The Alpha in PGR: Why Progressive is the Ultimate Compounding Engine

From "Un-insurable" niches to market dominance—mapping the financial mechanics behind the world’s most disciplined underwriter.

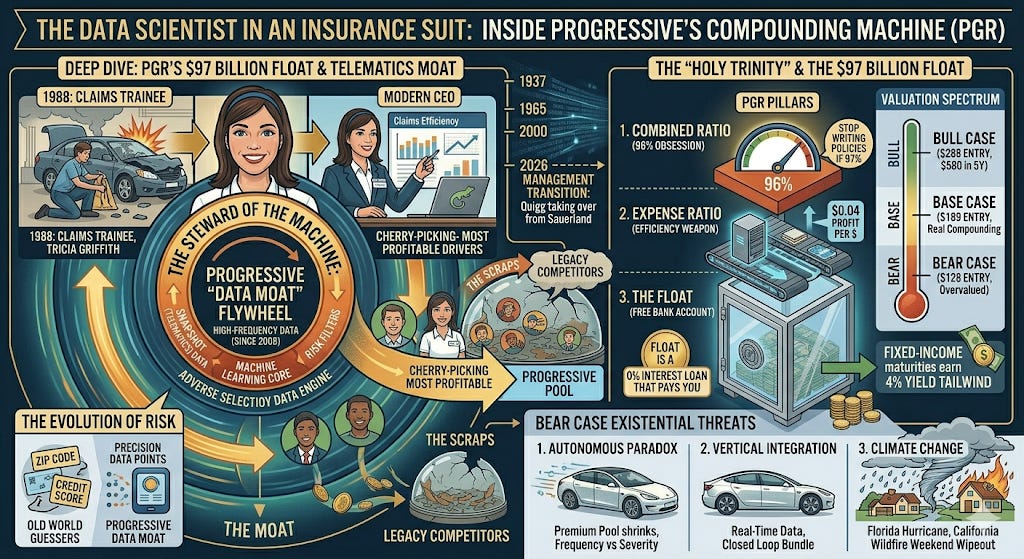

The Data Scientist in an Insurance Suit

Most investors view the insurance industry as a stagnant, commoditized pond where giants like State Farm and GEICO fight over pennies in the mud. They see a “boring” sector defined by television mascots and price-matching wars. They are missing the greatest compounding machine of the last 30 years.

Progressive (PGR) is not just an insurance company. It is a high-frequency data engine that happens to underwrite risk. While competitors were relying on archaic proxies like zip codes and credit scores, Progressive spent the last two decades building a “Data Moat” so deep that it has turned the traditional insurance model on its head.

Through a religious—almost fanatical—obsession with a 96% Combined Ratio, Progressive has mastered the art of “Adverse Selection”: cherry-picking the most profitable drivers and leaving the “scraps” for everyone else. With the company recently overtaking GEICO for the #2 spot in the U.S. and a management team that has been in the trenches since the 1980s, we are looking at a business that is hitting its stride just as interest rates provide a massive tailwind to its $97 billion float.

In this deep dive, we strip back the curtain on the “Holy Trinity” of Progressive’s financials, analyze the existential threat of autonomous vehicles, and run the numbers through our proprietary DCF models to see if the current price offers a margin of safety for the long-term compounder.

The Progressive Evolution: A Strategic Timeline

Progressive’s history is defined by three distinct eras: the Niche Specialist (1937–1965), the Lewis Era of Profitability (1965–2000), and the Digital & Data Powerhouse (2000–Present).

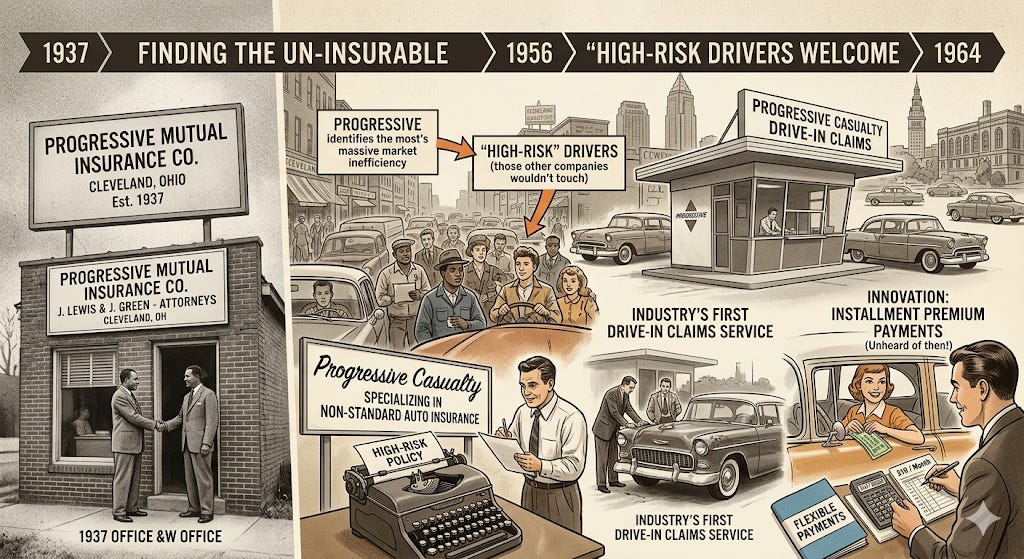

The Early Years: Finding the “Un-insurable” (1937–1964)

1937: Attorneys Joseph Lewis and Jack Green found Progressive Mutual Insurance Company in Cleveland, Ohio, with just $10,000 in capital.

1956: The company identifies a massive market inefficiency: “high-risk” drivers. They form Progressive Casualty specifically to write “non-standard” auto insurance—drivers other companies wouldn’t touch.

Innovation Highlight: They introduce the industry’s first drive-in claims service and allow customers to pay premiums in installments (unheard of at the time).

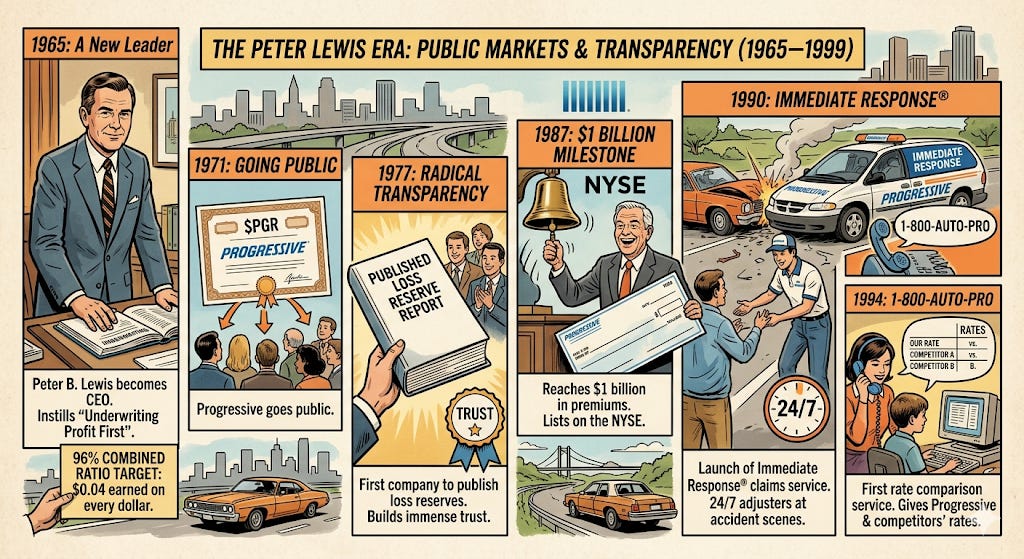

The Peter Lewis Era: Public Markets & Transparency (1965–1999)

1965: Peter B. Lewis (son of the founder) becomes CEO. He instills the “Underwriting Profit First” mantra, aiming for a 96% Combined Ratio (earning $0.04 on every dollar before investment income).

1971: Progressive goes public ($PGR).

1977: In a move toward radical transparency, Progressive becomes the first company to publish its loss reserve reports, building immense trust with analysts and shareholders.

1987: Progressive reaches $1 billion in premiums and lists on the NYSE.

1990: Launch of Immediate Response® claims service—24/7 support that sent adjusters directly to accident scenes in branded vehicles (the “IRVs”).

1994: Launch of 1-800-AUTO-PRO, the first service to give customers Progressive’s rates alongside those of their competitors.

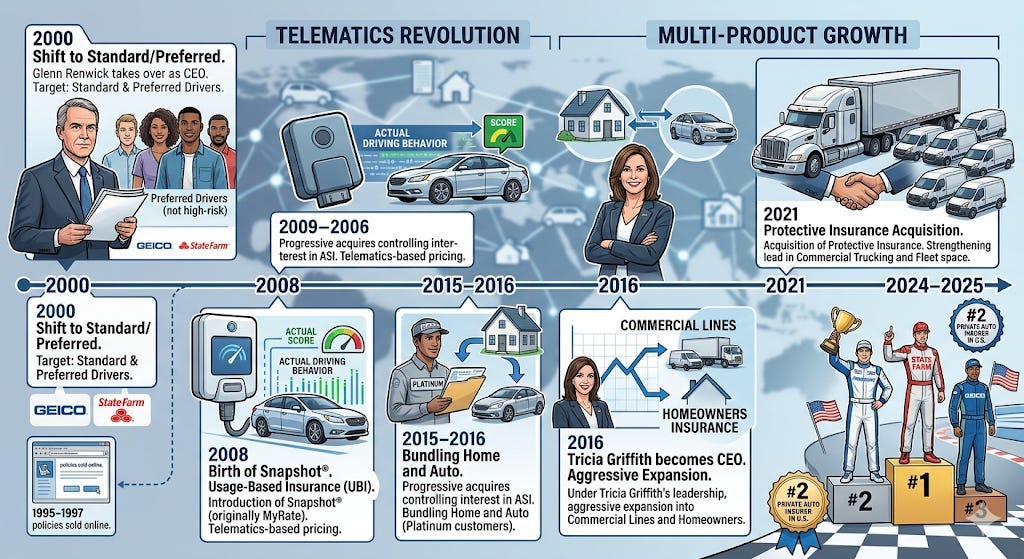

The Modern Era: Telematics & Multi-Product Growth (2000–Present)

1995–1997: Progressive becomes the first major insurer to launch a website and the first to sell policies online in real-time.

2000: Glenn Renwick takes over as CEO. The company shifts focus toward “Standard” and “Preferred” drivers to compete with GEICO and State Farm.

2008: Introduction of Snapshot® (originally MyRate). This marks the birth of Usage-Based Insurance (UBI), using telematics to price risk based on actual driving behavior rather than just demographics.

2015–2016: Progressive acquires a controlling interest in ASI (American Strategic Insurance), allowing them to bundle Home and Auto—a key move to increase customer retention (”Platinum” customers).

2016: Tricia Griffith becomes CEO. Under her leadership, the company aggressively expands into Commercial Lines and Homeowners insurance.

2021: Acquisition of Protective Insurance, strengthening their lead in the commercial trucking and fleet space.

2024–2025: Progressive overtakes GEICO to become the #2 private auto insurer in the U.S., trailing only State Farm.

The Holy Trinity of Progressive’s Printing Press

In the insurance world, most companies are “Asset Managers in Disguise.” They break even on their customers and hope the stock market goes up so they can make money on the “Float.”

Progressive is different.