Sportradar: The Operating System of Global Sports Data

An analytical deep dive into the business model, the AI pivot, and the DCF models to see if the base case offers a margin of safety.

Introduction

In the high-stakes world of global sports betting, the names FanDuel, DraftKings, and Bet365 dominate the headlines, but the true architect of the industry remains largely invisible to the average fan. Sportradar (SRAD) has evolved from a Norwegian data-scraping startup into the indispensable “operating system” of modern sports. By turning live matches into a real-time, tradable asset class, Sportradar has secured a near-duopoly in a market where data is the only currency that matters. As the company pivots from a human-centric “scouting” operation to an AI-driven “4D data” powerhouse, it stands at a critical inflection point. This deep dive explores how Sportradar’s transition from a high-growth tech firm to a high-efficiency cash machine is reshaping the landscape of sports media and gambling—and what it means for investors looking to capitalize on the “picks and shovels” of the betting gold rush.

Table of Contents

History

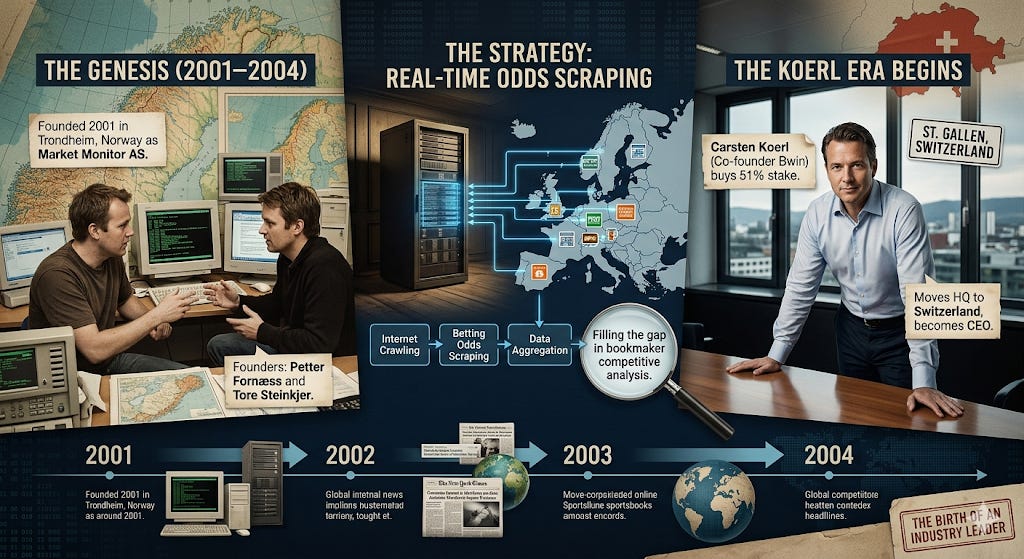

The Genesis (2001–2004)

Sportradar was founded in 2001 in Trondheim, Norway, originally under the name Market Monitor AS.

The Founders: Petter Fornæss and Tore Steinkjer developed a software program to crawl the internet and scrape betting odds from various online sportsbooks.

The Strategy: In the early days of online betting, there was no centralized way for bookmakers to see what their competitors were doing in real-time. Market Monitor filled this gap.

The Koerl Era Begins: Carsten Koerl, a heavy-hitter in the industry who had previously co-founded Bwin, saw the potential and bought a 51% stake in the company. He eventually moved the headquarters to St. Gallen, Switzerland, and became the driving force as CEO.

The Pivot to “Live” and Integrity (2005–2011)

This period saw the company transition from a data aggregator to a technology partner.

Live Data Focus (2005): Sportradar realized that the future of betting wasn’t just pre-match odds, but “in-play” betting. They shifted their focus to ultra-low latency live data feeds.

The Integrity Guard (2005–2009): Following the “Hoyzer” match-fixing scandal in German football, the company developed an Early Warning System (EWS). In 2009, they launched the Fraud Detection System (FDS) in partnership with UEFA, establishing themselves as the “police” of sports data, which gave them immense credibility with leagues.

Global Expansion & US Market Entry (2012–2020)

As the U.S. began to signal a shift toward legalized sports betting, Sportradar made its move.

US Entry (2013): They acquired SportsData LLC, a US-based firm, which gave them the infrastructure to cover American sports (NFL, MLB, NBA) with the same granularity they had for European soccer.

The “Big Three” Partnerships: Between 2014 and 2019, Sportradar secured massive data distribution deals with the NFL, NBA, and NHL. These weren’t just data deals; they often included equity components or exclusive rights to distribute “official” league data to sportsbooks.

Strategic Backing: The company attracted high-profile investors during this time, including Michael Jordan, Mark Cuban, and Ted Leonsis, signaling that the sports world’s power brokers were all-in on data.

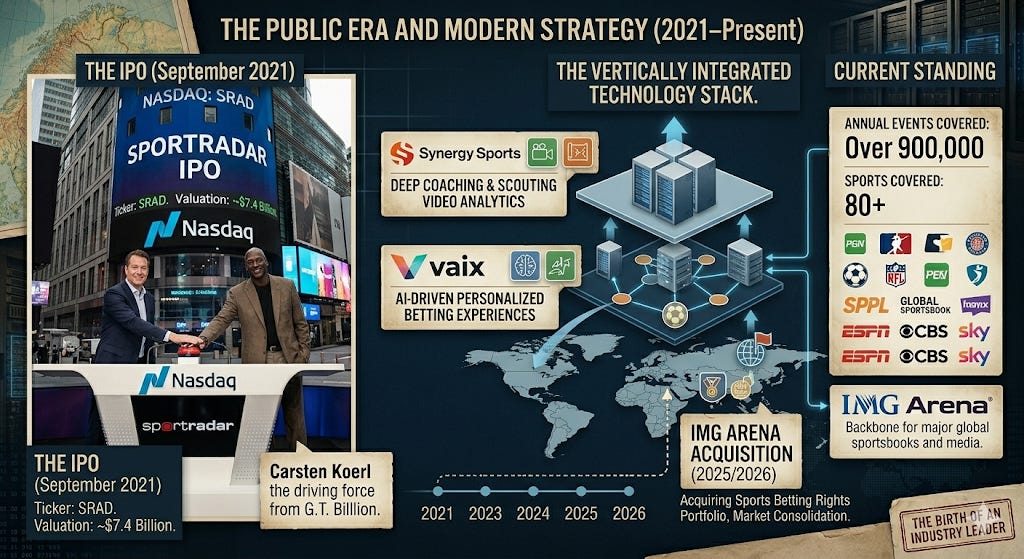

The Public Era and Modern Strategy (2021–Present)

The current era is defined by aggressive M&A and becoming a vertically integrated technology stack.

The IPO (September 2021): Sportradar went public on the Nasdaq (ticker: SRAD) with a valuation of roughly $7.4 billion. Michael Jordan famously joined Koerl on stage to ring the opening bell.

Acquisition Spree: They began buying companies that allowed them to offer more than just data:

Synergy Sports: For deep coaching and scouting video analytics.

Vaix: For AI-driven personalized betting experiences.

IMG Arena (2025/2026): One of their most significant recent moves, acquiring the sports betting rights portfolio of IMG Arena to further consolidate their market lead.

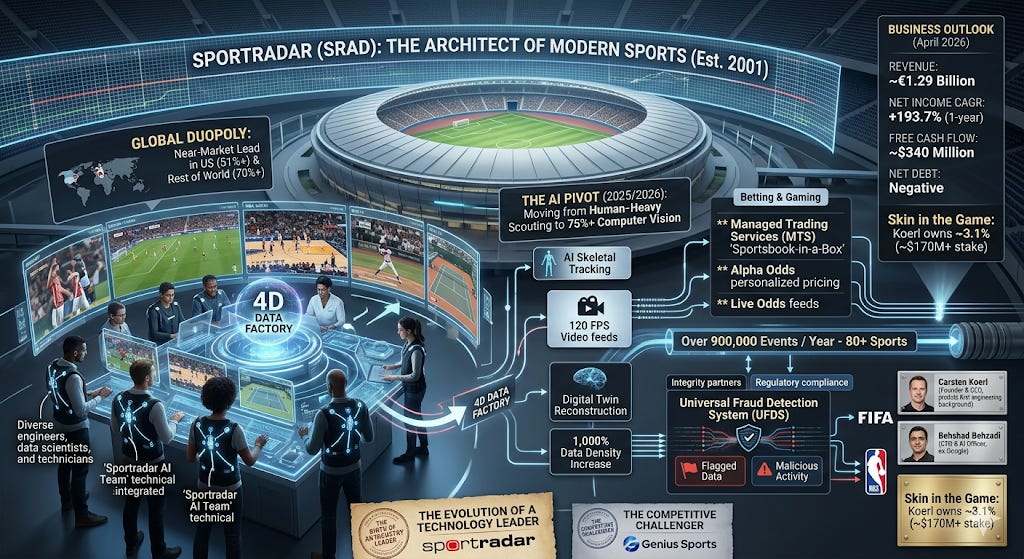

Current Standing: Today, Sportradar covers over 900,000 events annually across 80+ sports and serves as the backbone for nearly every major sportsbook and sports media outlet globally.

Product

To understand Sportradar’s dominance, you have to stop thinking of them as just a “data provider” and start seeing them as the operating system for the sports betting and media industry.

Their products are designed to touch every part of a game’s lifecycle—from the moment a player steps on the court to the moment a bet is settled in a fan’s app.

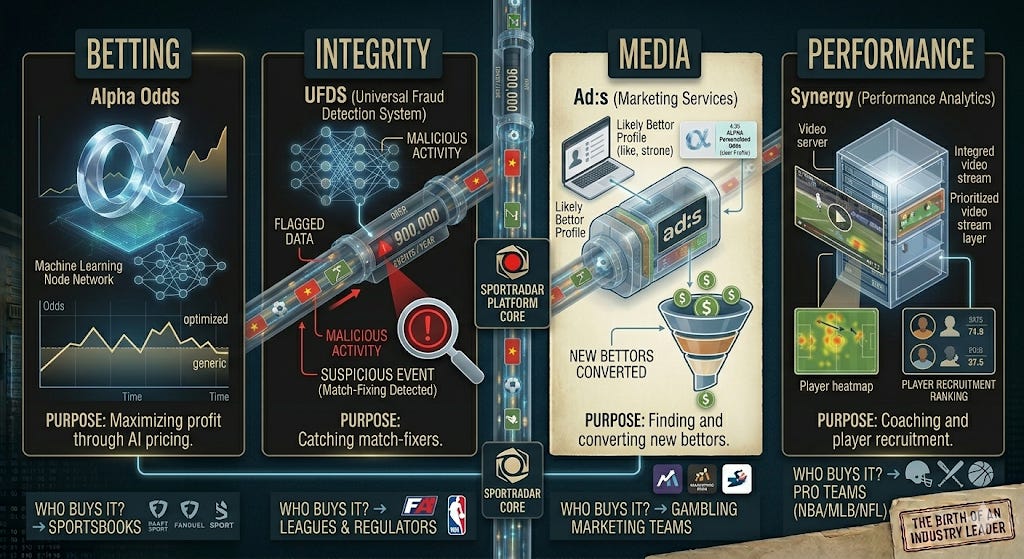

Betting & Gaming: The Revenue Engine

These products are sold to sportsbooks (like FanDuel, DraftKings, or Bet365) to help them run their businesses.

Managed Trading Services (MTS): This is essentially “Sportsbook-in-a-Box.” For smaller operators who don’t have thousands of employees, Sportradar handles the entire betting lifecycle: setting the odds, managing the risk of winning/losing, and settling bets.

Alpha Odds: Launched as a premium AI-driven service, Alpha Odds uses machine learning to create personalized pricing. Instead of one set of odds for the whole world, it allows bookmakers to adjust prices based on their specific liabilities or local market trends, significantly increasing their profit margins.

Live Odds & Pre-match Feeds: The core “pipe.” Sportradar provides the raw data and calculated probabilities for over 900,000 events a year. If a bookmaker wants to offer a bet on “Next Corner Kick” in a third-division soccer match in Vietnam, they get that data here.

Integrity Services: The “Police” Product

This is the product that gives Sportradar its “white hat” reputation and allows it to partner with government regulators and leagues like FIFA and the NBA.

Universal Fraud Detection System (UFDS): This is a sophisticated AI tool that monitors betting patterns across 600+ bookmakers worldwide.

How it works: If a massive, unusual amount of money is bet on a random tennis match in a specific region, the UFDS flags it.

The Result: Sportradar provides the evidence used in courtrooms and by sports leagues to ban players or officials for match-fixing. They actually offer a basic version of this for free to leagues to build goodwill and secure data rights.

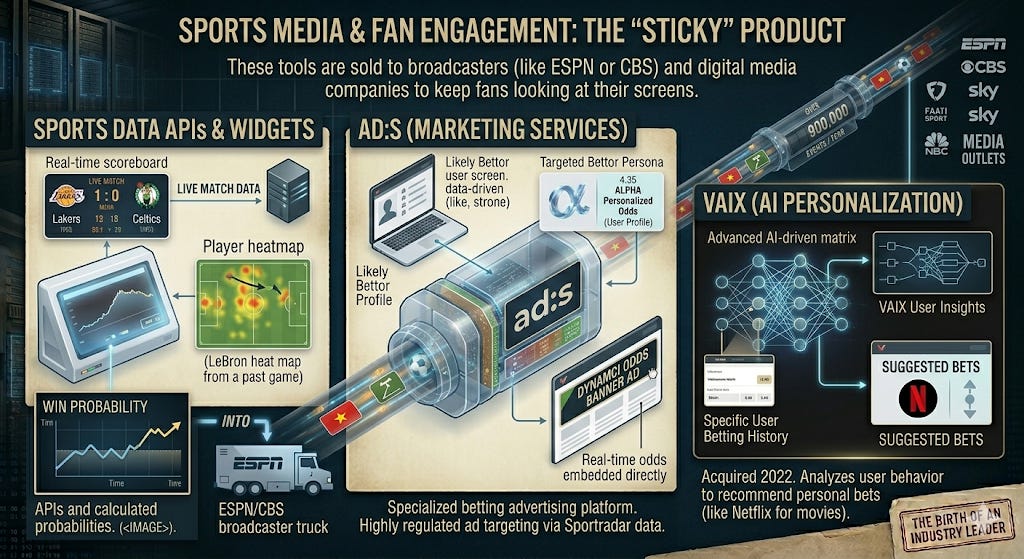

Sports Media & Fan Engagement: The “Sticky” Product

These tools are sold to broadcasters (like ESPN or CBS) and digital media companies to keep fans looking at their screens.

Sports Data APIs & Widgets: The real-time scoreboards, player heat maps, and “win probability” graphics you see on sports apps or during broadcasts are often powered by these APIs.

Ad:s (Marketing Services): This is a specialized advertising platform for the betting industry. Since sports betting ads are highly regulated, ad:s uses Sportradar’s data to target “likely bettors” across the web with real-time, dynamic odds embedded directly in the banner ads.

VAIX (AI Personalization): Acquired in 2022, this tech analyzes how a specific user bets and then recommends “suggested bets” to them, similar to how Netflix recommends movies.

Synergy Sports: The “Pro” Product

Acquired for $440 million in 2021, Synergy is the gold standard for high-level coaching and scouting.

Automated Video Capture: They use AI-powered cameras to record games without a human operator.

Deep Scouting: Every single “possession” in a game is tagged. An NBA scout can search “Every time Stephen Curry drives left when defended by a taller player” and instantly get a video playlist. This is a must-have for almost every pro team in the US.

Sportradar uses a “hybrid” model to collect data. They are currently in the middle of a massive technological shift, moving from a human-heavy operation to one powered almost entirely by AI and Computer Vision.

As of 2026, here is how the “data factory” actually works:

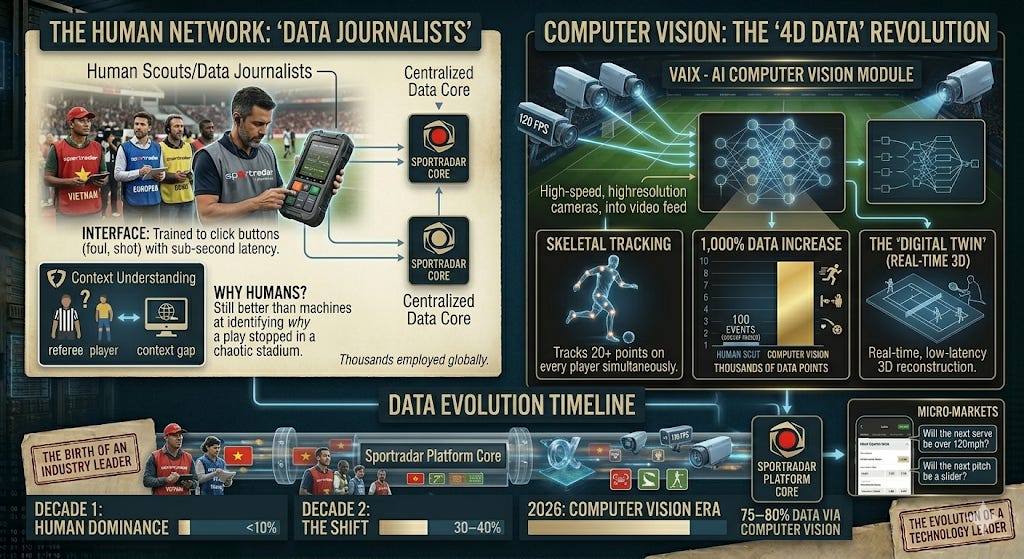

The Human Network: “Data Journalists”

For decades, Sportradar’s backbone has been a global army of scouts (often called Data Journalists).

The Foot Soldiers: Sportradar employs or contracts thousands of people worldwide who attend matches in person.

The “Interface”: These scouts use a specialized handheld device or mobile app. They aren’t just fans; they are trained to click buttons for every event (a foul, a throw-in, a shot on goal) within sub-second latency.

Why humans? Humans are still better than machines at context—identifying why a play stopped or which player a referee is talking to in a chaotic stadium environment.

Computer Vision: The “4D Data” Revolution

This is where the company is putting all its R&D. By 2026, Sportradar aims to have 75–80% of its data collected via Computer Vision rather than manual entry.

What it is: Instead of a scout clicking a button, AI software “watches” the video feed (at 120 frames per second).

Skeletal Tracking: The AI tracks 20+ points on every player’s body simultaneously. It knows exactly where a player’s knee is or the precise angle of a quarterback’s arm during a release.

1,000% Increase in Data: While a human scout might record 100 “events” in a soccer match, Computer Vision can record thousands of data points—player velocity, distance traveled, ball trajectory, and spacing between defenders.

The “Digital Twin”: This tech creates a real-time 3D reconstruction of the game. This allows sportsbooks to offer “Micro-markets” (e.g., “Will the next serve be over 120mph?” or “Will the next pitch be a slider?”).

Official League Partnerships: The “Gold Pipe”

When Sportradar signs a deal with the NBA or MLB, they don’t just get a badge; they get direct access to stadium infrastructure.

In-Stadium Sensors: In leagues like the NBA, Sportradar uses optical tracking systems installed in the rafters of every arena.

Low Latency: Because they are “official” partners, their data feed usually leaves the stadium faster than the television broadcast. This “latency edge” is why sportsbooks pay them millions—it prevents bettors from “court-siding” (betting on something they see in person before the bookmaker’s odds can update).

The “Synergy” Video Layer

The acquisition of Synergy Sports gave them a specialized way to collect data from thousands of lower-tier games (college, international, pro-am).

Automated Cameras: They install AI cameras in gyms that automatically follow the ball and the players without a camera crew.

Auto-Tagging: The system automatically clips and tags video. If a coach wants to see every “pick and roll” from last night’s game, the AI has already cut the video and linked it to the data points.

The shift to Computer Vision is a margin play. As they move from paying thousands of humans to running server-side AI, their costs drop and their data becomes denser. This "4D Data" is what enables the next generation of betting—where you aren't just betting on who wins, but on the physics of the game itself.

Competition

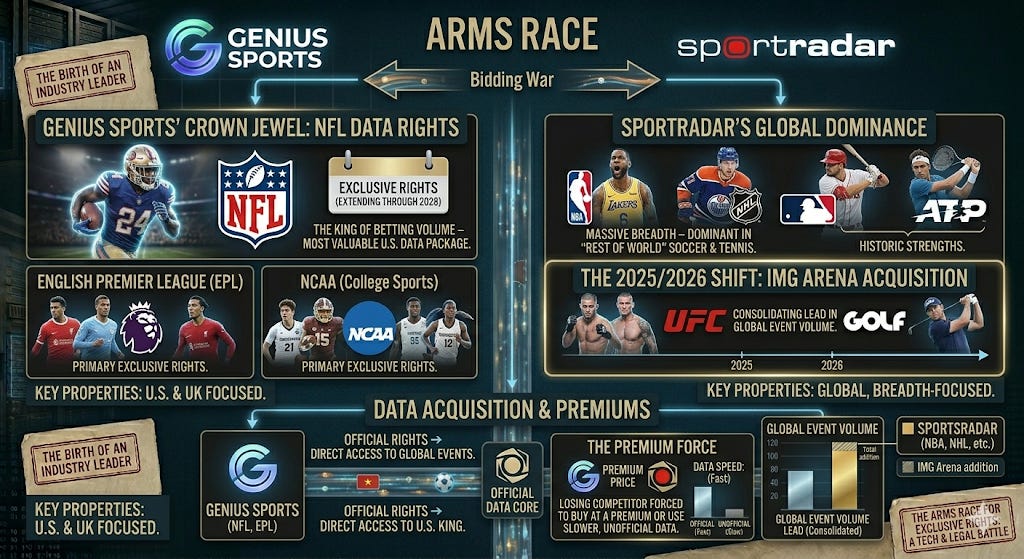

Sportradar (SRAD) is not without competition for this invaluable data however. Genius Sports (GENI) could be described as a "duopoly" with Sportradar, or locked in "Cold War" for sports data. While Sportradar is the older, larger "incumbent," Genius Sports has positioned itself as the high-growth, tech-focused challenger.

The “Arms Race” for Exclusive Rights

The most visible part of their rivalry is the bidding war for official data rights. If one company wins a league’s exclusive rights, the other is often forced to buy that data from their competitor at a premium or use slower, unofficial data.

Genius Sports’ Crown Jewel: They hold the exclusive NFL data rights (extending through 2028). This is the most valuable data package in the U.S. market because the NFL is the king of betting volume. They also hold the rights for the English Premier League (EPL) and NCAA.

Sportradar’s Global Dominance: They counter with massive breadth, holding the rights for the NBA, NHL, MLB, and ATP (Tennis). Historically, Sportradar has been stronger in “rest of world” soccer and tennis, while Genius has fought hard for the high-profile U.S. and UK properties.

The 2025/2026 Shift: Sportradar recently acquired the IMG Arena portfolio, which brought them rights for the UFC and major golf tours, further consolidating their lead in global event volume.

Differing Business Philosophies

While they provide similar services, their strategic “bets” are different:

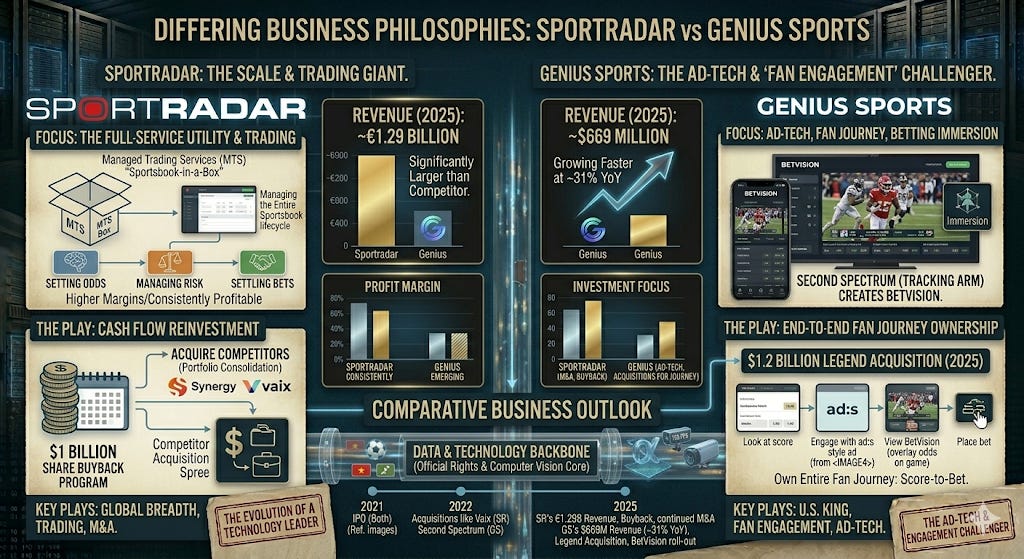

Sportradar: The Scale & Trading Giant.

Revenue (2025): Approximately €1.29 Billion (significantly larger than Genius).

Focus: They act as a full-service utility. They don’t just provide data; they manage the entire sportsbook for clients (Managed Trading Services). They have higher margins and are more consistently profitable.

The Play: Use their massive cash flow to buy back shares ($1 billion program) and acquire competitors.

Genius Sports: The Ad-Tech & “Fan Engagement” Challenger.

Revenue (2025): Approximately $669 Million (growing faster at ~31% YoY).

Focus: Genius is pivoting away from being just a “data wholesaler.” With their recent $1.2 billion acquisition of Legend, they are trying to own the entire fan journey—from the moment a fan looks at a score on a website to the moment they place a bet.

The Play: They use Second Spectrum (their tracking arm) to create “BetVision,” which overlays betting odds directly onto live video streams, making the experience more immersive.

Technology: Computer Vision vs. Hardware

Both companies are moving toward AI-driven collection, but their methods vary:

GeniusIQ: Genius relies heavily on Second Spectrum’s optical tracking. In 2026, they are expanding their “GeniusIQ” system to double the number of stadiums covered. Interestingly, their system often uses a fleet of iPhones/mobile hardware to capture and process video in real-time at the “edge.”

Sportradar 4Sight: Sportradar is focusing on Skeletal Tracking to create “Digital Twins” of games. Their goal is to turn the game into a 3D environment where they can calculate things like “catch probability” or “expected goals” in milliseconds.

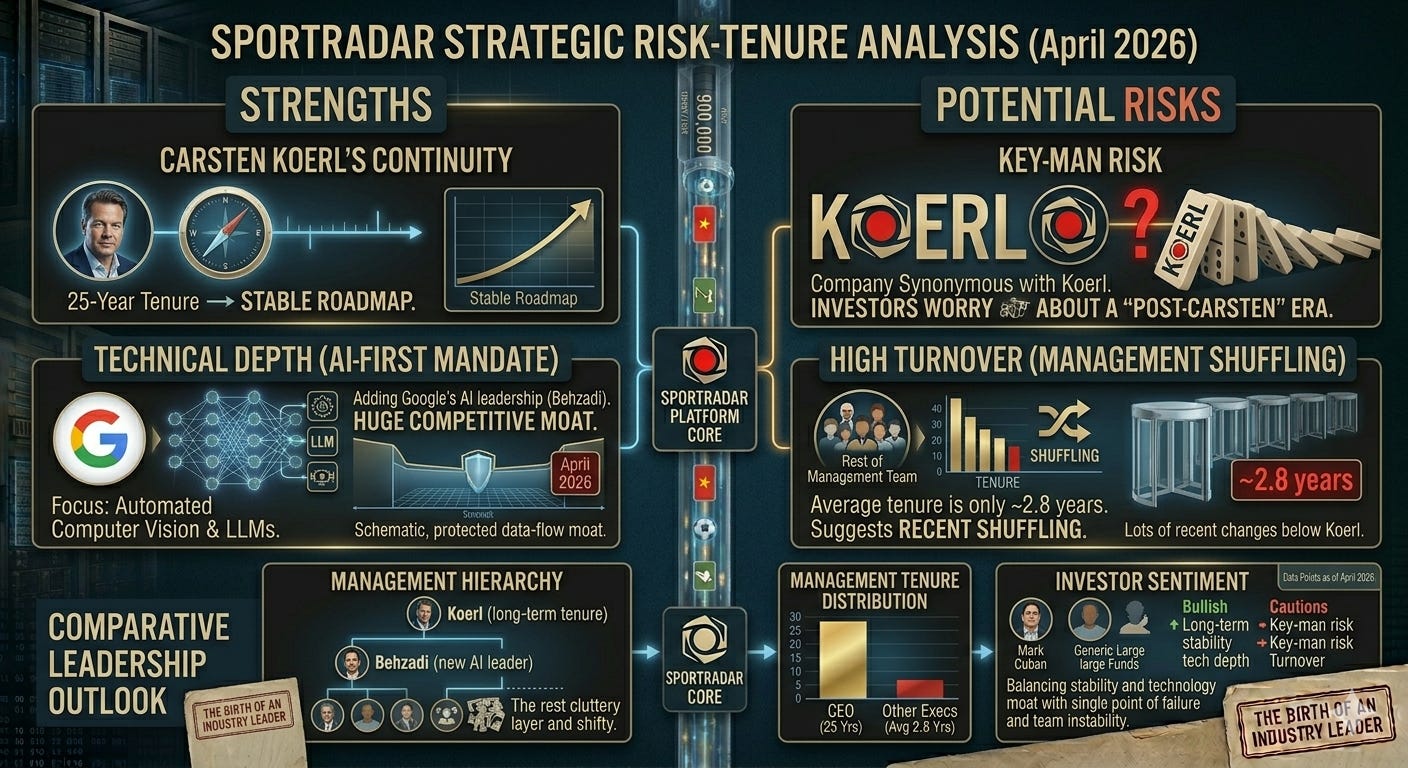

Management

Unlike many tech mid caps that cycle through CEOs, Sportradar is still led by its original founder. This gives the company a level of long-term strategic consistency that is rare in the gambling/tech space.

The Architect: Carsten Koerl (Founder & CEO)

Carsten Koerl isn’t just an executive; he is a pioneer of the industry. To understand his leadership, you have to look at his “product-first” engineering background.

Background: An engineer by training, he co-founded Bwin (one of the world’s largest betting brands) in 1997 before launching Sportradar in 2001. He has been the CEO for over 25 years.

The “Visionary” Reputation: Koerl is famous for recognizing early on that sports data shouldn’t just be “news”—it should be a tradable asset class. He treats a tennis match like a stock market ticker.

Leadership Style: He is known for being extremely technical and “hands-on.” In recent interviews (2025/2026), he has been vocal about his “AI-first” mandate, stating that any company not applying Large Language Models and automated computer vision to sports will be “extinct by the end of the decade.”

Skin in the Game: As of April 2026, Koerl still owns roughly 3.1% of the company directly (worth over $170M), ensuring his interests remain aligned with shareholders.

The “New Guard” (Strategic Hires)

In the last few years, Koerl has aggressively recruited top-tier talent from “Big Tech” and traditional finance to professionalize the company post-IPO.

Behshad Behzadi (Chief Product, Technology & AI Officer): This was a massive hire in 2024. Behzadi came directly from Google, where he was a co-founder of Google Assistant and Google Lens. His presence confirms that Sportradar is pivoting from a “data warehouse” to an “AI laboratory.”

Craig Felenstein (CFO): Joined in 2024 from Lindblad Expeditions, with deep roots at Discovery and News Corp. His job is to manage the transition from high-growth “startup mode” into a mature, high-free-cash-flow public company.

Eduard Blonk (Chief Commercial Officer): A veteran of the company since 2015, Blonk is the “deal-maker” responsible for the massive partnerships with the NBA, NHL, and MLB.

The Behshad Behzadi (ex-Google) hire, is a strong signal that Sportradar is trying to out-engineer Genius Sports, rather than just out-bid them for rights.

The Board of Directors: The “Power Players”

The board is where Sportradar’s influence in the sports and finance world becomes clear.

Jeffery Yabuki (Chairman): Former CEO of Fiserv. He brings deep expertise in “fintech” and payments, which is crucial as betting and financial transactions merge.

Breon Corcoran: The former CEO of Paddy Power Betfair (now Flutter). Having a former “customer” on the board gives them an inside look at what sportsbooks actually need.

The “Jordan” Influence: While not on the daily management team, Michael Jordan remains a key investor and advisor. His involvement isn’t just for marketing; he helps open doors with league owners and global brands that a typical tech CEO couldn’t reach

Business Risks

While Sportradar is a dominant market leader, its business model faces several high-stakes risks.

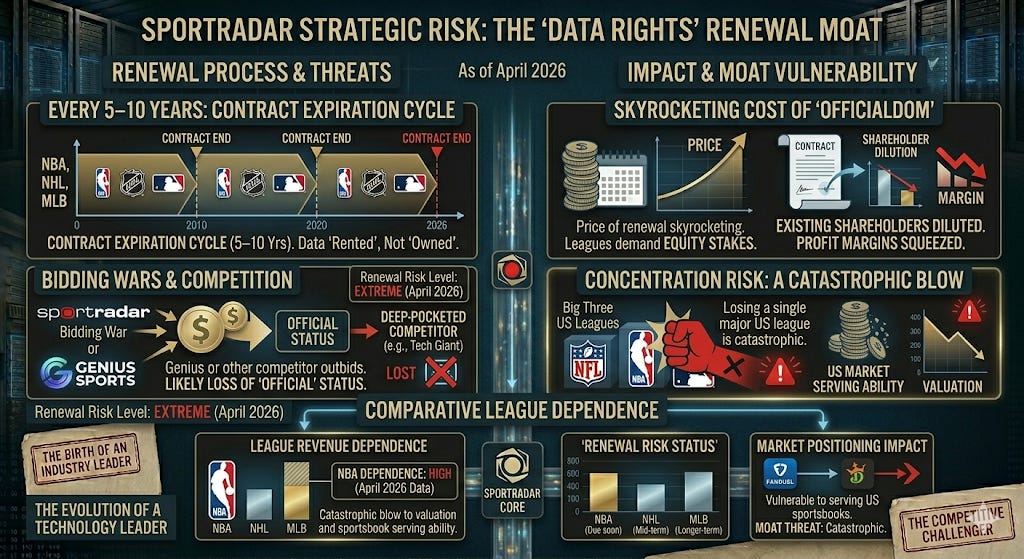

The “Data Rights” Renewal Risk

This is the single biggest threat to their moat. Sportradar does not “own” the sports; they rent the data from the leagues.

Bidding Wars: Every 5 to 10 years, major contracts (like the NBA or NHL) come up for renewal. If Genius Sports or another deep-pocketed competitor outbids them, Sportradar loses its “official” status for that league.

The Cost of “Officialdom”: Even when they win, the price is skyrocketing. Leagues now demand not just cash, but equity stakes in Sportradar. This dilutes existing shareholders and squeezes profit margins.

Concentration Risk: Losing a single major “Big Three” US league would be a catastrophic blow to their valuation and their ability to serve US sportsbooks.

Technical Execution: The AI Pivot

As we discussed, Sportradar is moving from human scouts to Computer Vision.

Model Accuracy: If their AI misidentifies a play (e.g., calling a “strike” a “ball” in a high-stakes MLB game), it could lead to millions in losses for their sportsbook clients. This creates “liabilities” that manual scouting rarely faced.

High CapEx: Building out “Skeletal Tracking” in thousands of stadiums is incredibly expensive. If the ROI (Return on Investment) on this tech doesn’t materialize—meaning sportsbooks aren’t willing to pay extra for “4D data”—it could lead to a massive drag on their free cash flow.

Regulatory & Integrity Headwinds

Because Sportradar is the “integrity partner” for leagues, they are on the front lines of political scrutiny.

Advertising Bans: Governments (especially in Europe and increasingly the US) are cracking down on sports betting ads. Since Sportradar’s ads product relies on these marketing budgets, a ban on gambling ads would directly hit their high-margin media segment.

Match-Fixing Scandals: If a major scandal happens in a league Sportradar “polices” (like UEFA or the NBA) and they fail to catch it, their reputation—and their “official” status—could be permanently damaged.

Competitive Dynamics (The Genius/IMG Factor)

The market is consolidating, which creates “all-or-nothing” scenarios.

M&A Integration: Sportradar recently acquired IMG Arena (late 2025/early 2026). Integrating a massive competitor is notoriously difficult. If they fail to merge the technology and sales teams smoothly, they could lose market share to a more focused Genius Sports.

Pricing Pressure: As the “duopoly” matures, sportsbooks (who are also struggling for profitability) are pushing back on the high fees Sportradar and Genius charge. This “squeezing from the middle” could cap their future revenue growth.

Financial Statements

Sportradar is exhibiting the classic profile of a maturing tech transitioning from growth at all costs, to a high-efficiency, cash-generating machine.

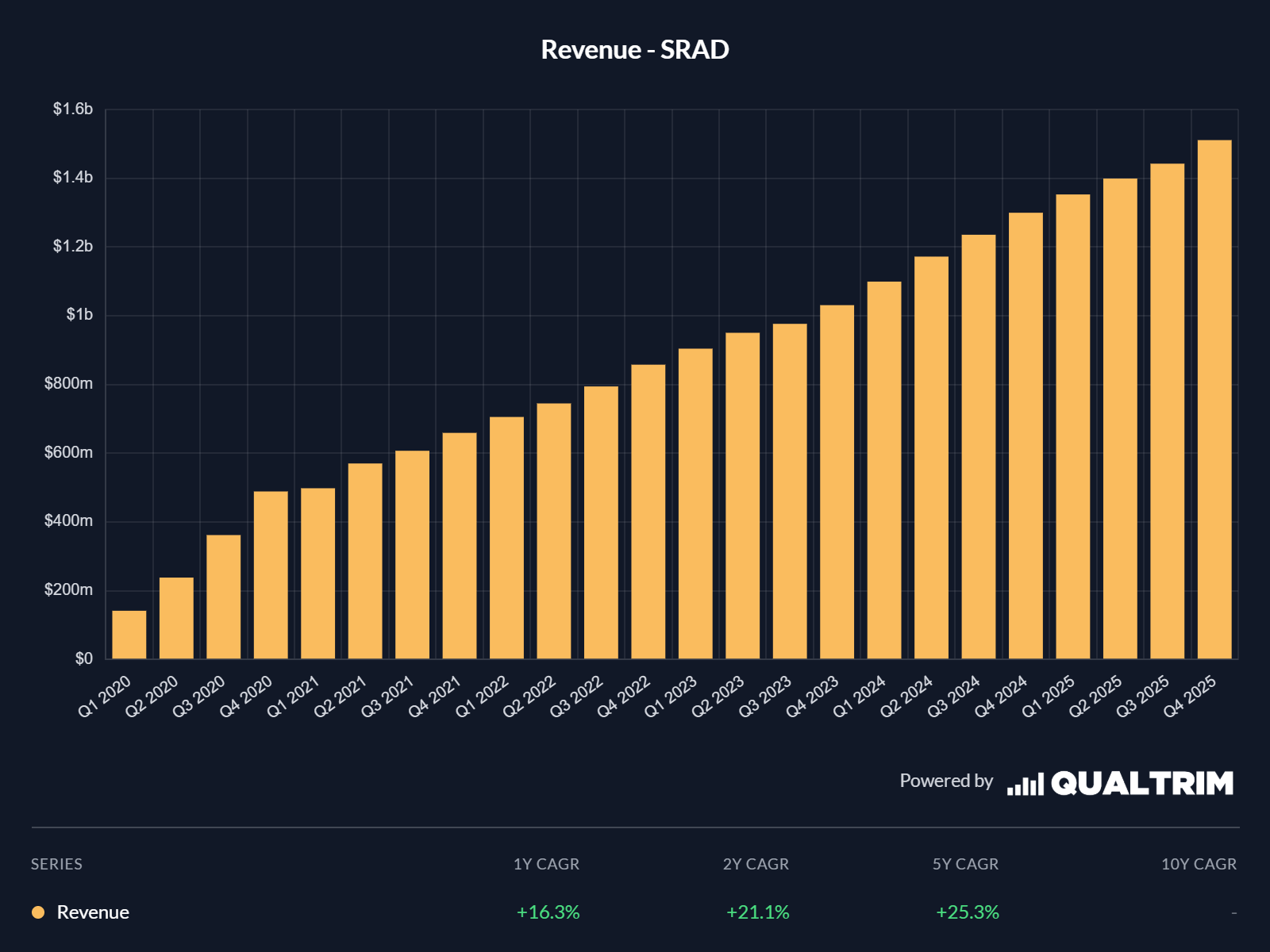

Revenue Growth: The Upward Staircase

The Revenue chart shows one of the most consistent growth trajectories in the sector.

Compound Annual Growth Rate (CAGR): With a 5-year CAGR of +25.3%, the company has successfully scaled from roughly $200M in early 2020 to surpassing the $1.5B mark by Q4 2025.

Resilience: Note the lack of seasonality or dips. Because Sportradar’s revenue is tied to long-term data contracts and “SaaS-like” subscriptions from sportsbooks, their income is incredibly predictable compared to the volatile betting companies they serve.

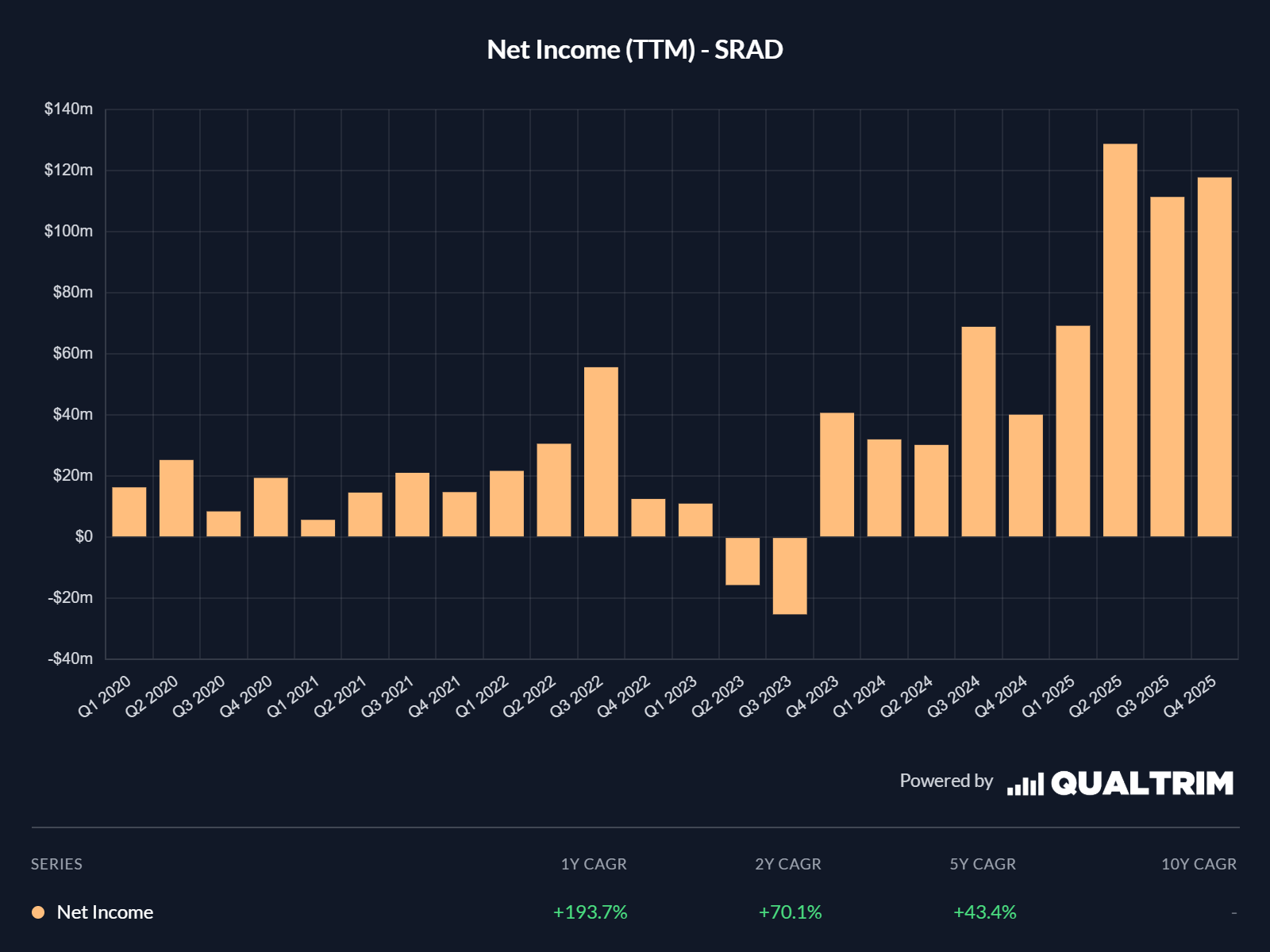

Net Income: The “J-Curve” Breakout

The Net Income (TTM) chart reveals the moment the business model “inflected.”

The Dip (2023): You can see a period of net losses in mid-2023. This likely reflects the heavy “investment phase” where they were aggressively spending on US data rights and the initial rollout of their AI Computer Vision tech.

The Breakout: Since Q4 2023, profitability has exploded. By Q4 2025, Net Income reached approximately $120M, representing a massive +193.7% 1-year CAGR. This suggests that their “operating leverage” is finally kicking in—revenue is growing faster than their expenses.

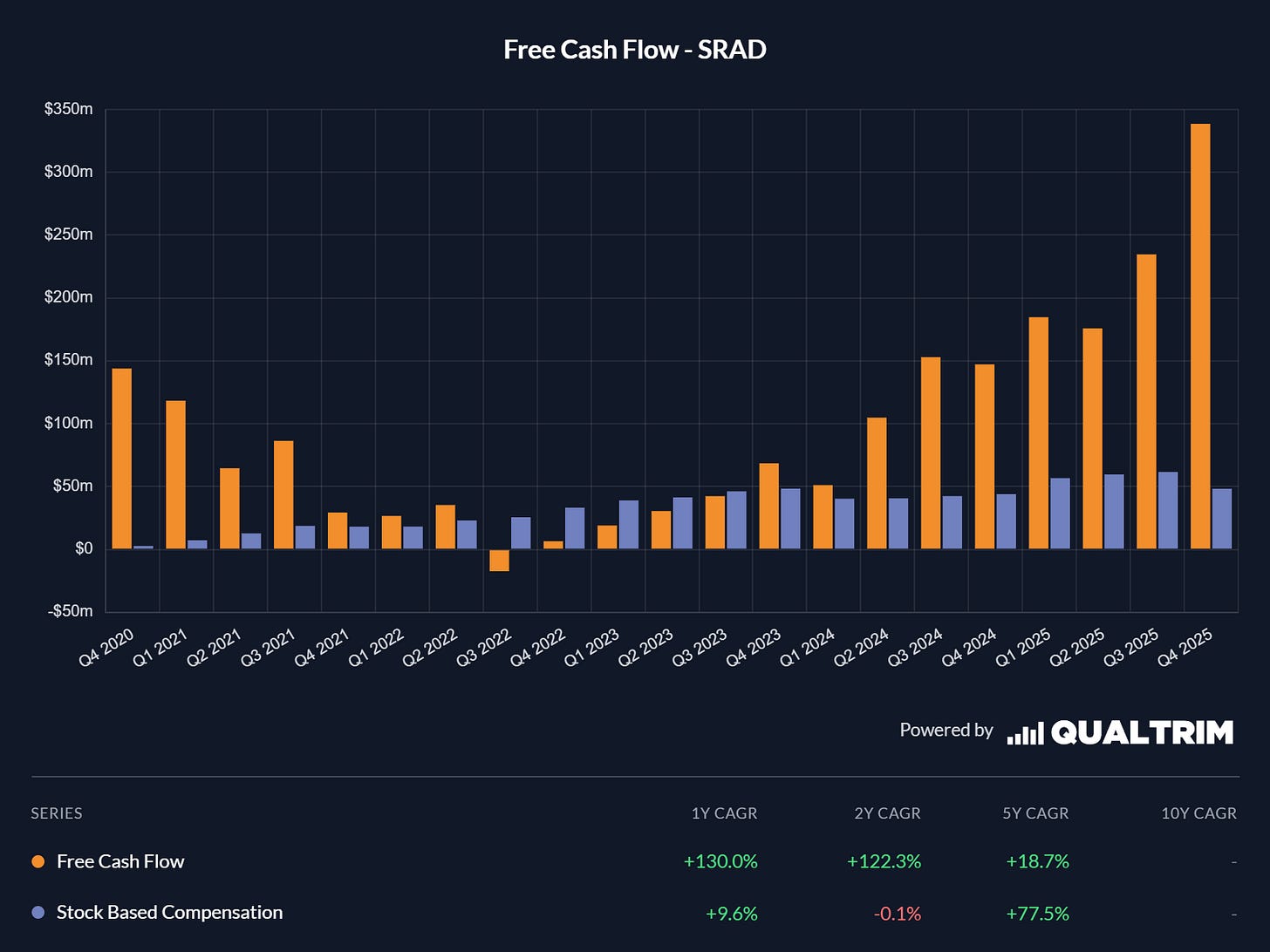

Free Cash Flow (FCF) & SBC: The Real Success Story

This is arguably the most important chart.

Cash King: FCF has skyrocketed to nearly $340M in Q4 2025 (a +130% 1-year growth rate). This gives management immense “optionality” for M&A or share buybacks.

Stock-Based Compensation (SBC) Control: Unlike many tech peers, Sportradar has kept SBC relatively flat (the purple bars). While FCF (orange) grew exponentially, SBC only grew by +9.6% over the last year. This means the cash flow is “real” and not just a byproduct of diluting shareholders.

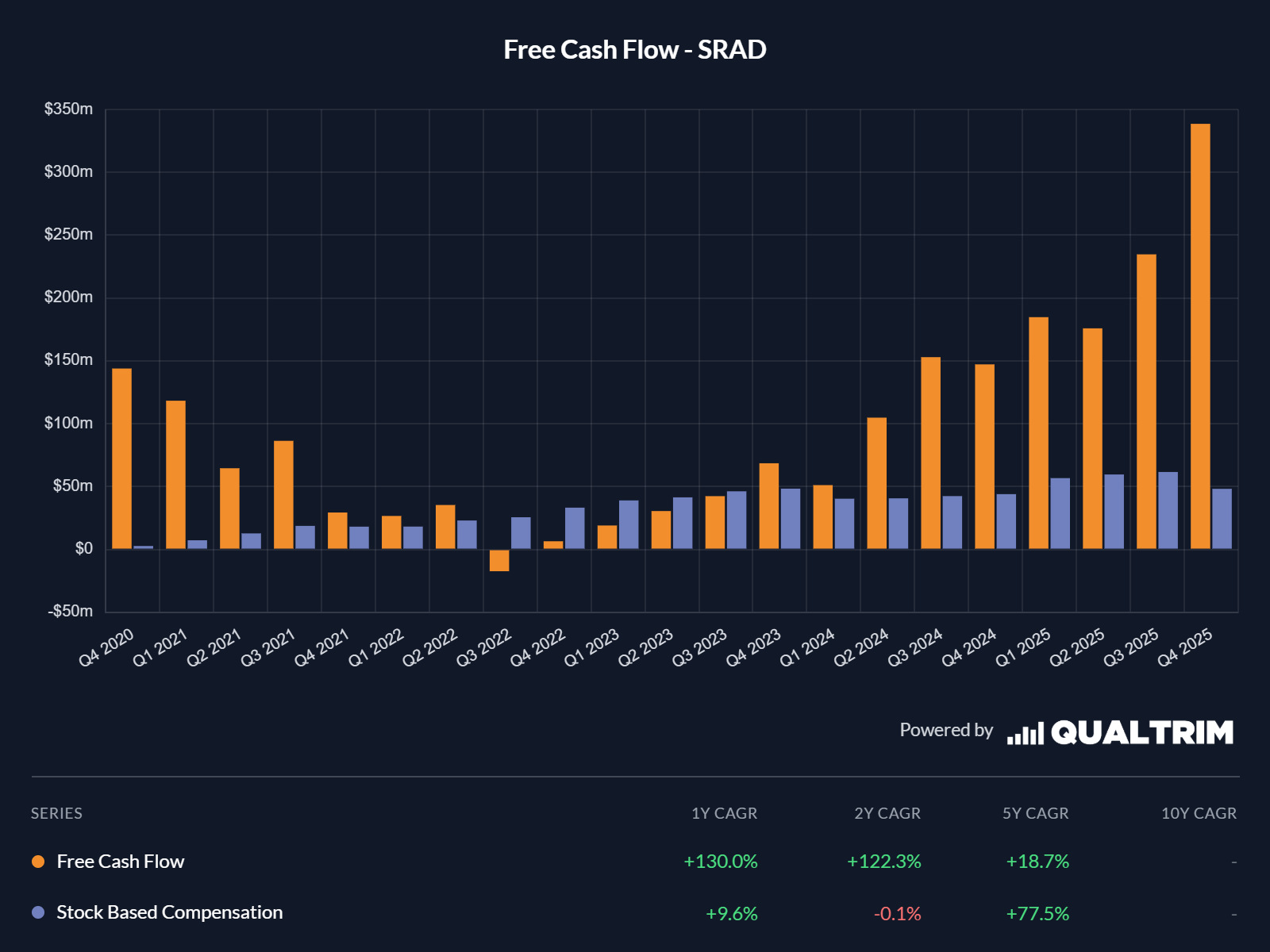

Capital Structure: De-Leveraging

The Cash & Debt chart shows a company that has significantly de-risked its balance sheet.

Cash Position: They maintain a healthy “war chest” of roughly $400M as of Q4 2025.

Debt Reduction: Look at the red bars. They carried significant debt in 2021-2022 (likely to fund US expansion). By late 2025, that debt has been drastically reduced to nearly negligible levels compared to their cash on hand. They are effectively Net Debt Negative.

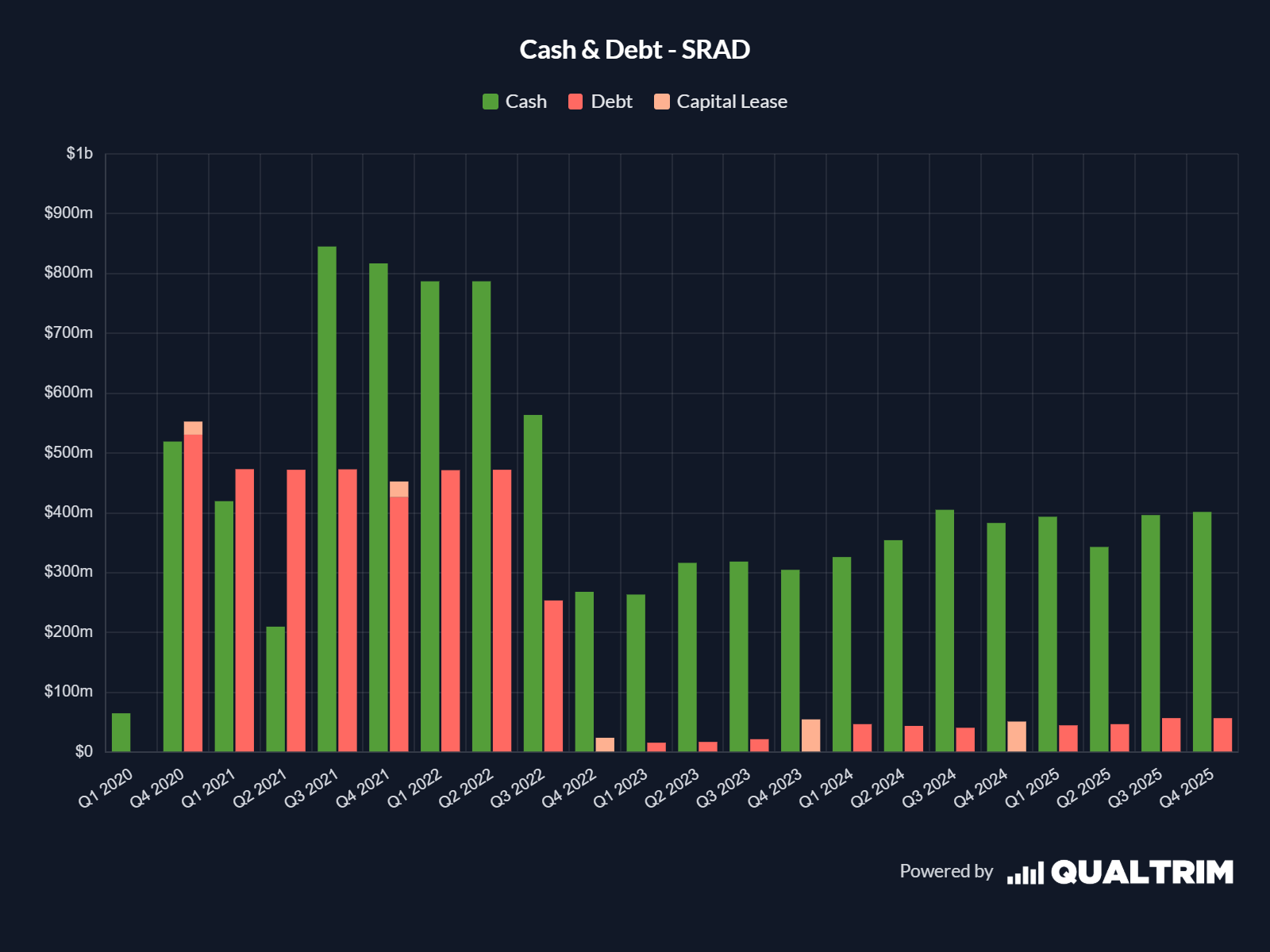

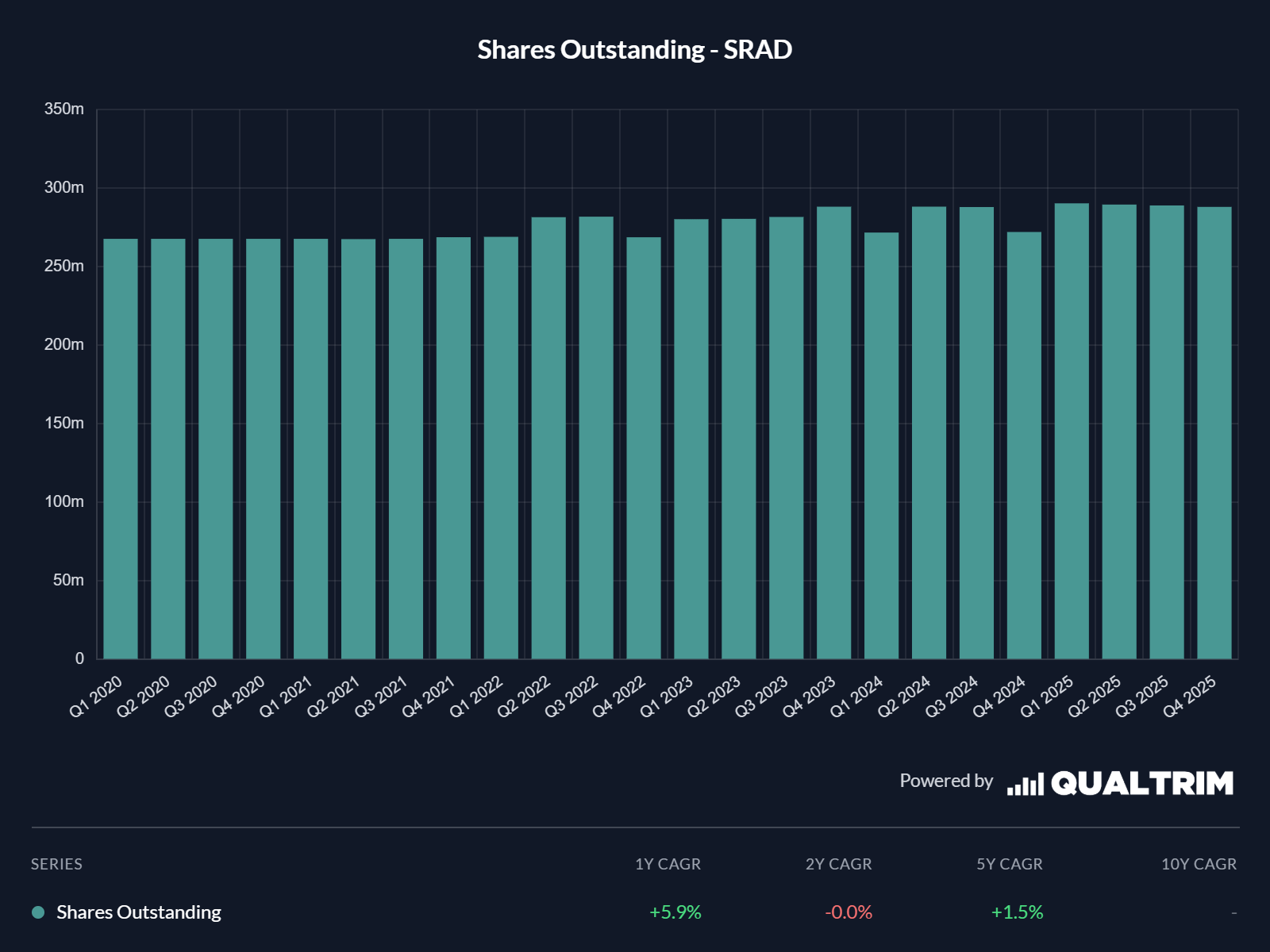

Shares Outstanding: Managing Dilution

The Shares Outstanding chart shows a stabilized share count.

The IPO Spike: You can see the jump in shares during 2021 when they went public.

Recent Stability: The count has flattened out at roughly 290M shares. Combined with their massive FCF, the company is now in a position where they can begin (or continue) share buybacks to drive “Earnings Per Share” (EPS) even higher.

Valuation

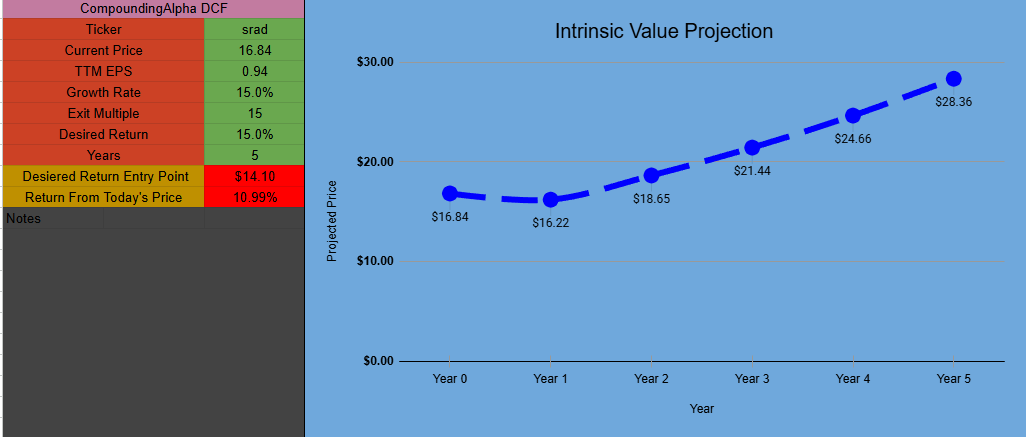

The Base Case: The “Market Utility” Scenario

Target Growth Rate: 15%

Exit Multiple: 15x

Intrinsic Value (Year 5): $28.36

Entry Point (for 15% Return): $14.10

This is the most realistic path, assuming Sportradar continues its current trajectory as the industry’s “operating system.”

Why it happens: Revenue grows in line with the broader global betting market. While data rights costs (NBA, ATP, etc.) remain high, the company’s scale allows them to maintain a 15% FCF growth rate. Share buybacks help keep the “per share” numbers healthy even if top-line growth settles into the mid-teens.

The Valuation: At a 15x multiple (standard for a mature tech utility), the stock is currently overvalued. While our “desired entry” is $14.10, the current price still offers a solid ~11% annual return, which is likely to beat the S&P 500.

The Bear Case: The “Commodity & Regulation” Scenario

Target Growth Rate: 6%

Exit Multiple: 12x

Intrinsic Value (Year 5): $15.10

Entry Point (for 15% Return): $7.50

This scenario assumes the “Squeeze” we discussed in the risks section comes to fruition.

Why it happens: Pro-league data rights become so expensive that they eat all the FCF growth. Simultaneously, major sportsbooks like FanDuel and DraftKings build more of their own “in-house” modeling, reducing their reliance on Sportradar’s premium products. Regulatory crackdowns on gambling ads in Europe and the US hit the ad:s marketing revenue hard.

The Valuation: In a low-growth environment (6%), the market de-rates the stock to a 12x multiple. At today’s price of $16.84, you would actually see a -2.16% return over 5 years.

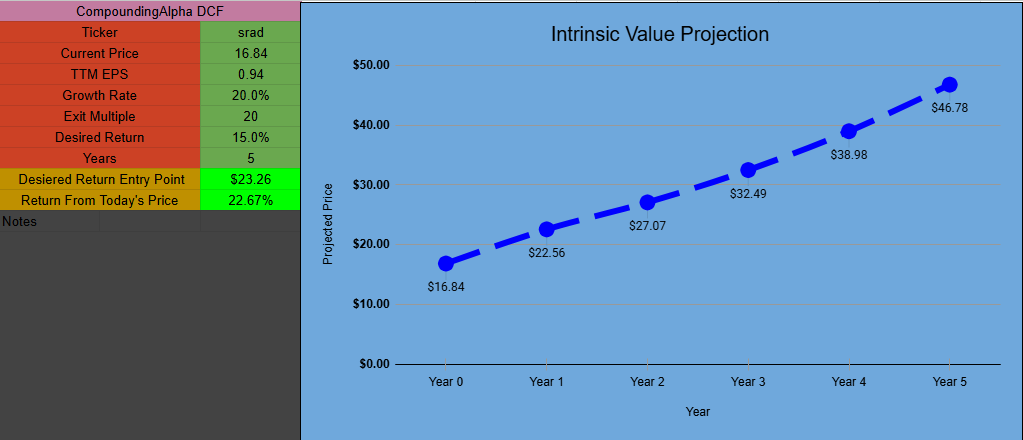

The Bull Case: The “AI-Driven Alpha” Scenario

Target Growth Rate: 20%

Exit Multiple: 20x

Intrinsic Value (Year 5): $46.78

Entry Point (for 15% Return): $23.26

In this scenario, Sportradar isn’t just a data provider; it’s a high-margin AI firm.

Why it happens: The pivot to Computer Vision (75%+ automated collection) works perfectly, drastically lowering the cost of data collection. Their Alpha Odds product becomes a “must-have” for sportsbooks, allowing Sportradar to take a larger percentage of the “net gaming revenue” (NGR) from their clients.

The Valuation: A 20x multiple is justified by a return to high-double-digit growth and dominant market share in the US, fueled by a successful integration of IMG Arena. At the current price of $16.84, this represents a massive 22.67% annual return.

Conclusion

Sportradar is no longer a speculative play on the legalization of sports betting; it is a mature, cash-generating utility that has successfully navigated its most expensive investment phase. While the “Cold War” with Genius Sports for exclusive league rights remains a persistent risk to margins, Sportradar’s aggressive pivot toward Computer Vision and the high-level recruitment of Big Tech talent like Behshad Behzadi suggests a strategy focused on engineering its way out of commodity traps. Financially, the company’s “J-Curve” breakout in net income and massive acceleration in free cash flow provide a fortress-like margin of safety that its competitors simply cannot match. Whether the stock achieves the “Bull Case” target of $46.78 depends on the successful scaling of its AI-driven Alpha Odds, but even as a “Base Case” market utility, Sportradar offers a compelling risk-reward profile. In an industry defined by volatility, Sportradar provides the rare combination of predictable revenue and a technological moat that makes it the definitive infrastructure play for the future of global sports.

The AI pivot you describe as moving from scouting to 4D data has a flip side worth examining. Sportradar's two-decade investment in a global network of in-venue human scouts was the moat for tier-two and tier-three sports coverage. Computer vision collapses that moat for any well-capitalized entrant, which is why the league rights deals (NBA renewed 2023 around $1B over the term, NFL went exclusive to Genius Sports for nine figures plus equity) are doing more of the load-bearing work in the bull case. The duopoly looks more like a rights-bidding war than a tech moat, and rights inflation tends to flow to the leagues, not the data shareholders.