The Case for $285 Uber

Why the market is mispricing the world’s most dominant mobility network in the face of the autonomous revolution.

The market is currently pricing Uber as if it is a legacy business about to be disrupted by autonomous vehicles. In reality, Uber has transformed into an expanding toll bridge for global mobility with a massive free cash flow inflection that is just beginning.

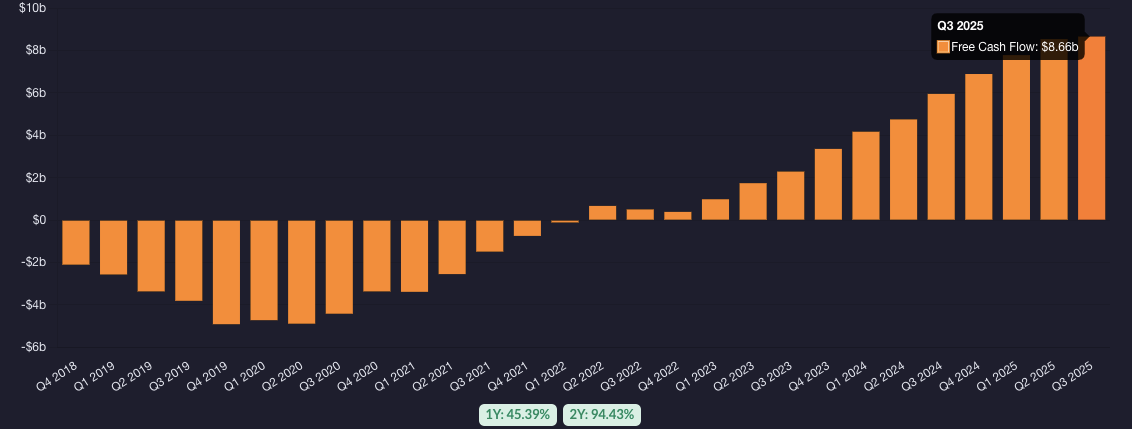

Uber has evolved from losing nearly $1B in a single quarter (2017) to generating $8B in Free Cash Flow over the last 12 months.

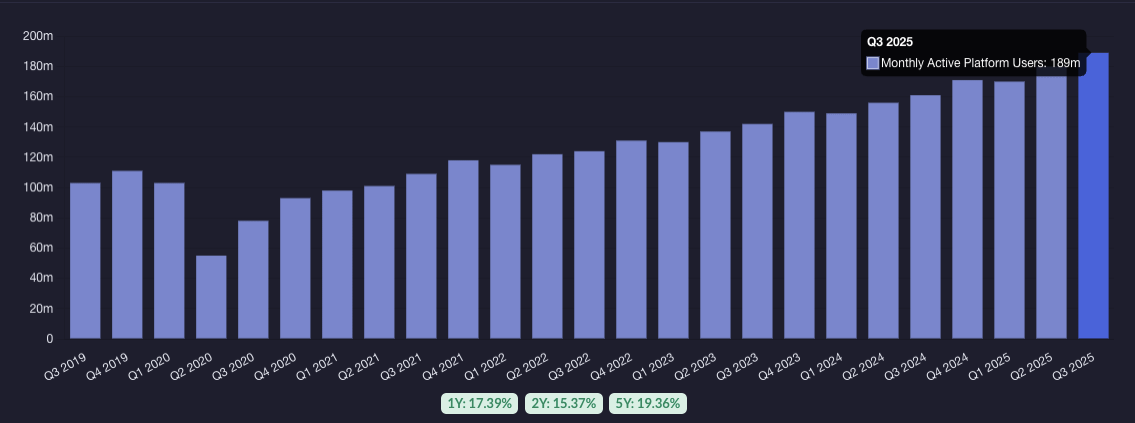

Rather than being disrupted, Uber’s 189M monthly user network makes them the indispensable partner for autonomous players who lack consumer scale.

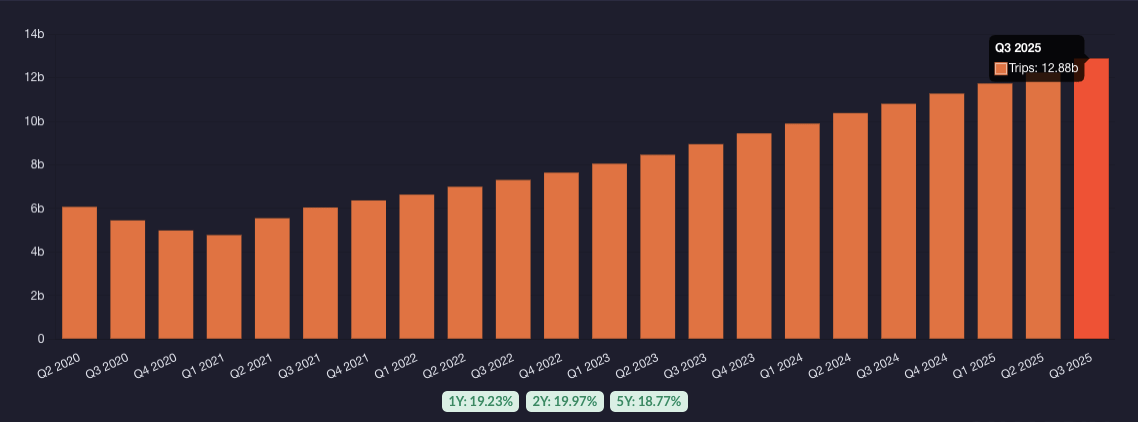

With 12 billion annual trips, a simple $0.50 price increase per trip flows $6B directly to the bottom line representing a massive untapped margin lever.

Currently trading at 20x FCF with 18% revenue growth.

My base case projects a $285 share price within 5 years, representing a 28% annual return.

20 years ago when you finished your day, and left your high profile business meeting in downtown New York, you went outside and waited for the yellow cab. Unbeknownst to the yellow cab operators in 2009 something would change forever.

Co-founder Travis Kalanick had spent $800 hiring a private driver on New Year’s Eve. Later that year the first prototype of Uber’s app was developed lead by other co-founder Garrett Camp. In May of 2010 a beta of Uber launched, in December of 2010 Kalanick took over as CEO of Uber, and in the following year Uber was open to the public in San Francisco.

From here one might say the rest is history gone are the days of flagging down the cab driver and here are the days of having your Uber booked and waiting for you when you get downstairs.

When Uber first launched it was a luxury platform. Always a black luxary car and the cost typically being 1.5x that of a standard taxi. Over the years Uber has launched many different services, with notable ones such as UberX a service allowing drivers to use standard vehicles with more competitive rates compared to traditional taxis, and UberEats a food delivery service.

By 2017 when then CEO of Expedia Dara Khosrowshahi took over at Uber. It was already a global company well known by consumers and growing fast. The problems came from questions about the companies profitability and legal issues.

When expanding to new cities Uber sometimes began operations without any regard for local regulations. If faced with regulatory opposition, Uber called for public support for its service and mounted political campaigns. Coupled with the issues of low driver pay, and insurance costs, Uber at the time was justifiable in the crosshairs of regulators. Since taking over Dara has done a great job of keeping Uber out of these negative headlines. Although you may still see articles of low driver pay, gone are the days of Uber playing bully ball and ignoring local regulation.

As far as profitability in Q1 of 2017 Uber was hemorrhaging money the company had a net income of -$927 million for the trailing 12 months. Many experts were left wondering if the company would even survive. Fast forward 8 years past ZIRP era financing, a successful IPO, a global pandemic, and a rate hiking cycle. Uber is generating $16 Billion of net income now over the last year, leaving little doubt over the companies business model. One might say Dara has done alright here as well.

Today the risks have shifted from profitability concerns, to automated copy cats. With companies like Waymo, and Tesla showcasing automated ride sharing capabilities Mr. Market is starting to question if Uber’s ride sharing network is here to stay. With Uber worth nearly $170 Billion today, I will be laying out the investment case for Uber to rebuke these automated concerns and potentially offer a 25%+ IRR well into the future.

Autonomous Vehicles are nothing short of technological brilliance, but to call them an immediate concern to Ubers business would be far fetched. Waymo is the clear leader, and is scaling rapidly, however Waymo is currently only available in a handful of cities. With concerns over geo fencing new cities, regulatory approval, and autonomous vehicle performance in more harsh winter climates you have to wonder if even a company financially backed by google can challenge Uber’s network within the next 5-10 years.

Uber is not resting on its laurels when it comes to autonomous either. Waymo and Uber have already reached agreements to offer Waymo autonomous rides through the Uber network in multiple prominate US cities. Internationally Uber has announced partnerships with multiple companies such as Aurora, AVride, WeRide, Wayve, PonyAI, VW, Volvo and many more. With rides notably going live in Saudi Arabia. Albeit without the technical capabilities of Waymo. Tesla presents one of the only major companies to not partner with Uber, and will be an interesting domino to watch fall, no matter the direction.

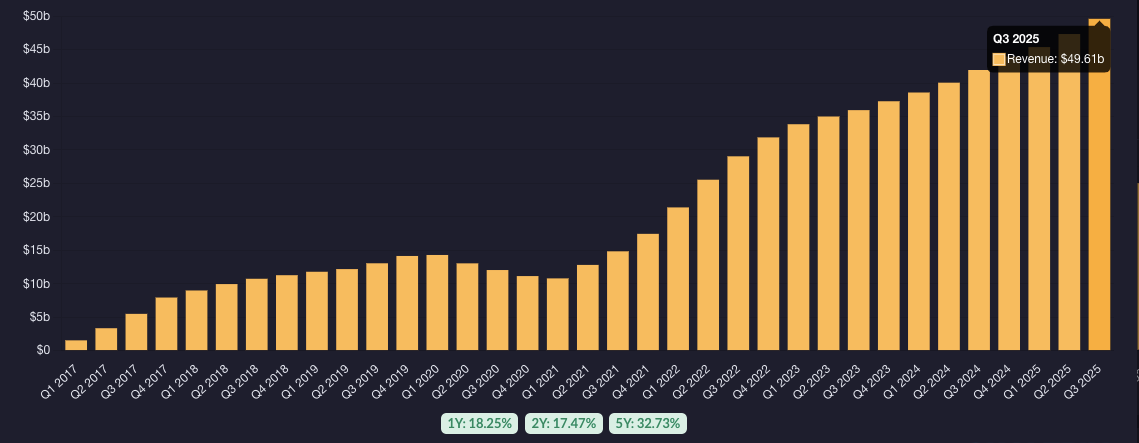

Despite Uber’s valuation in the stock market, the business has been thriving in recent years. Uber reached nearly 50 billion in total revenue over the last 12 months.

With an impressive growth rate of just over 18% in the last year, and actually an acceleration from the 2 year growth rate. This does not look like the revenue chart from a struggling company.

In term of a profitability metric Uber’s net income over the last 12 months has been positively affected with a one time affect to the tune of billions of dollars. This makes the 10x earnings Uber trades at deceiving. Instead of net income we will look at free cash flow to give us a better look at Ubers annualized earnings.

While still trading at a modest 20x cash flows there is no signs of struggling here either as the company has rapidly increased its margin profile over the last few years.

Uber has an impressively large customer base of 189 million monthly active customers around the world and over 12 billion trips logged in the past year.

With scale of this size, Uber is uniquely positioned to continue to increase its margin profile in the coming years. Assuming no increase to number of trips in a given year, or expenses at Uber. A 50c price increase on every trip would result in an extra $6+ billion in annualized profits. With 6 Billion in profits currently representing about 3% of Ubers market cap and a substantially boost to its current earnings.

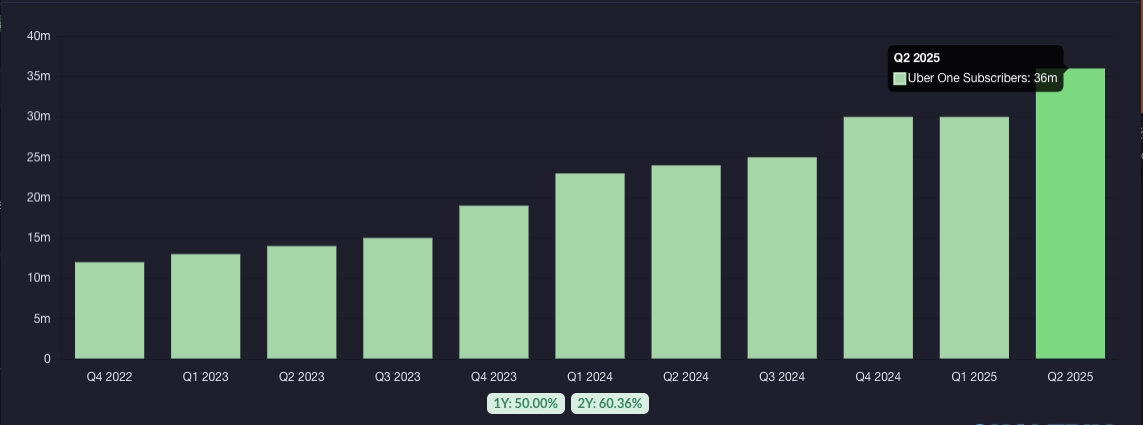

Along with price increases, scale of this size positions Uber well for a subscription offering. which the company unveiled in 2021. The subscription product called UberOne allows users to get 0 fees when ordering through UberEats, discounts on delivery and pickup, cash back on rides, and cancellation without penalty.

UberOne has 36 million subscribers representing an impressive percent of the monthly active users for a product that has only been around a few years. UberOne perks also primary focus on the apps secondary features such as delivery signaling a large portion of the user base is using multiple Uber products.

With a $10 per month or $100 per year price tag UberOne is starting to make up a sizable chunk of Ubers profits. The strong growth from UberOne will continue to add a predictable highly profitable income stream to the company.

Looking at the business, its hard not to think what a wonderful job management has done here. Nearly ever financial metric, and KPI is growing high teens, and the company is addressing its major question marks with partnerships and strategic investments.

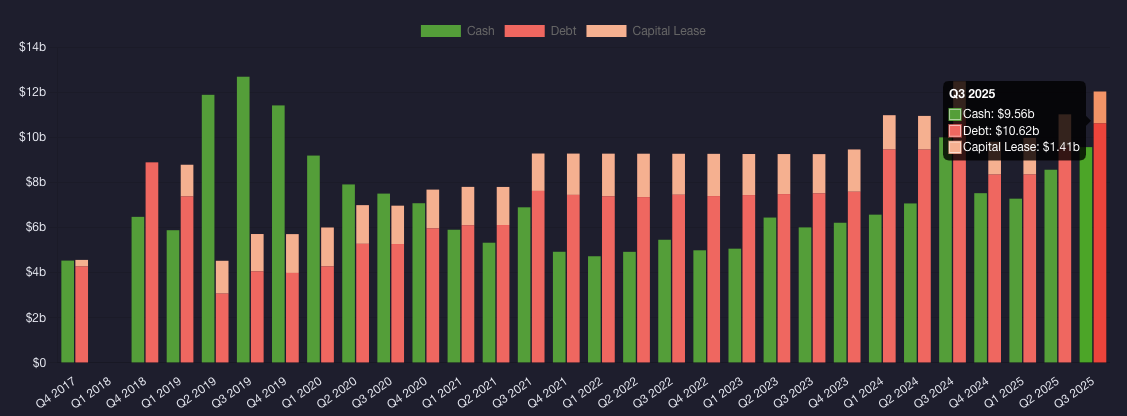

This companies balance sheet also remains in very solid condition and with Uber generating $8 billion in free cash flow over the last year it puts Uber in a very advantageous position.

With Uber’s newfound profit, in the coming years they will have to put this money to work. I believe there is 3 main use of this capital.

Debt Reduction With Uber already having an investment grade credit rating, and a solid balance sheet with only 1 billion of net debt, I view this as the least likely option, but with 1-2 years of cash flows Uber could wipe away its entire debt.

Acquisitions and Investments

With the advent of autonomous vehicles Uber may be on the look out to acquire an entire company with these capabilities. A leading autonomous company, developed at Uber with leading network, and data would be an immediate force to be reckoned with. Profitability of such a business line would be a concern, however if this were to happen the economics would ultimately end up being favorable to Uber. Where a company such as Hertz could potentially maintain vehicles. Uber has many investments in ride sharing apps world wide as well such as DiDi and Grab in China and South East Asia. Investments into the leading player in different markets will be something I continue to monitor. Overall I think Uber will at least continue to invest into leading players internationally, however this will be not consume the lions share of cash flows in an average year.

Return of Capitol to Shareholders

With Uber stock trading at 20x cash flows the investment into one’s self through buybacks look very attractive here. Provided the use of capitol doesn’t look far more attractive in option 2. Uber is well position for the next few years to repurchase 3-5% of the stock annually. This would accelerate Uber’s per share profitability substantially, almost certainly pushing most if not all metrics past 20%. In most scenarios, I view this as the most likely and best use of Uber’s capitol.

If you are say waiting for a company to hit you between the eyes with a 2x4, this might have already done it. If you are like most of us and still want to see the numbers, you’ve made it.

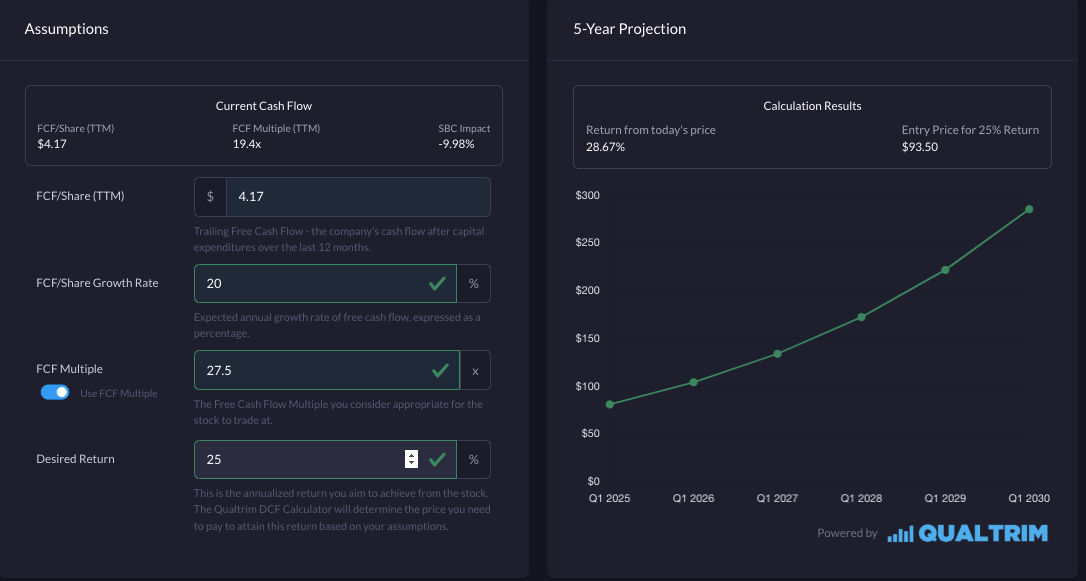

In terms on a base case valuation I see Uber growing revenue by 18% annually for the next 5 years. I see margin expansion through price increases and continued adoption of UberOne to the tune of 1% each year. Finally I see Uber repurchasing at least 1% of its shares outstanding per year. All together I think Uber will grow its Free Cash Flow per share by 20% over the next 5 years. For a company of Ubers size, growth rate, and moat in a base case with these assumptions I view a 25-30 multiple as appropriate.

With a 20% growth rate and a 27.5 multiple at the end of 5 years we end up with a $285 Uber and a 28% annual return. A return even Warren would have to entertain. Ultimately I even view these assumptions as somewhat modest for a base case. Uber can easily grow bottom line faster than a combined 2% annually. Uber has the ability to grow bottom line 4-6% annualized for a number of years through multiple avenues. If Uber raises prices, continues UberOne penetration, or executes a large share repurchase program. That would put the projected CAGR north of 30%.

I think the down side of autonomous vehicles is more than priced into Uber stock. Even if autonomous did erode Ubers moat overnight. You will likely not lose much more than opportunity given Uber’s current multiple, this is an attractive head’s I win, Tail’s I don’t lose much bet. Uber has positioned themselves well for autonomous, baring Waymo, or Tesla’s RoboTaxi becoming an overnight sensation, its hard to imagine a company even using autonomous to compete with Uber rather than partner. Furthermore for the next 5-10 years its hard to imagine a world that has any where close to as many autonomous car to standard cars.

For a company that many investors have scoffed at. It’s hard to deny the network effects of a company that has nearly 200 million monthly customers and their product is used 12 billion times a year. If thats not a moat then what is?