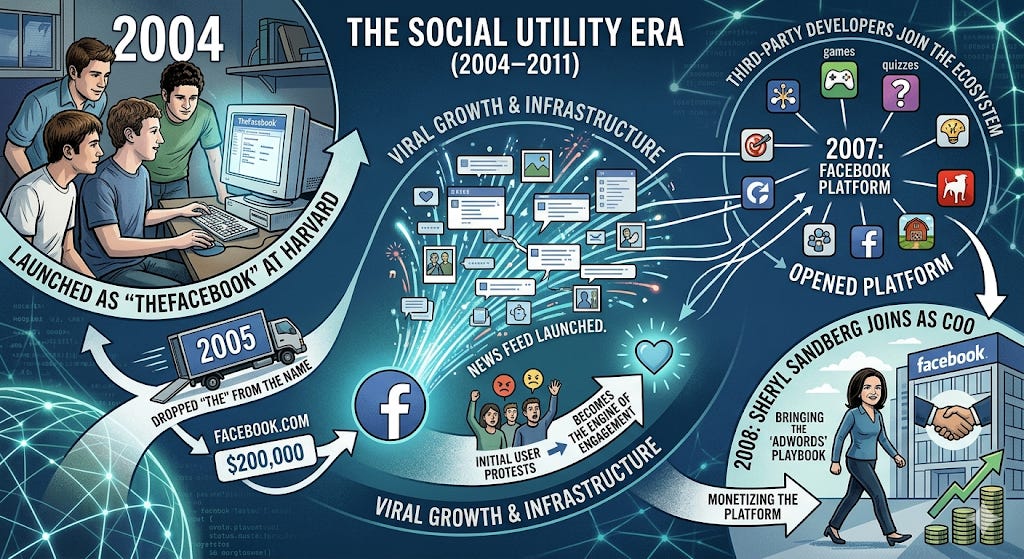

The Social Utility Era (2004–2011)

Theme: Viral Growth and Infrastructure.

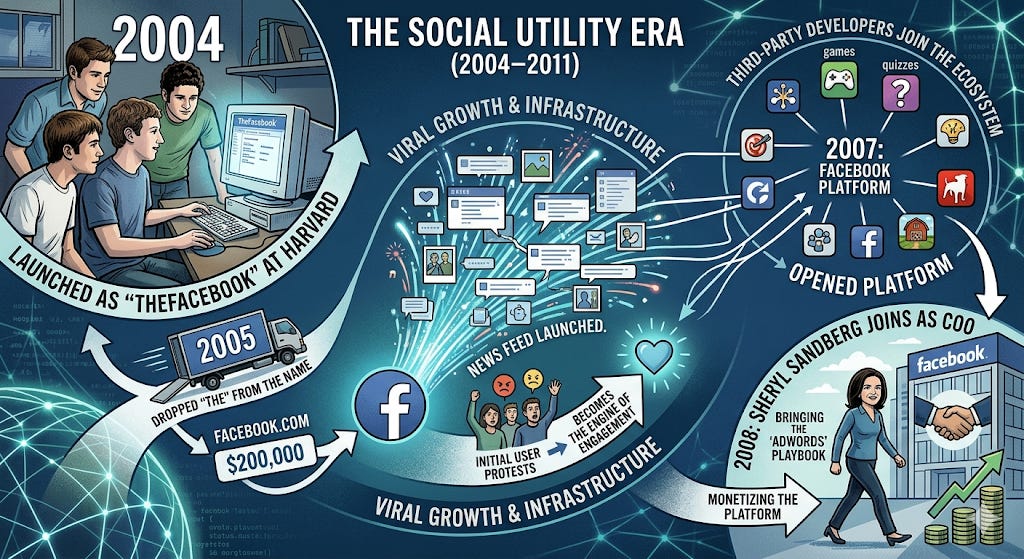

2004: Launched as “TheFacebook” at Harvard by Mark Zuckerberg, Eduardo Saverin, Dustin Moskovitz, and Chris Hughes. It quickly expanded to the Ivy League and moved to Palo Alto.

2005: Dropped “The” from the name (purchased facebook.com for $200,000).

2006: The “Big Bang” of social media: The News Feed launched. Initially hated by users for privacy reasons, it became the engine of engagement.

2007: Zuckerberg opened the Facebook Platform, allowing third-party developers (like Zynga) to build apps on top of Facebook.

2008: Sheryl Sandberg joined as COO from Google, bringing the “AdWords” playbook to monetize the platform.

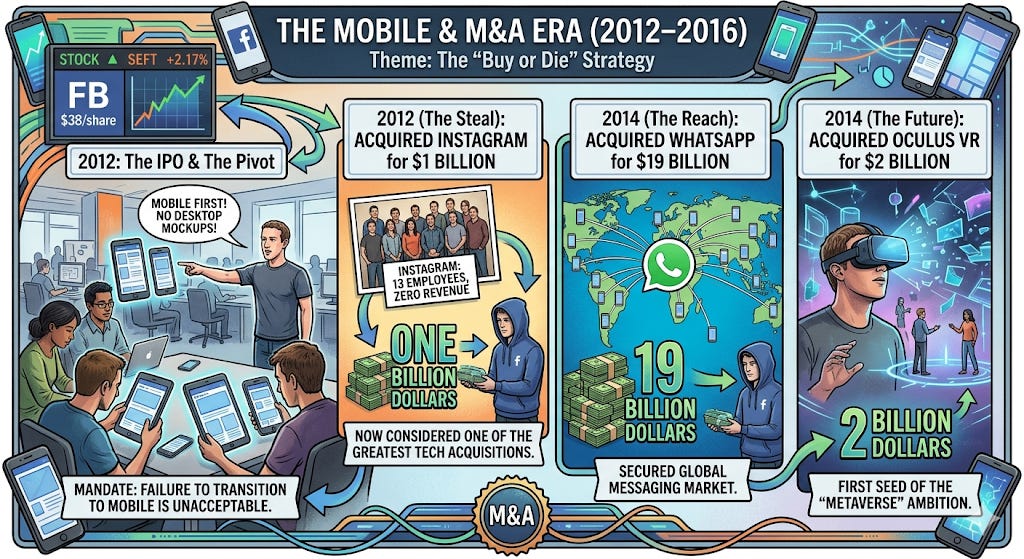

The Mobile & M&A Era (2012–2016)

Theme: The “Buy or Die” Strategy.

2012: The IPO & The Pivot. Facebook went public at $38/share. Simultaneously, Zuckerberg realized the company was failing the transition to mobile. He famously ordered a “Mobile First” mandate, where engineers couldn’t show him desktop mockups.

2012 (The Steal): Acquired Instagram for $1 billion. At the time, it had 13 employees and zero revenue. It is now considered one of the greatest acquisitions in tech history.

2014 (The Reach): Acquired WhatsApp for $19 billion. This secured the global messaging market.

2014 (The Future): Acquired Oculus VR for $2 billion, the first seed of the “Metaverse” ambition.

The Regulatory & Crisis Era (2017–2020)

Theme: Platform Responsibility and Antitrust.

2018: The Cambridge Analytica scandal broke, revealing that data from 87 million users was harvested for political profiling. Zuckerberg testified before Congress.

2019: The FTC hit Facebook with a record $5 billion fine for privacy violations.

2020: The “Year of Efficiency” predecessor: Despite the pandemic, the company faced a massive advertiser boycott (#StopHateForProfit) and increasing competition from TikTok.

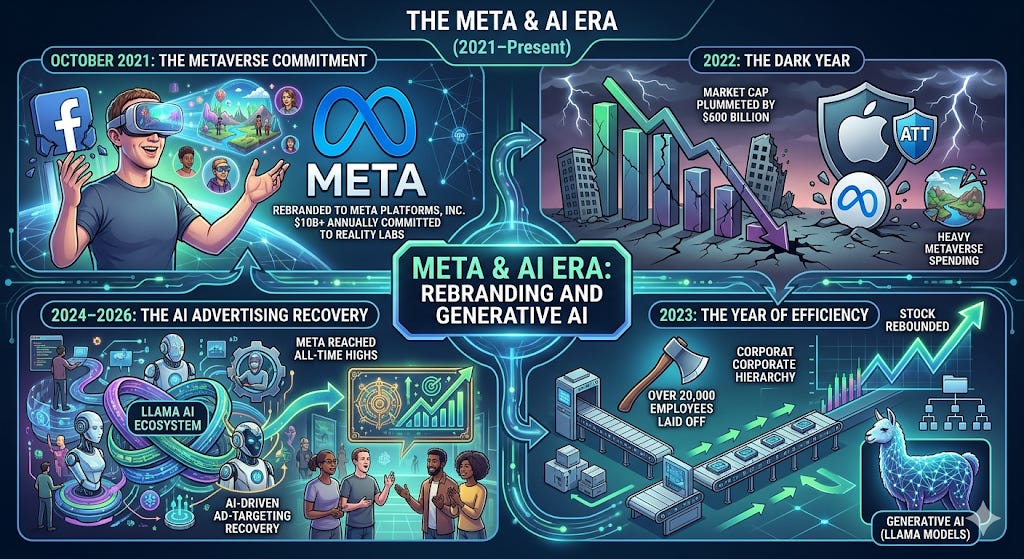

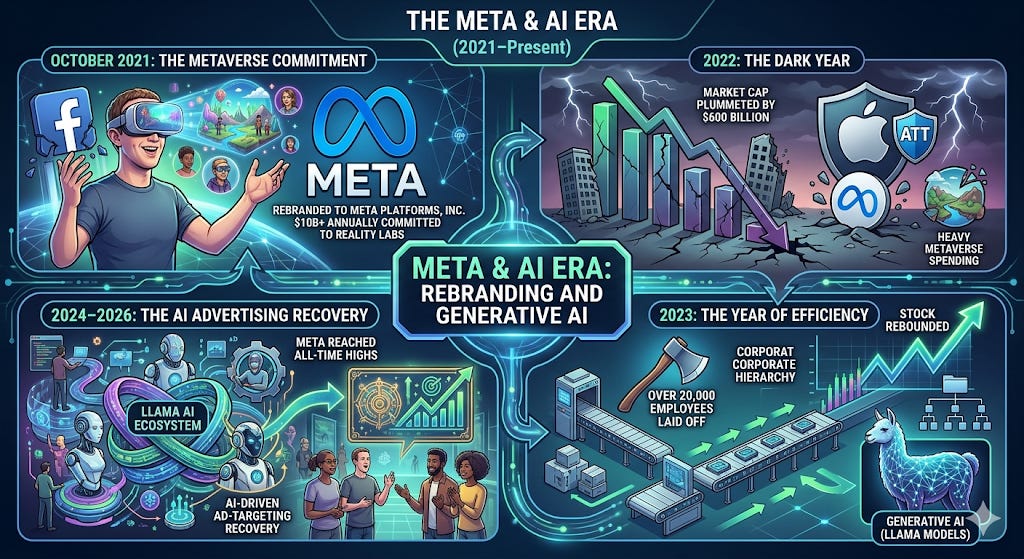

The Meta & AI Era (2021–Present)

Theme: Rebranding and Generative AI.

October 2021: Facebook rebranded to Meta Platforms, Inc. Zuckerberg committed $10B+ annually to “Reality Labs” to build the Metaverse.

2022: The “Dark Year.” Meta’s market cap plummeted by $600 billion due to Apple’s privacy changes (ATT) and heavy Metaverse spending.

2023: The Year of Efficiency. Meta laid off over 20,000 employees. The stock rebounded as the company pivoted its narrative toward Generative AI (Llama models).

2024–2026: Meta reached all-time highs, driven by its Llama AI ecosystem and the massive success of its AI-driven ad-targeting recovery.

The Core Engine: “Family of Apps” (FoA)

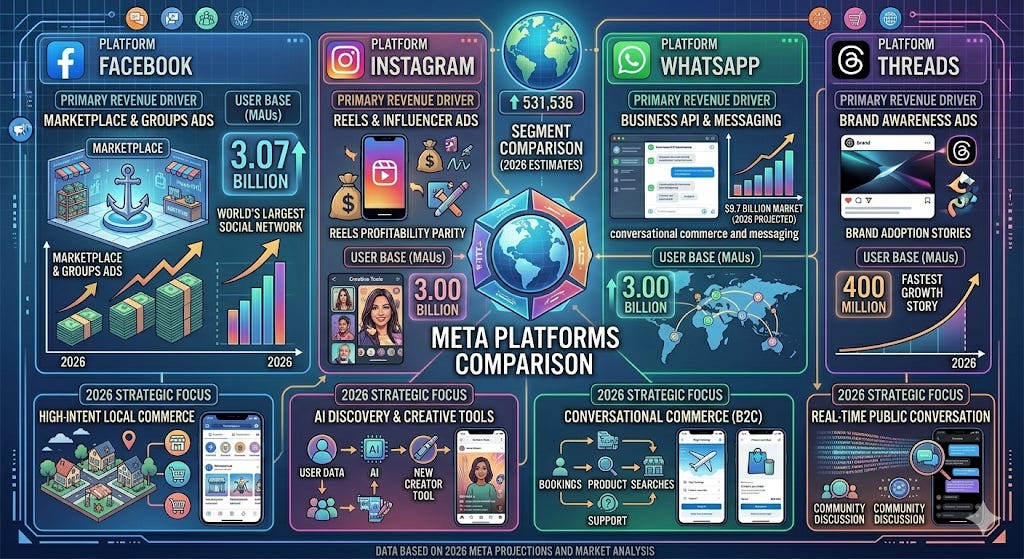

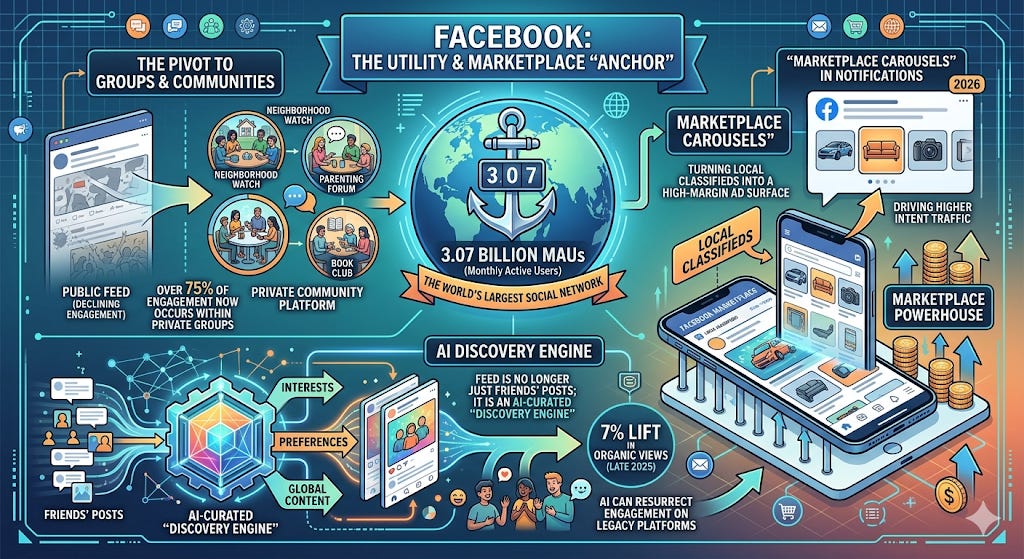

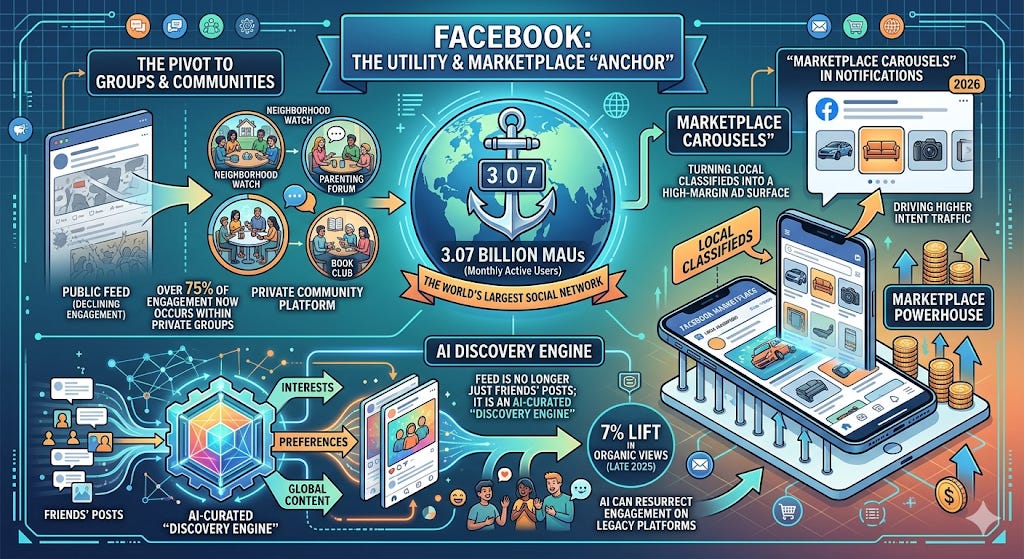

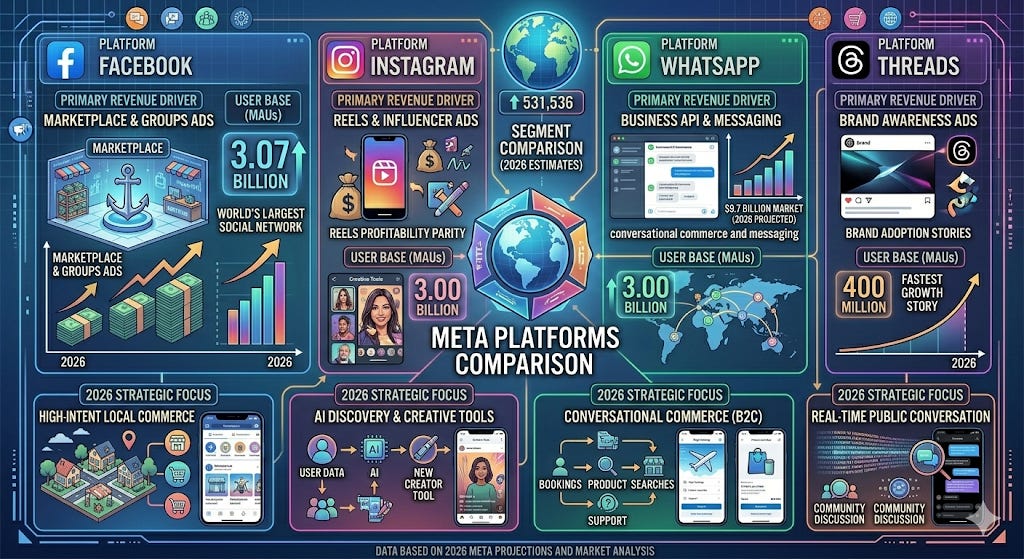

Facebook: The Utility & Marketplace “Anchor”

Despite perennial “Facebook is dead” narratives, it remains the world’s largest social network with 3.07 billion Monthly Active Users (MAUs).

The Pivot to Groups & Communities: Meta has successfully transitioned Facebook from a “Public Feed” (where engagement was declining) to a “Private Community” platform. Over 75% of engagement now occurs within private Groups.

The Marketplace Powerhouse: Facebook Marketplace is now a top-tier e-commerce destination globally. In 2026, Meta began testing “Marketplace Carousels” in notifications to drive higher intent traffic, turning local classifieds into a high-margin ad surface.

AI Discovery Engine: Facebook’s feed is no longer just your friends’ posts; it is an AI-curated “Discovery Engine.” This shift led to a 7% lift in organic views in late 2025, proving that AI can resurrect engagement on legacy platforms.

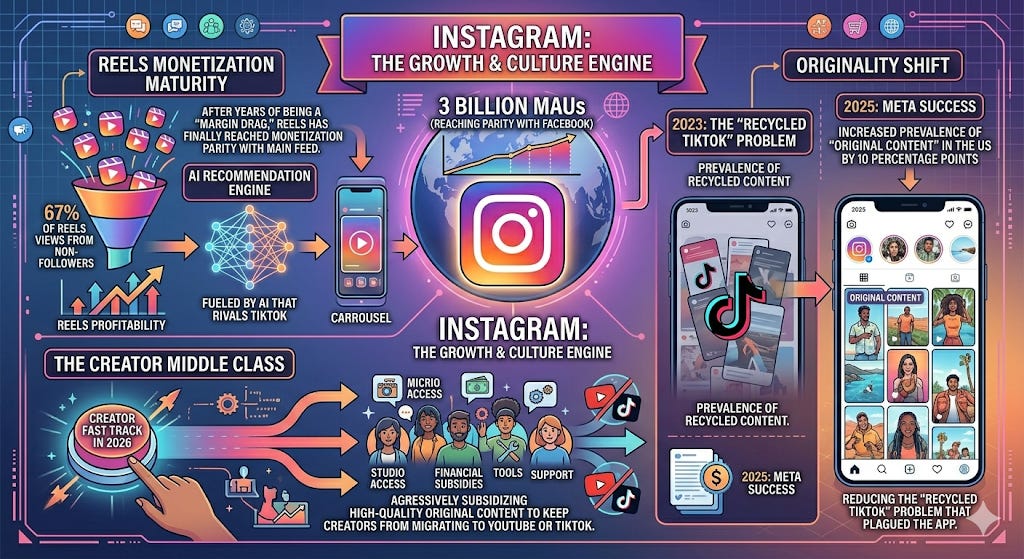

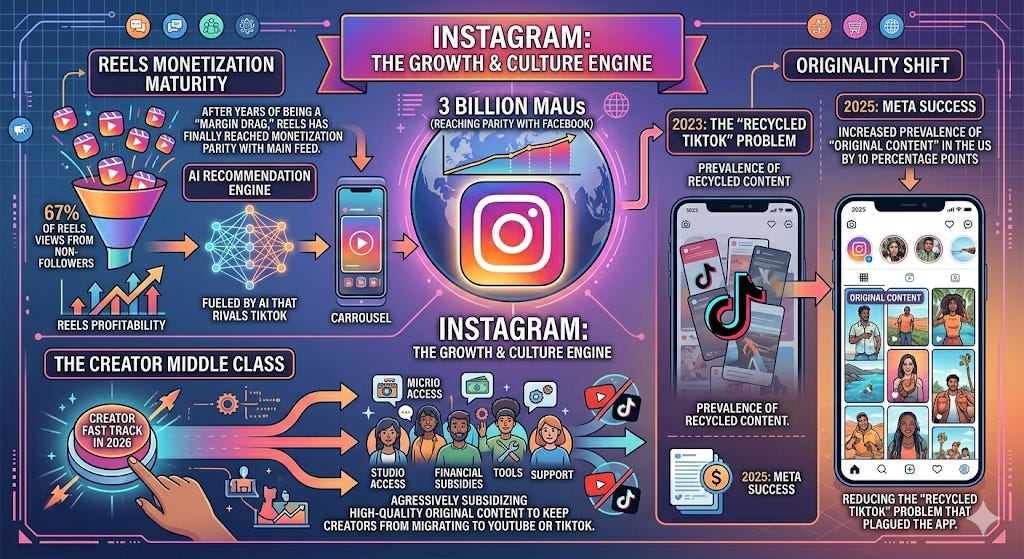

Instagram: The Growth & Culture Engine

Instagram is the primary driver of Meta’s current valuation. It recently hit 3 billion MAUs, reaching parity with Facebook.

Reels Monetization Maturity: After years of being a “margin drag,” Reels has finally reached monetization parity with the main Feed. 67% of Reels views now come from non-followers, fueled by an AI recommendation engine that rivals TikTok.

The Creator Middle Class: With the launch of Creator Fast Track in 2026, Meta is aggressively subsidizing high-quality original content to keep creators from migrating to YouTube or TikTok.

Originality Shift: Meta successfully increased the prevalence of “original content” in the US by 10 percentage points in 2025, reducing the “recycled TikTok” problem that plagued the app in 2023.

WhatsApp: The Unlocked “Alpha”

WhatsApp is the most under-monetized asset in the portfolio, but that is changing rapidly in 2026. It currently has over 3 billion users.

Conversational Commerce: The WhatsApp Business API is the star of the 2026 growth story. It is projected to be a $9.7 billion market this year, growing at a 20.7% CAGR.

The “Service Concierge”: Through “WhatsApp Flows,” businesses now conduct entire customer journeys—booking a flight, buying insurance, or tracking a package—without the user ever leaving the chat.

Click-to-Message Ads: This is Meta’s fastest-growing ad format. Instead of a traditional “website click,” ads lead directly to a WhatsApp chat. This is seeing massive adoption in India, Brazil, and Indonesia, where WhatsApp is effectively the “OS” of the internet

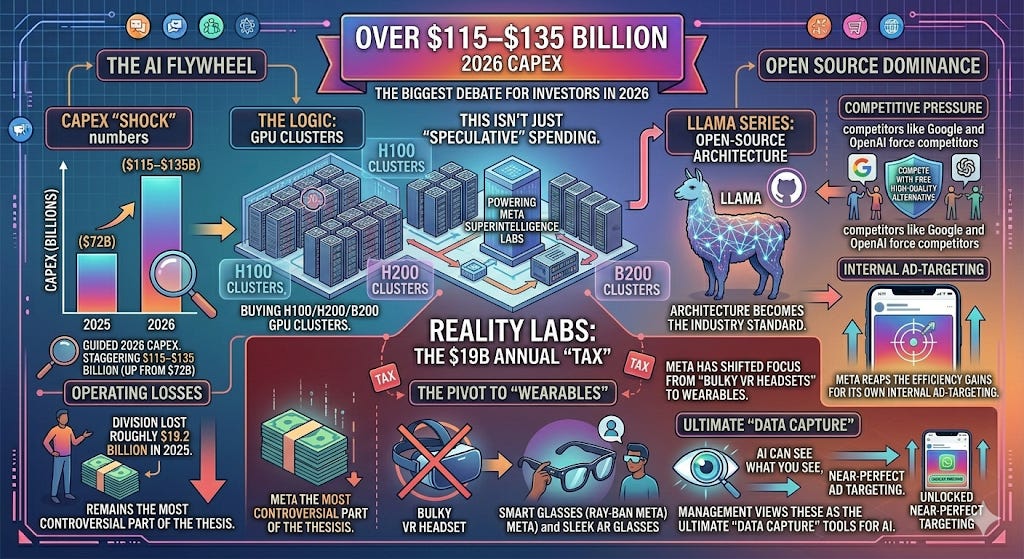

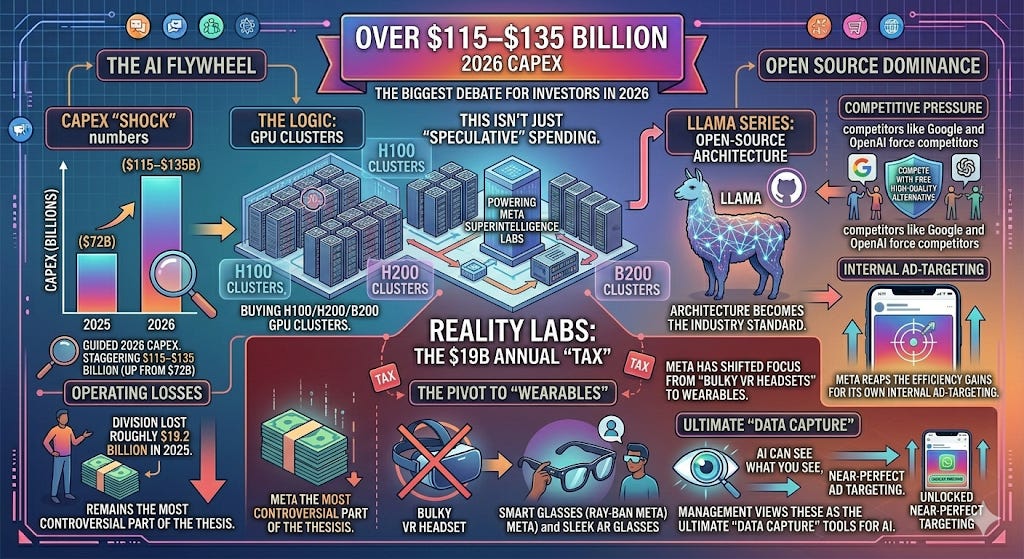

The AI Flywheel & Capex “Shock”

The biggest debate for investors in 2026 is Meta’s massive capital expenditure.

The Numbers: Meta has guided 2026 Capex to a staggering $115–$135 billion (up from $72B in 2025).

The Logic: This isn’t just “speculative” spending. This capital is buying H100/H200/B200 GPU clusters to power Meta Superintelligence Labs.

Open Source Dominance: By releasing the Llama series as open-source, Meta has effectively made its architecture the industry standard for developers, forcing competitors like Google and OpenAI to compete with a “free” high-quality alternative while Meta reaps the efficiency gains for its own internal ad-targeting.

Reality Labs: The $19B Annual “Tax”

Reality Labs (VR/AR) remains the most controversial part of the thesis.

Operating Losses: The division lost roughly $19.2 billion in 2025.

The Pivot to “Wearables”: Meta has shifted focus from “bulky VR headsets” to smart glasses (Ray-Ban Meta) and sleek AR glasses. Management views these as the ultimate “data capture” tools for AI—if the AI can see what you see, the ad targeting becomes near-perfect.

The “Threads” Factor

Don’t ignore Threads. It surpassed 400 million MAUs in Q1 2026. Meta has officially rolled out ads to the platform globally, and it is benefiting from a 20% lift in time spent due to deep integration with the Instagram ecosystem.

Key Takeaway: The “Family of Apps” is no longer just about social connection. It is an AI-driven arbitrage machine. Meta uses the massive data from 3.9+ billion unique people (across all apps) to train its Llama models, which then serve better ads, creating a compounding loop that competitors with smaller data sets simply cannot match.

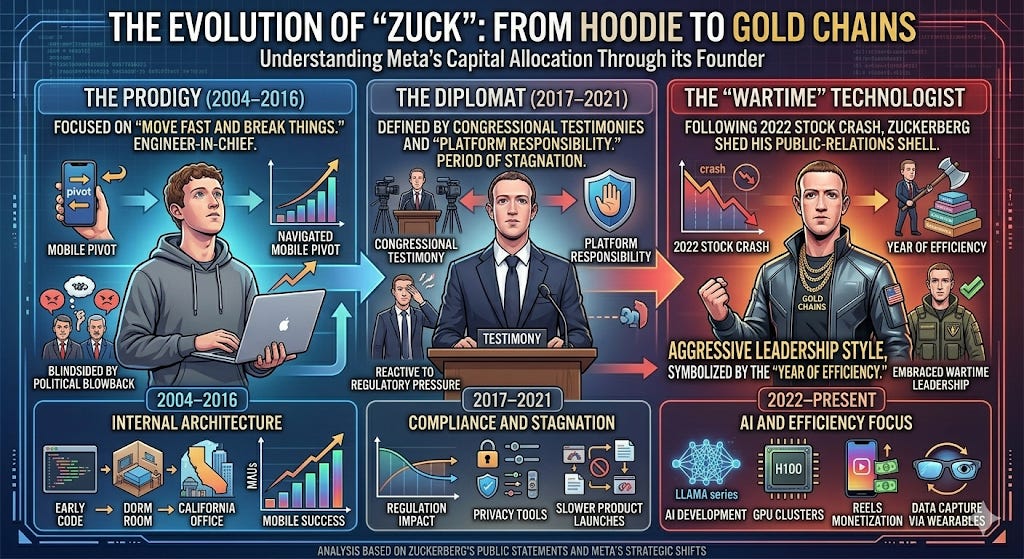

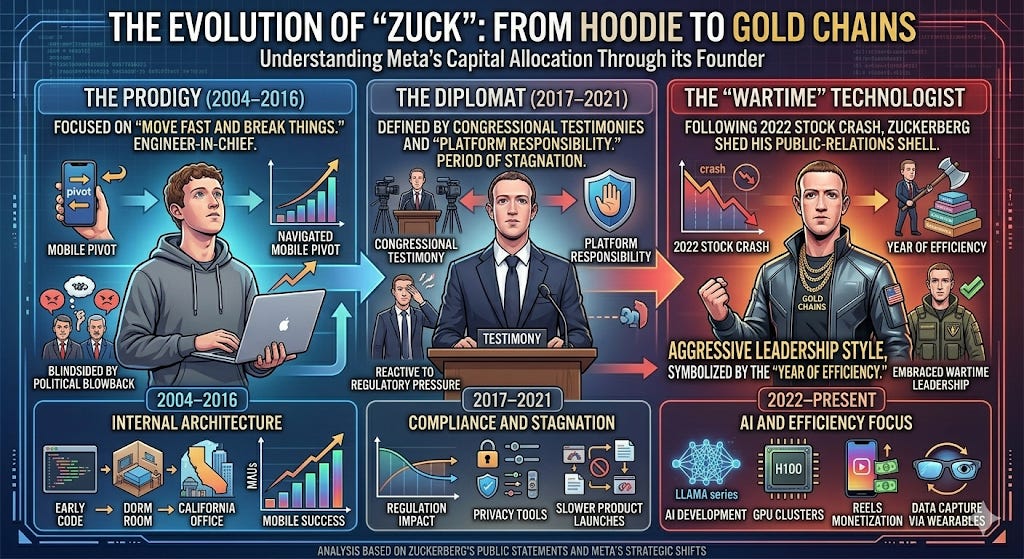

The Evolution of “Zuck”: From Hoodie to Gold Chains

To understand Meta’s capital allocation, you must understand the three distinct versions of its founder:

The Prodigy (2004–2016): Focused on “Move Fast and Break Things.” He was the engineer-in-chief who successfully navigated the mobile pivot but was blindsided by the political blowback of the late 2010s.

The Diplomat (2017–2021): Defined by congressional testimonies and “Platform Responsibility.” This was a period of stagnation where Zuckerberg appeared reactive to regulatory pressure.

The “Wartime” Technologist (2022–Present): Following the 2022 stock crash, Zuckerberg shed his public-relations shell. He embraced a more aggressive, leadership style, symbolized by the “Year of Efficiency.” He has stopped apologizing for Meta’s dominance and started leaning into it.

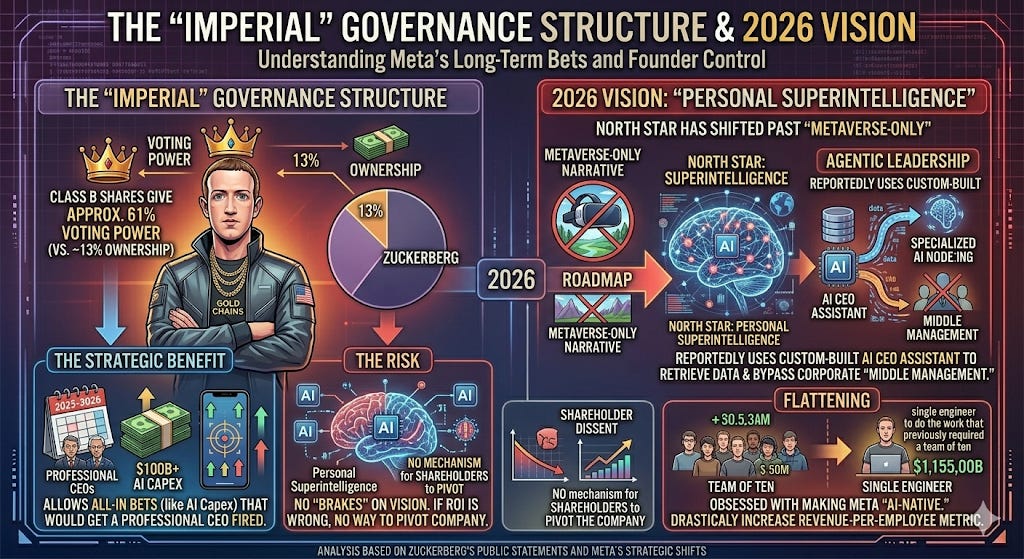

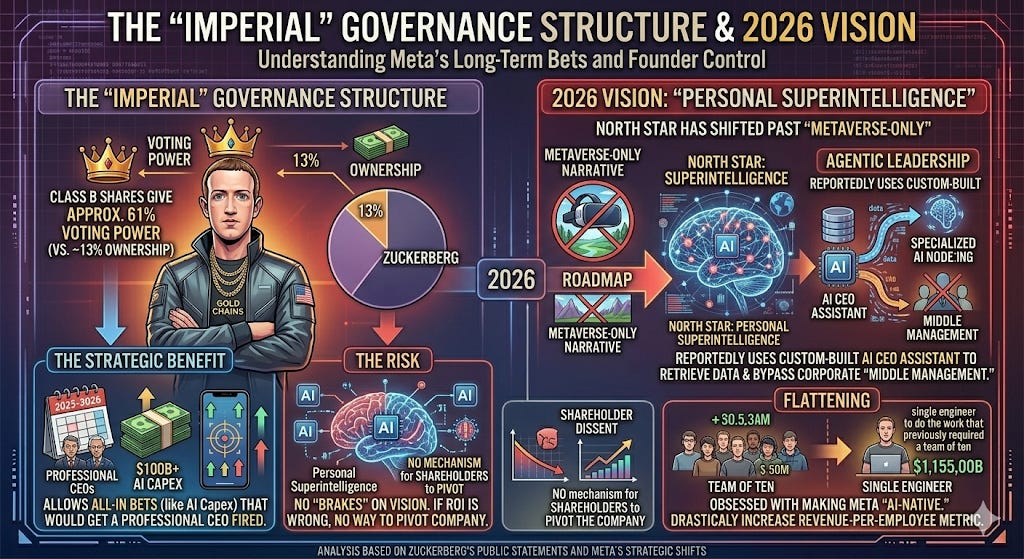

The “Imperial” Governance Structure

Zuckerberg holds Class B shares, giving him roughly 61% of the voting power despite owning only about 13% of the company.

The Strategic Benefit: This allows him to make “all-in” bets (like the $100B+ AI Capex in 2025-2026) that would get a professional CEO fired.

The Risk: There are no “brakes” on his vision. If he is wrong about the ROI of “Personal Superintelligence,” there is no mechanism for shareholders to pivot the company.

2026 Vision: “Personal Superintelligence”

In his 2026 roadmap, Zuckerberg has moved past the “Metaverse-only” narrative. His new North Star is Personal Superintelligence.

Agentic Leadership: Zuckerberg is reportedly using his own custom-built AI CEO Assistant to retrieve data and bypass corporate “middle management.”

The “Flattening”: He is obsessed with using AI to make Meta “AI-native.” His goal is to allow a single engineer to do the work that previously required a team of ten, drastically increasing the revenue-per-employee metric.

Political & Cultural Realignment

In a significant shift for 2025–2026, Zuckerberg has moved Meta away from Silicon Valley’s typical DEI (Diversity, Equity, and Inclusion) and social-justice-focused corporate culture.

The “Neutral” Pivot: He has positioned Meta as a more politically neutral utility, focusing on “meritocracy” (his own words from a 2025 podcast).

Government Relations: Under his leadership, Meta has aggressively courted government partnerships for its Meta Compute infrastructure, positioning Llama as the “American Open Source” alternative to state-controlled AI from rivals.

The $135B Question: Infrastructure or Excess?

Meta’s 2026 Capex guidance represents a nearly 88% increase from its 2025 spend ($72B). To put this in perspective, Meta is spending more on hardware and data centers this year than the entire market cap of most S&P 500 companies.

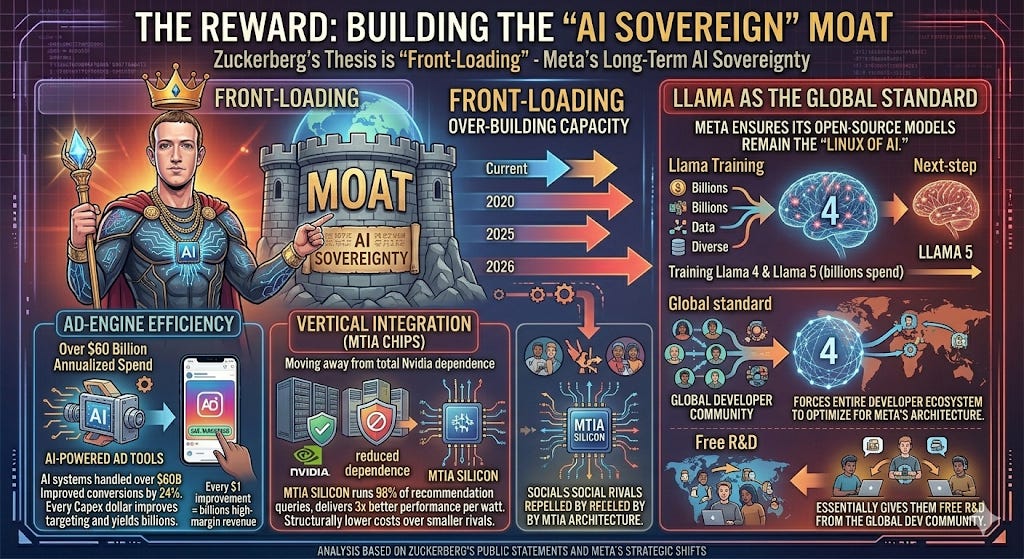

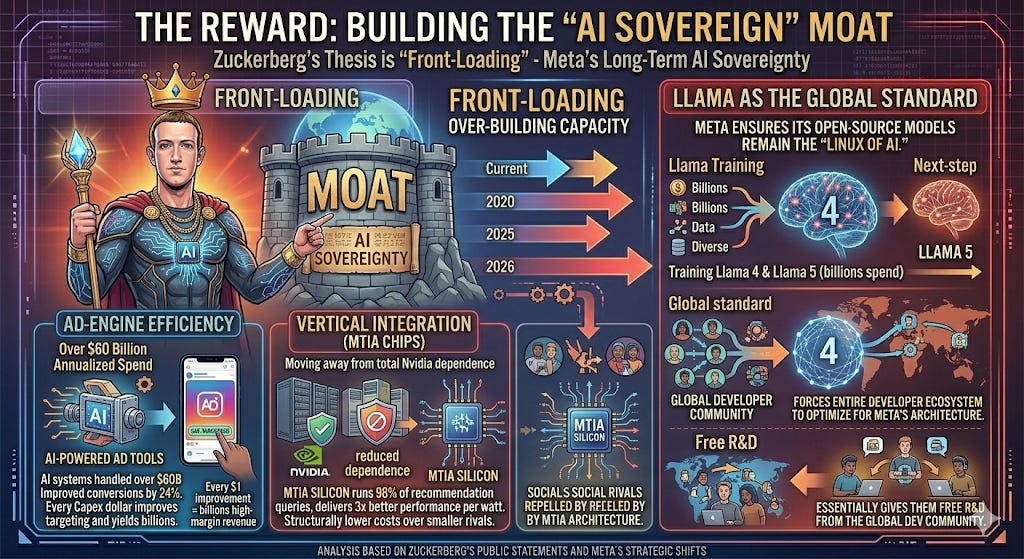

The Reward: Building the “AI Sovereign” Moat

Zuckerberg’s thesis is “Front-Loading.” By over-building capacity now, Meta aims to reach Personal Superintelligence before its peers.

Ad-Engine Efficiency: AI-powered ad tools already handle over $60 billion in annualized spend. In 2025, these systems improved conversions by 24%. Every dollar of Capex that improves ad-targeting by even 1% yields billions in high-margin revenue.

Vertical Integration (MTIA Chips): Meta is moving away from total Nvidia dependence. Its MTIA (Meta Training and Inference Accelerator) silicon now runs 98% of recommendation queries, delivering 3x better performance per watt. This creates a structural cost advantage over smaller social rivals.

Llama as the Global Standard: By spending billions to train Llama 4 (and the upcoming Llama 5), Meta ensures its open-source models remain the “Linux of AI.” This forces the entire developer ecosystem to optimize for Meta’s architecture, essentially giving them free R&D from the global dev community.

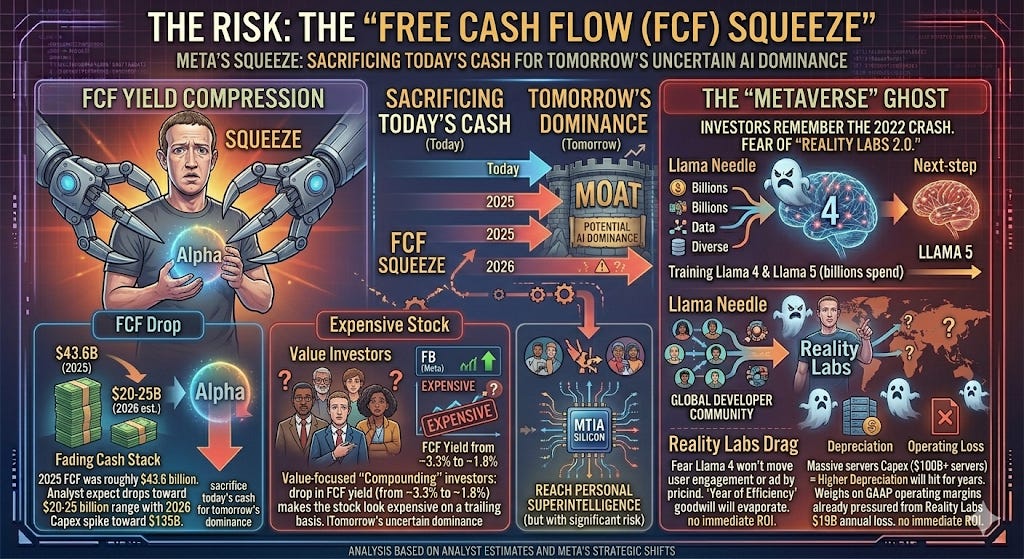

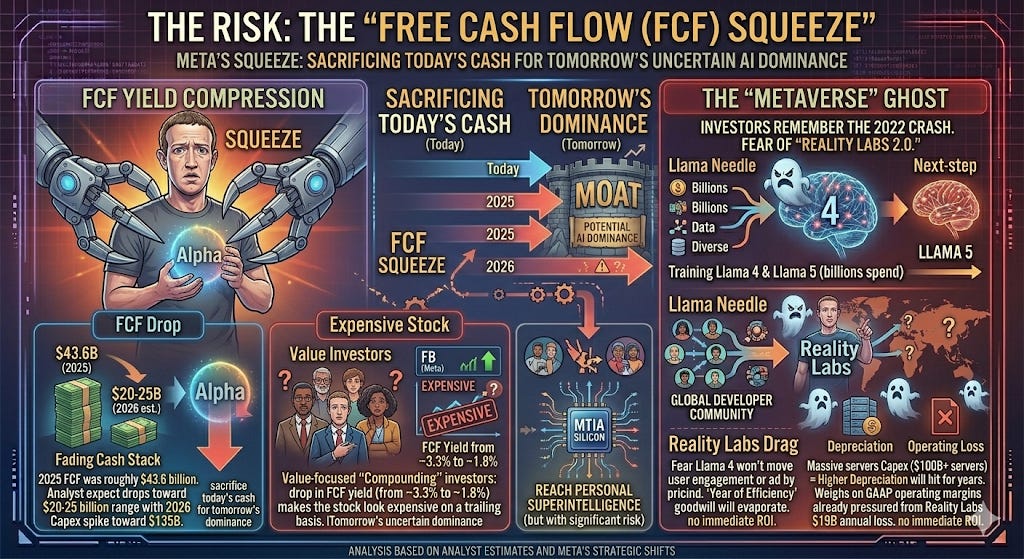

The Risk: The Free Cash Flow Squeeze

The primary “Alpha” risk is that Meta is sacrificing today’s certain cash for tomorrow’s uncertain dominance.

FCF Yield Compression: In 2025, Meta’s FCF was roughly $43.6 billion. With 2026 Capex spiking toward $135B, analysts expect FCF to drop significantly—potentially to the $20–$25 billion range. For value-focused “Compounding” investors, this drop in FCF yield (from ~3.3% to ~1.8%) makes the stock look expensive on a trailing basis.

The “Metaverse” Ghost: Investors remember the 2022 crash. There is a lingering fear that “Superintelligence Labs” is just “Reality Labs 2.0”—a black hole for cash with no immediate ROI. If Llama 4 doesn’t significantly move the needle on user engagement or ad pricing by year-end, the “Year of Efficiency” goodwill will evaporate.

Depreciation Drag: This massive Capex won’t just hit cash; it will hit the income statement for years. Higher depreciation from $100B+ in servers will weigh on GAAP operating margins, which are already feeling pressure from Reality Labs’ $19B annual loss.

The takeaway is that Meta is re-investing nearly all its profits into a single bet. If Zuckerberg is right, Meta owns the “operating system” of the 2030s. If he is wrong, Meta has built the world’s most expensive collection of rapidly depreciating H100 GPUs. Currently, the market is giving him the benefit of the doubt because Operating Income is still guided to grow in 2026 despite the spend—a feat few other companies could manage.

Research Tip: Watch the “Revenue per Employee” metric. If Meta can keep this rising while spending $100B+ on AI, the “Efficiency” story is still alive. If it dips, the “Empire Building” risks have returned.

Financial Analysis: The Efficiency Machine

Meta’s financial statements tell a story of anti-fragility. After a significant dip in 2022, the company has re-engineered its cost structure while simultaneously hitting record revenue levels.