Eating the Restaurant Industry: Why Toast ($TOST) is Winning the POS Wars

Square dominates the cafes, legacy rules the enterprises, but Toast is quietly hunting the "whales" to own the entire hospitality stack.

Introduction: Ripping Out the Operational Brain

For decades, the restaurant technology landscape was a fragmented nightmare. A typical mid-sized operator survived by duct-taping five to seven different vendors together: an on-premise NCR cash register, a separate legacy scheduling spreadsheet, a third-party payroll processor, and a clunky online ordering plug-in that constantly crashed. Every vendor sat in an isolated silo, leaving restaurateurs buried in manual data entry and margin leakages.

Then came Toast.

What began as a struggling consumer mobile app has morphed into one of the most compelling vertical SaaS stories in the public markets. Toast did not just build a software platform; they engineered a “Logistics OS”—a unified cloud infrastructure that acts as the operational brain of the modern restaurant. By anchoring themselves directly at the physical point of sale via cheap, durable Android hardware, Toast created a digital center of gravity. Once a merchant integrates their payments, frontline staff, kitchen routing, and supply chain into Toast, the switching costs become astronomically high. Ripping out Toast doesn’t just mean changing credit card terminals; it means shutting down the restaurant’s entire nervous system.

After years of critics labeling the company a low-margin payment processor masked as a tech stock, Toast has reached a monumental financial inflection point. Between 2024 and 2026, the company slammed the brakes on stock dilution, unleashed a massive shift into self-funded GAAP profitability, and transformed its cash-burning growth engine into a free cash flow cannon.

Table of Contents

Deep dives are only half the equation. Join me as we put this research into practice and build a high-conviction allocation strategy from the ground up in the CompoundingAlpha Tracking Portfolio.

The Evolution of a Logistics OS

Toast’s journey from a floundering consumer app to a vertical SaaS powerhouse is a classic “land and expand” case study. Their history is defined by a massive early pivot and an aggressive go-to-market strategy that displaced legacy players like NCR and Micros.

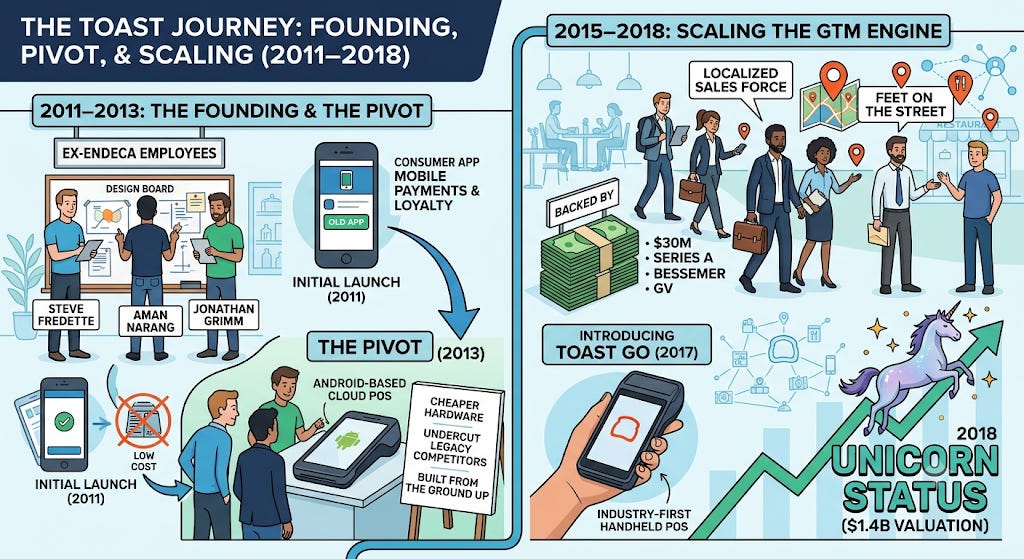

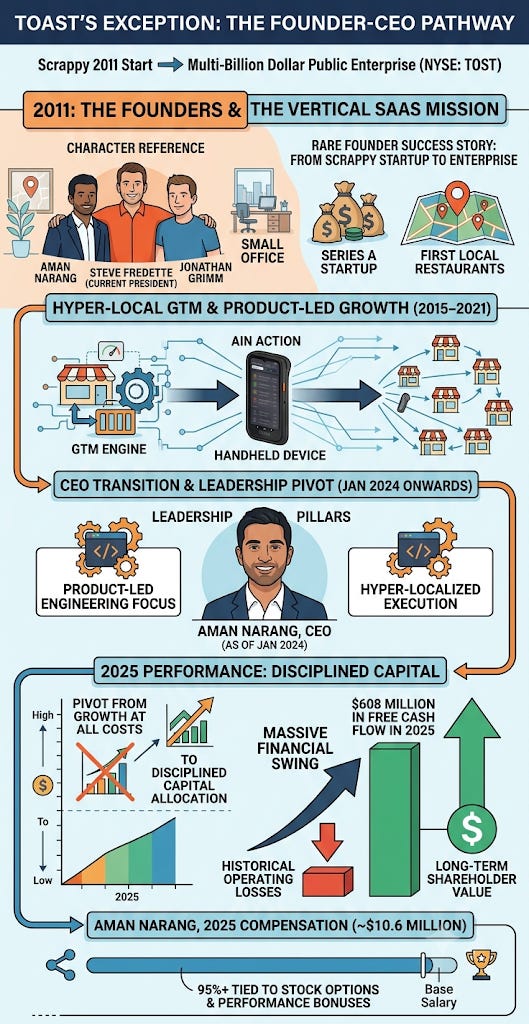

2011 – 2013: The Founding & The Pivot

Founded by Steve Fredette, Aman Narang, and Jonathan Grimm (former Endeca employees), Toast initially launched in 2011 as a consumer-facing app for mobile payments and loyalty. Realizing restaurants needed a holistic solution rather than just another consumer app, they executed a massive strategic pivot in 2013. They built an Android-based cloud POS from the ground up, deliberately utilizing cheaper hardware to lower the barrier to entry and undercut proprietary legacy competitors.

2015 – 2018: Scaling the GTM Engine

Backed by a $30M Series A from Bessemer and GV in 2015, Toast built a localized, “feet on the street” sales force. They didn’t just sell software; they sold localized restaurant operations. By 2017, they introduced Toast Go, an industry-first, purpose-built handheld POS device. This aggressive hardware-software expansion pushed them to unicorn status ($1.4B valuation) in 2018.

2020: The COVID-19 Crucible

The pandemic devastated the restaurant industry. Toast laid off 50% of its workforce in April 2020 as dining rooms shut down globally. However, the company rapidly shipped Toast Now, a suite enabling digital ordering, curbside pickups, and flat-fee delivery integrations. This critical pivot kept their clients afloat, accelerated the industry’s digital transition, and drove Toast’s valuation back up to $8 billion by November of that same year.

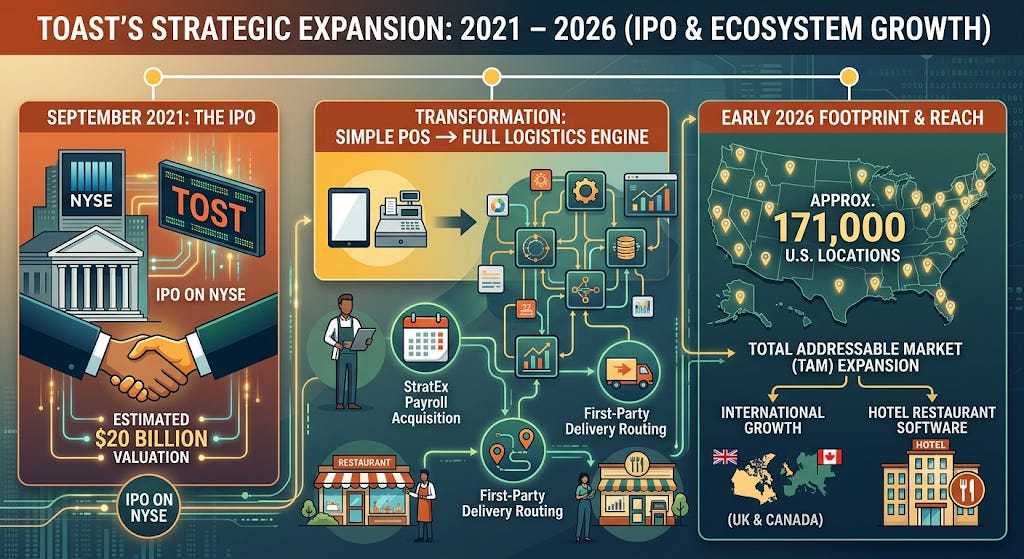

2021 – 2026: IPO & Ecosystem Expansion

Toast went public (NYSE: TOST) in September 2021 at a roughly $20 billion valuation. Since the IPO, they have transitioned from a simple POS to a full “logistics engine,” acquiring companies like StratEx for payroll and integrating first-party delivery routing. As of early 2026, Toast has grown its footprint to serve approximately 171,000 U.S. locations, and has expanded its total addressable market through international growth in the UK and Canada, as well as pushing into hotel restaurant software.

The Logistics OS

To understand Toast's dominance, you have to look at how they construct their ecosystem. They didn't build a software suite; they built a "Logistics OS" designed to replace a fragmented mess of 5 to 7 different vendors that restaurants historically relied on.

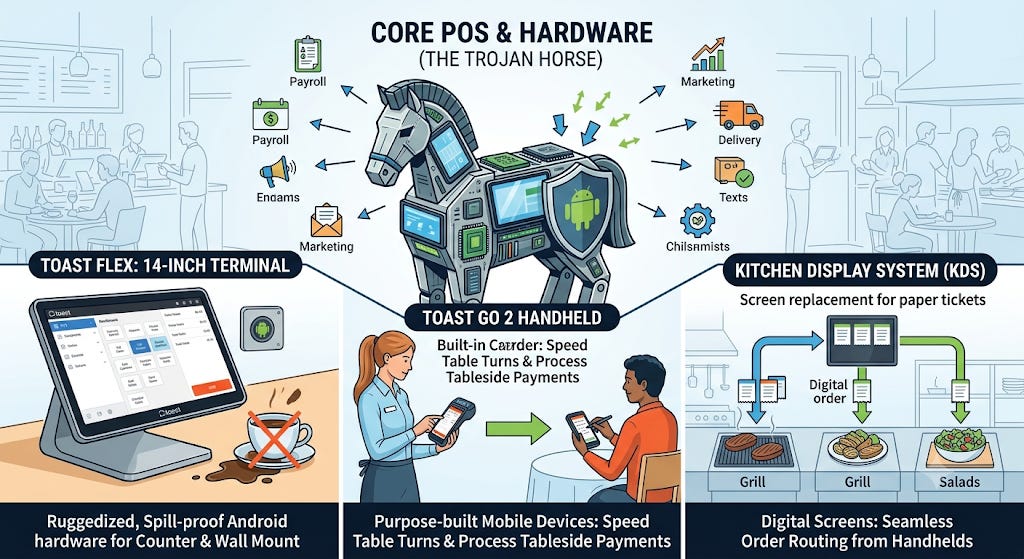

The Trojan Horse: Core POS & Hardware

Everything starts at the point of sale. Unlike competitors who rely on iPads, Toast built their system entirely on Android. This gave them the flexibility to create ruggedized, spill-proof, restaurant-specific hardware.

Toast Flex: The 14-inch terminal used at the counter or mounted on walls.

Toast Go 2 Handhelds: Purpose-built mobile devices with built-in card readers that allow servers to take orders and process payments tableside. This drastically speeds up table turns and is a massive selling point for full-service restaurants.

Kitchen Display System (KDS): Digital screens that replace paper tickets, seamlessly routing orders from the handhelds straight to the right prep stations.

Front-of-House & Digital Ordering

Once Toast owned the physical transaction, they aggressively expanded into the digital guest experience — cutting out expensive third-party platforms where possible.

Toast Online Ordering & TakeOut App: A commission-free digital storefront that allows restaurants to take online orders directly, circumventing the 30% fees charged by Uber Eats and DoorDash.

Toast Delivery Services: If a restaurant doesn’t have its own drivers, Toast dispatches flat-fee drivers from third-party networks to fulfill direct orders, allowing the restaurant to keep the customer data.

Marketing & Loyalty: Integrated tools that capture guest emails and phone numbers at the point of payment, triggering automated campaigns and point-based rewards.

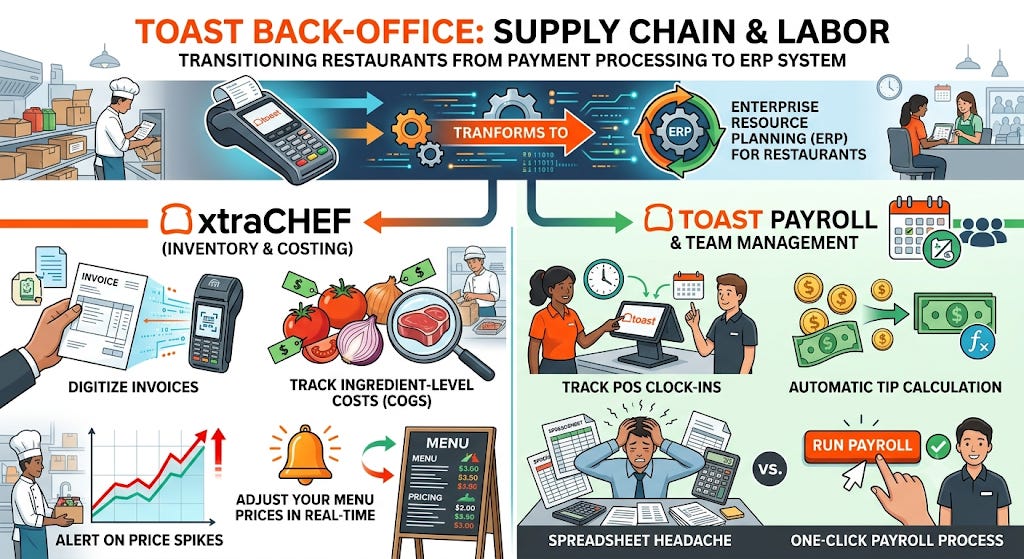

Back-Office: Supply Chain & Labor

This is where Toast transitions from a payment processor into an enterprise resource planning (ERP) system for restaurants.

xtraCHEF (Inventory & Costing): An acquisition that gave Toast deep supply chain capabilities. It digitizes invoices, tracks ingredient-level costs (Cost of Goods Sold), and alerts operators if the price of a specific ingredient spikes so they can adjust menu prices in real-time.

Toast Payroll & Team Management: Integrated scheduling and payroll modules. Because Toast already tracks when employees clock in on the POS, and automatically calculates tips at the end of the shift, running payroll becomes a one-click process rather than a multi-hour spreadsheet headache.

The Fintech Engine: Capital & Payments

While the software is impressive, Fintech is the financial engine of the company.

Payment Processing: Toast operates on a payment-facilitator model. They require customers to use their processing (typically locking in rates around 2.49% + 15¢). Because they process billions of dollars in Gross Payment Volume (GPV), this is their primary revenue driver.

Toast Capital: Because Toast sees every dollar that flows through the restaurant every day, their underwriting models are incredibly accurate. They offer working capital loans to restaurants to cover renovations or slow seasons, taking a fixed percentage of daily POS sales until the loan is repaid.

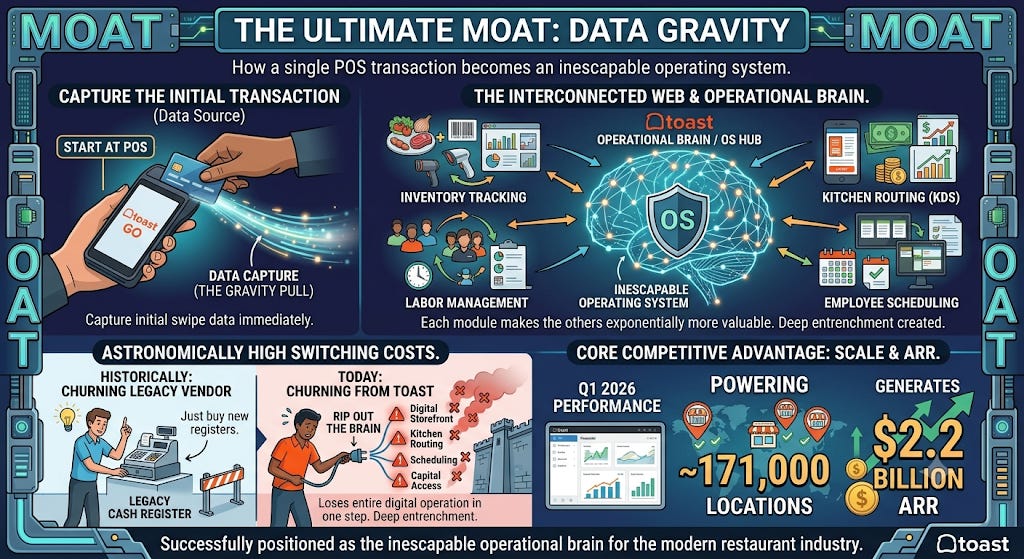

The Ultimate Moat: Data Gravity

When you look at Toast’s entire ecosystem — from the initial swipe on a Toast Go handheld to the automated payroll run in the back office — the overarching strategy becomes clear: data gravity.

By capturing the initial transaction at the point of sale, Toast seamlessly feeds that data into inventory tracking, labor management, and capital underwriting. They didn’t just build a software suite; they built an interconnected web where each module makes the others exponentially more valuable.

This architecture creates astronomically high switching costs. Historically, for a restaurant operator, churning from a legacy vendor just meant buying new cash registers. Today, churning from Toast means ripping out the operational brain of the business. An operator leaving the ecosystem loses their digital storefront, their kitchen routing, their employee scheduling, and their working capital access all at once.

This deep entrenchment is the core of their competitive advantage. It is exactly why, as of Q1 2026, Toast has successfully scaled to power approximately 171,000 locations and generates $2.2 billion in Annualized Recurring Run-Rate (ARR). They aren’t just processing payments; they have successfully positioned themselves as the inescapable operating system for the modern restaurant industry.

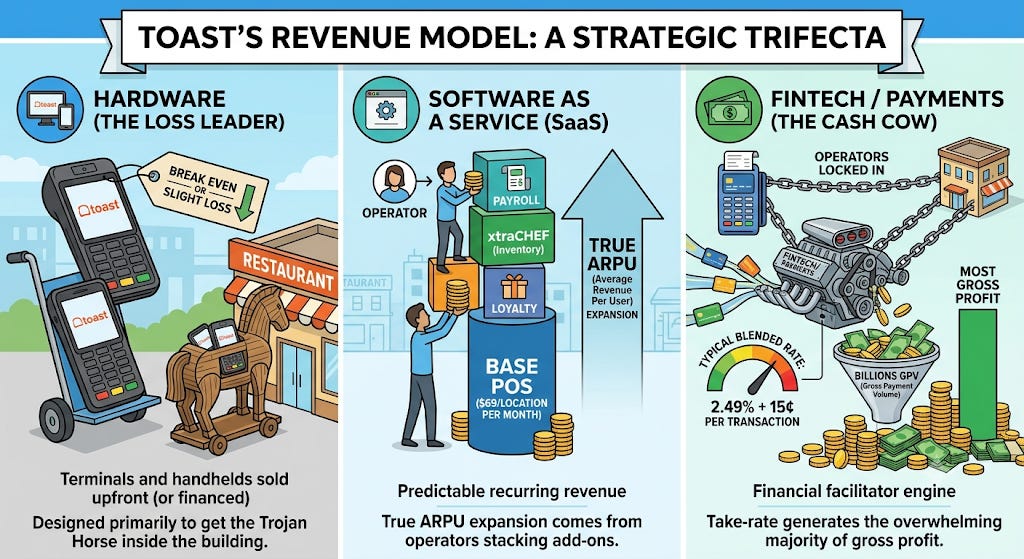

The Business Model: Monetizing the Ecosystem

To evaluate Toast from an equity research perspective, you have to look at their revenue mix. They operate a hybrid pricing model that monetizes the restaurant at three distinct touchpoints.

Hardware (The Loss Leader): Toast typically breaks even or takes a slight loss on their initial hardware deployments. Terminals and handhelds are sold upfront (or financed), designed primarily to get the Trojan Horse inside the building.

Software as a Service (SaaS): This is the predictable recurring revenue. The base POS software starts around $69 per location per month, but the true ARPU (Average Revenue Per User) expansion comes from operators stacking add-ons like Payroll, xtraCHEF (inventory), and Loyalty programs.

Fintech / Payments (The Cash Cow): This is the financial engine. Toast is a payment facilitator, meaning operators are locked into using Toast for card processing. They typically charge a blended rate of 2.49% + 15¢ per in-person transaction. Because Toast processes billions in Gross Payment Volume (GPV), this take-rate generates the overwhelming majority of their gross profit.

Analyst Insight: Toast’s pricing power is immense due to high switching costs, but it isn’t infinite. In 2023, Toast attempted to add a mandatory $0.99 fee to customer online orders to boost revenue. The operator backlash was so severe that management had to roll the fee back within weeks. It was a massive stress test that proved while restaurants won’t churn over software price increases, they will revolt if you tax their direct consumer relationships.

The Competitive Landscape: Who is Toast Eating?

The point-of-sale (POS) and restaurant management industry remains fragmented, but the market has clearly segmented into distinct competitive lanes. While Toast is the undisputed heavyweight in the independent, full-service restaurant (FSR) category, they face strategic battles on both the lower and upper ends of the market.

1. The Micro-Merchant Market: Square (Block)

Core Market: Cafes, food trucks, and single-location micro-SMBs.

The Toast Advantage: Deep, restaurant-specific operational workflows. Toast excels at complex floor mapping, table coursing (appetizer vs. entree timing), and multi-station Kitchen Display System (KDS) routing.

The Vulnerability: Square has a significantly lower barrier to entry, offering transparent, flat-rate pricing with zero monthly software fees for basic tiers and cheaper, widely available hardware. Square dominates the “day-one” entrepreneur.

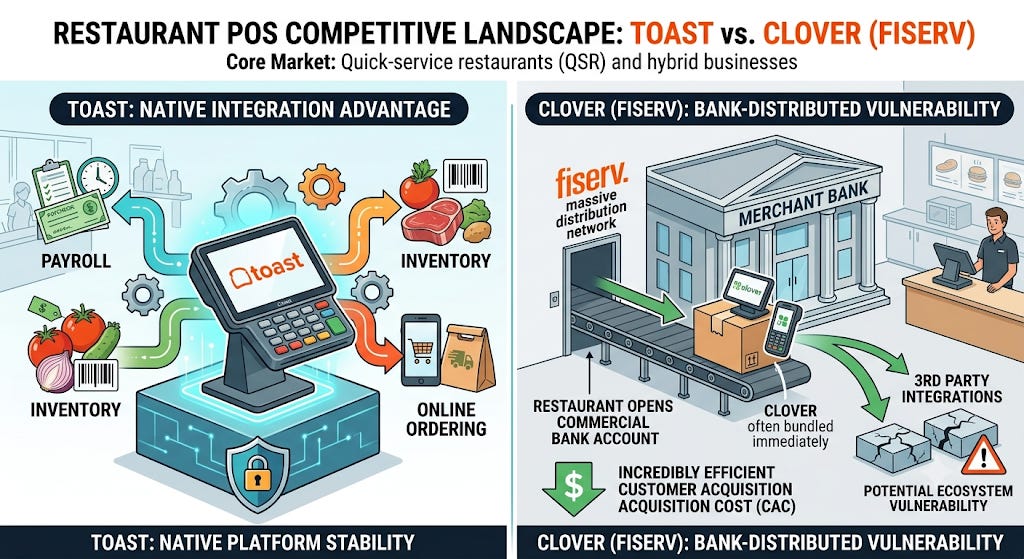

2. The Bank-Distributed Alternative: Clover (Fiserv)

Core Market: Quick-service restaurants (QSR) and hybrid retail/food businesses.

The Toast Advantage: A deeply integrated, native software ecosystem. Toast builds its core modules (payroll, inventory, online ordering) in-house, ensuring absolute platform stability.

The Vulnerability: Clover is distributed natively through merchant banks via Fiserv’s massive distribution network. When a restaurant opens a commercial bank account, Clover is often bundled in immediately, giving them an incredibly efficient customer acquisition cost (CAC) channel.

3. The Multi-Location Challenger: Lightspeed

Core Market: Fine dining, complex multi-location groups, and hybrid hospitality.

The Toast Advantage: Scale of the domestic footprint and a hyper-localized U.S. sales force. Toast’s “feet on the street” model provides unmatched implementation support.

The Vulnerability: Lightspeed boasts highly sophisticated multi-location accounting, deep inventory matrices, and multi-currency capabilities that appeal heavily to high-end hospitality groups and international operators.

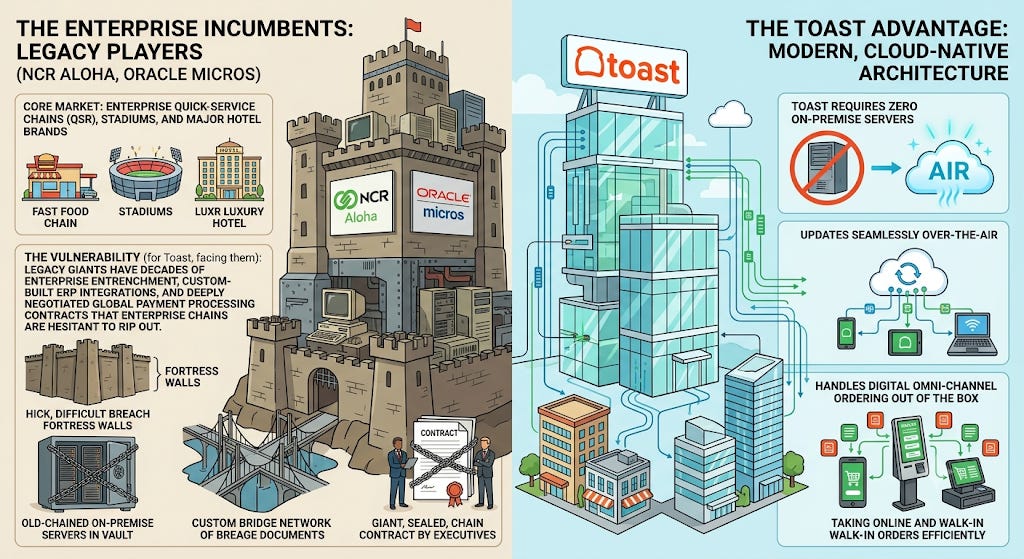

4. The Enterprise Incumbents: Legacy Players (NCR Aloha, Oracle Micros)

Core Market: Enterprise Quick-Service Chains (QSR), stadiums, and major hotel brands.

The Toast Advantage: Modern, cloud-native architecture. Toast requires zero on-premise servers, updates seamlessly over-the-air, and handles digital omni-channel ordering out of the box.

The Vulnerability: Legacy giants have decades of enterprise entrenchment, custom-built ERP integrations, and deeply negotiated global payment processing contracts that enterprise chains are hesitant to rip out.

Market Dynamics by Segment: The Land Grab

The Downmarket Guardrail: Square rules the small cafe and food truck crowd. It is frictionless to set up, but once a restaurant scales past $1 million in annual revenue and requires advanced operational logic, Square’s restaurant features can feel bolted-on. Toast regularly poaches these graduating clients.

The Mid-Market Moat: This is Toast’s absolute sweet spot. Clover relies heavily on a third-party app store to fulfill advanced restaurant needs, which creates a disjointed UX and siloed data for the operator. Toast’s closed, Apple-like ecosystem ensures that frontline data flows automatically to the back office without integration friction.

The Enterprise Frontier: To justify its valuation multiples, Toast is aggressively moving upmarket to hunt enterprise “whales” (50+ location chains). The pitch to these enterprise legacy users is simple: remove expensive on-premise hardware maintenance, transition completely to the AWS cloud, and consolidate a fragmented vendor stack of 10+ software solutions into Toast’s single operating system.

Management & Leadership: The Founders at the Helm

In the vertical SaaS industry, it is relatively rare to see the original founders successfully transition a company from a scrappy Series A startup to a multi-billion dollar publicly traded enterprise. Toast is the exception.

The company is led by Aman Narang, who co-founded Toast in 2011 alongside Steve Fredette (current President) and Jonathan Grimm. Narang, after serving as Co-President for over a decade, officially stepped into the CEO role in January 2024.

Narang’s leadership style is deeply rooted in product engineering and hyper-localized go-to-market execution. His compensation package—which was roughly $10.6 million in 2025—is over 95% tied to stock options and performance bonuses, heavily aligning his incentives with long-term shareholder value. Under his tenure as CEO, the company has explicitly pivoted from a “growth at all costs” mentality toward disciplined capital allocation, delivering a massive swing from historical operating losses to $608 million in free cash flow in 2025.

2026 Strategic Initiatives: Expanding the TAM

For years, the bear case against Toast was that they would eventually hit a saturation point in the U.S. independent restaurant market. To combat this, Narang and the management team have outlined a highly aggressive playbook for 2026 to expand their Total Addressable Market (TAM).

Management expects 20% to 22% growth in recurring gross profit for 2026. Here is how they plan to achieve it:

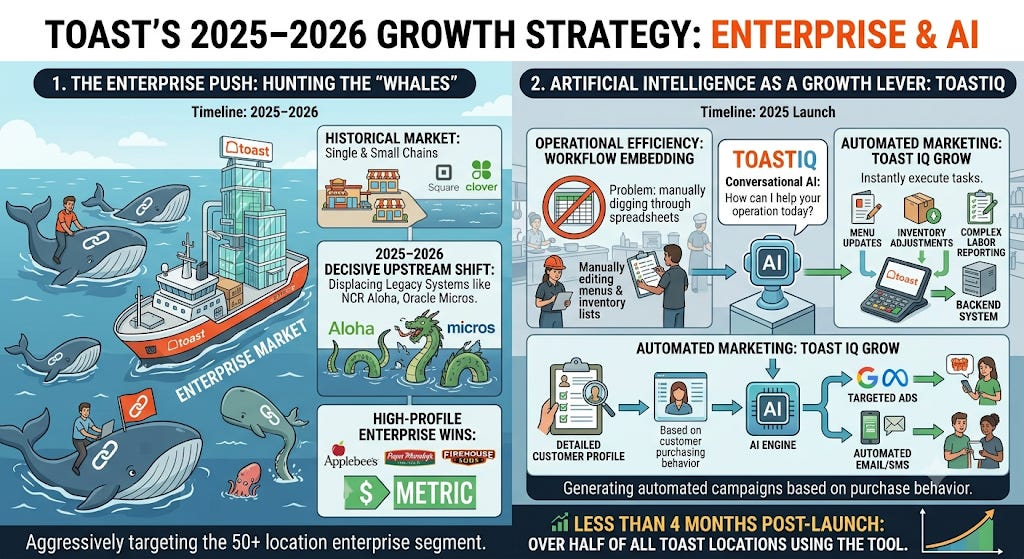

1. The Enterprise Push (Hunting the “Whales”)

Historically, Toast won by out-competing Square and Clover in the single-location or small-chain market. In 2025 and 2026, their focus has decisively shifted upmarket. They are aggressively targeting the 50+ location enterprise segment to displace legacy systems like NCR Aloha and Oracle Micros. This is already bearing fruit, with recent high-profile enterprise wins including Applebee’s, Papa Murphy’s, and Firehouse Subs.

2. Artificial Intelligence as a Growth Lever (ToastIQ)

Toast is not just treating AI as a buzzword; they are embedding it directly into the restaurant’s operational workflows. In 2025, they launched ToastIQ, an integrated conversational AI assistant.

Operational Efficiency: Instead of manually digging through spreadsheets, operators can use ToastIQ to instantly execute tasks like menu updates, inventory adjustments, and complex labor reporting.

Automated Marketing (Toast IQ Grow): The AI engine helps restaurants build targeted ad campaigns across Google and Meta, generating automated email/SMS campaigns based on customer purchasing behavior. Less than four months post-launch, over half of all Toast locations were actively using the tool.

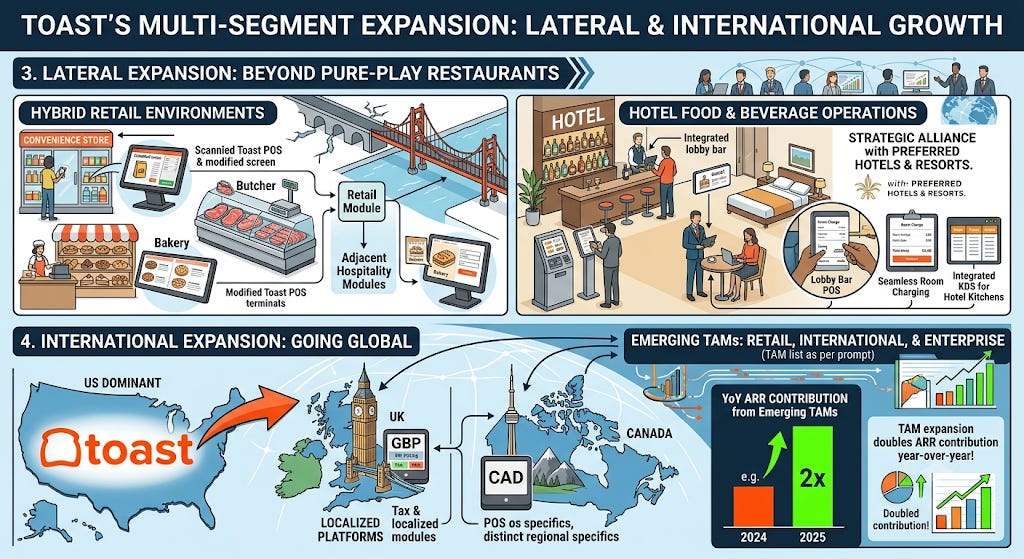

3. Lateral Expansion: Retail & Hotels

Toast is officially breaking out of pure-play restaurants. They are modifying their software to cater to adjacent hospitality segments. This includes hybrid retail environments (convenience stores, butcher shops, bakeries) and hotel food & beverage operations, recently forming a strategic alliance with Preferred Hotels & Resorts.

4. International Expansion

Toast’s dominance has historically been confined to the United States. They have now launched localized platforms in the UK and Canada, with management noting that their emerging TAMs (retail, international, and enterprise) successfully doubled their Annual Recurring Revenue (ARR) contribution year-over-year.

Analyst Insight: The enterprise and retail expansion strategies are brilliant, but they bring new risks. Enterprise clients demand deep custom integrations and take significantly longer to close, which increases Toast’s Customer Acquisition Cost (CAC). Additionally, management recently flagged that supply chain pressures, specifically higher memory chip costs for their hardware, will act as a margin headwind in the second half of 2026. Watch the margins closely over the next two quarters.

The Financials: From Cash Burn to a Cash Cannon

For years, the Wall Street narrative on Toast was identical to many other hyper-growth vertical SaaS companies: massive revenue growth funded by unsustainable cash burn. But between 2024 and 2026, Toast completely flipped the script. The company has aggressively scaled into self-funded profitability, proving that their “land and expand” model produces real operating leverage once a critical mass of locations is reached.

Revenue & Top-Line Growth

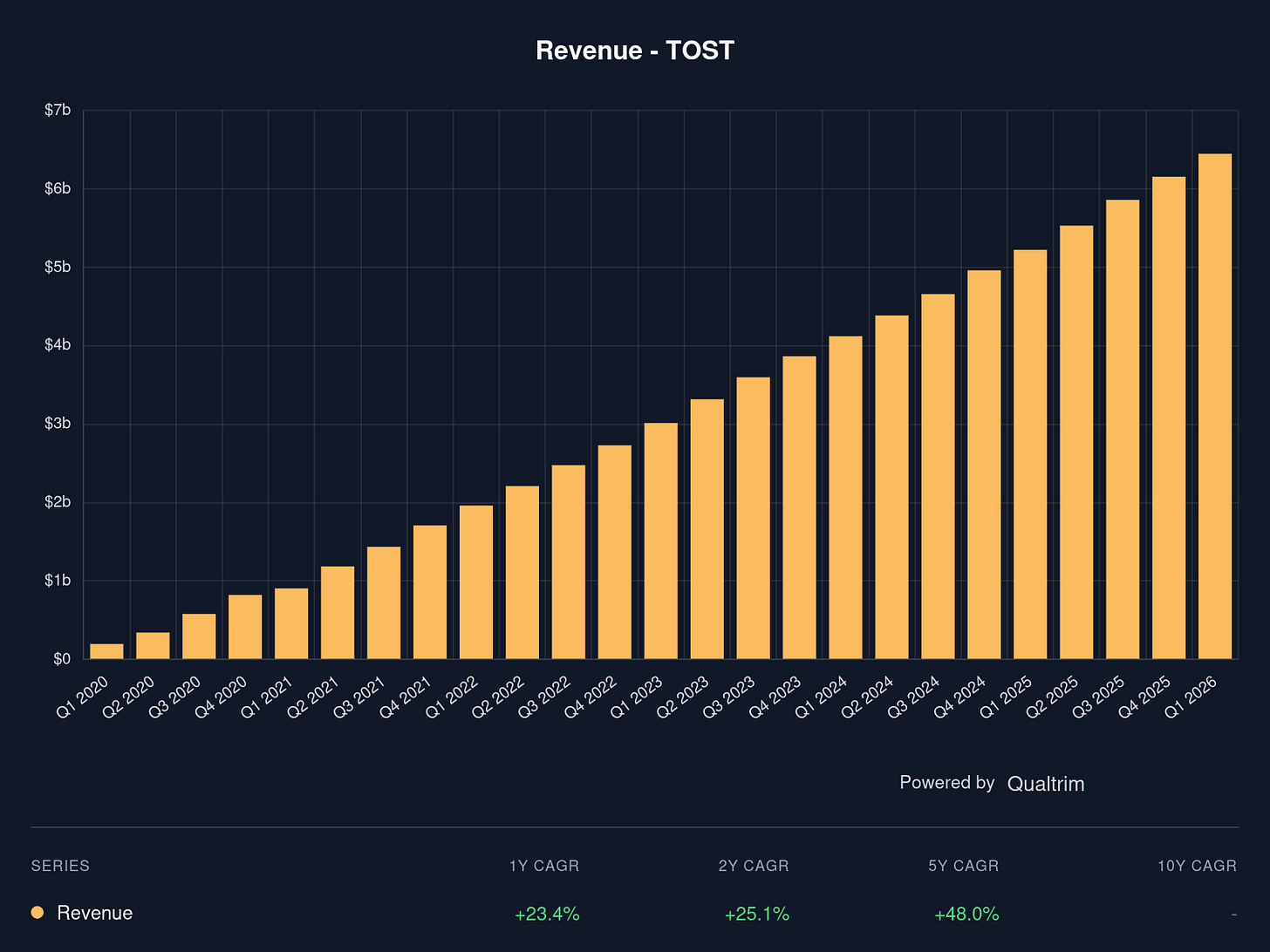

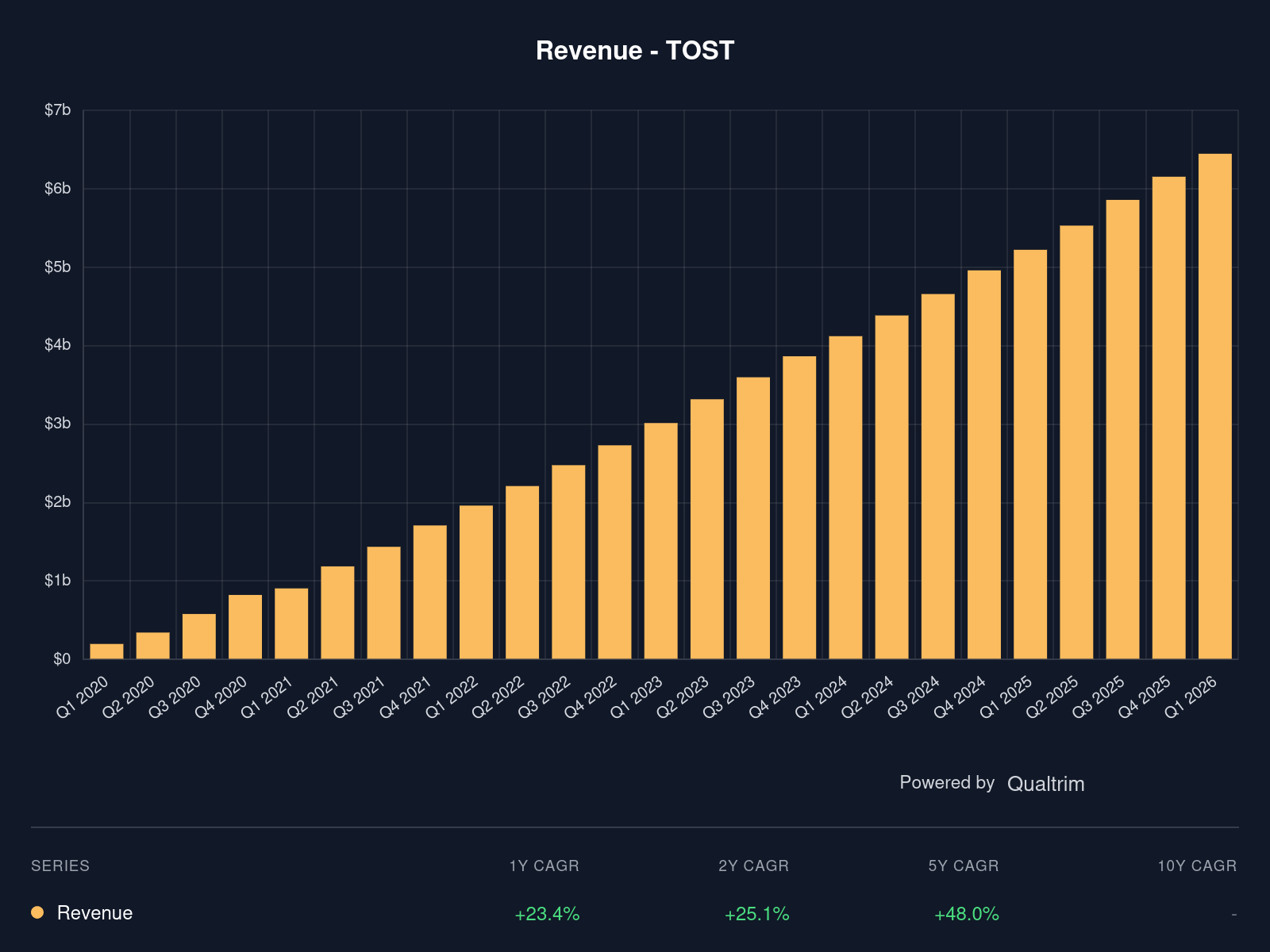

Toast’s top line continues to grow at a blistering pace despite their increasing scale.

Total Revenue: In Q1 2026, total revenue reached $1.63 billion, a 22% year-over-year increase.

Annualized Recurring Run-Rate (ARR): This is the metric management cares about most. ARR hit $2.2 billion as of March 2026, up 26% YoY. This growth was driven both by adding roughly 7,000 net new locations in the quarter (reaching 171,000 total locations) and operators adopting more software modules.

Gross Payment Volume (GPV): Toast processed $51.3 billion in payments in Q1 2026 alone (up 22%), demonstrating how deeply entrenched they are in the daily cash flow of the U.S. restaurant industry.

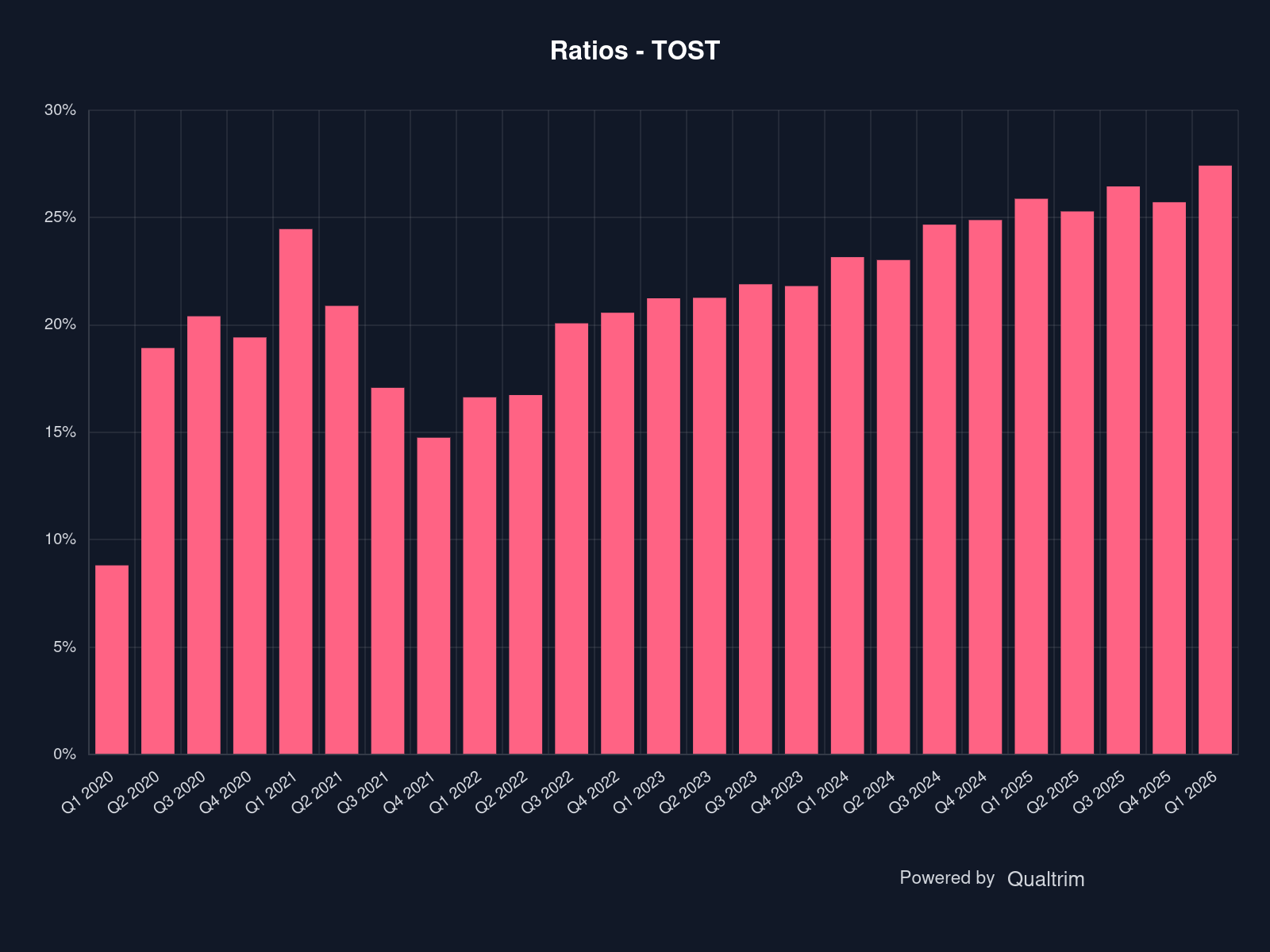

Profitability & Margins (The Inflection Point)

The most important shift in Toast’s financial profile is the translation of top-line scale into bottom-line profits.

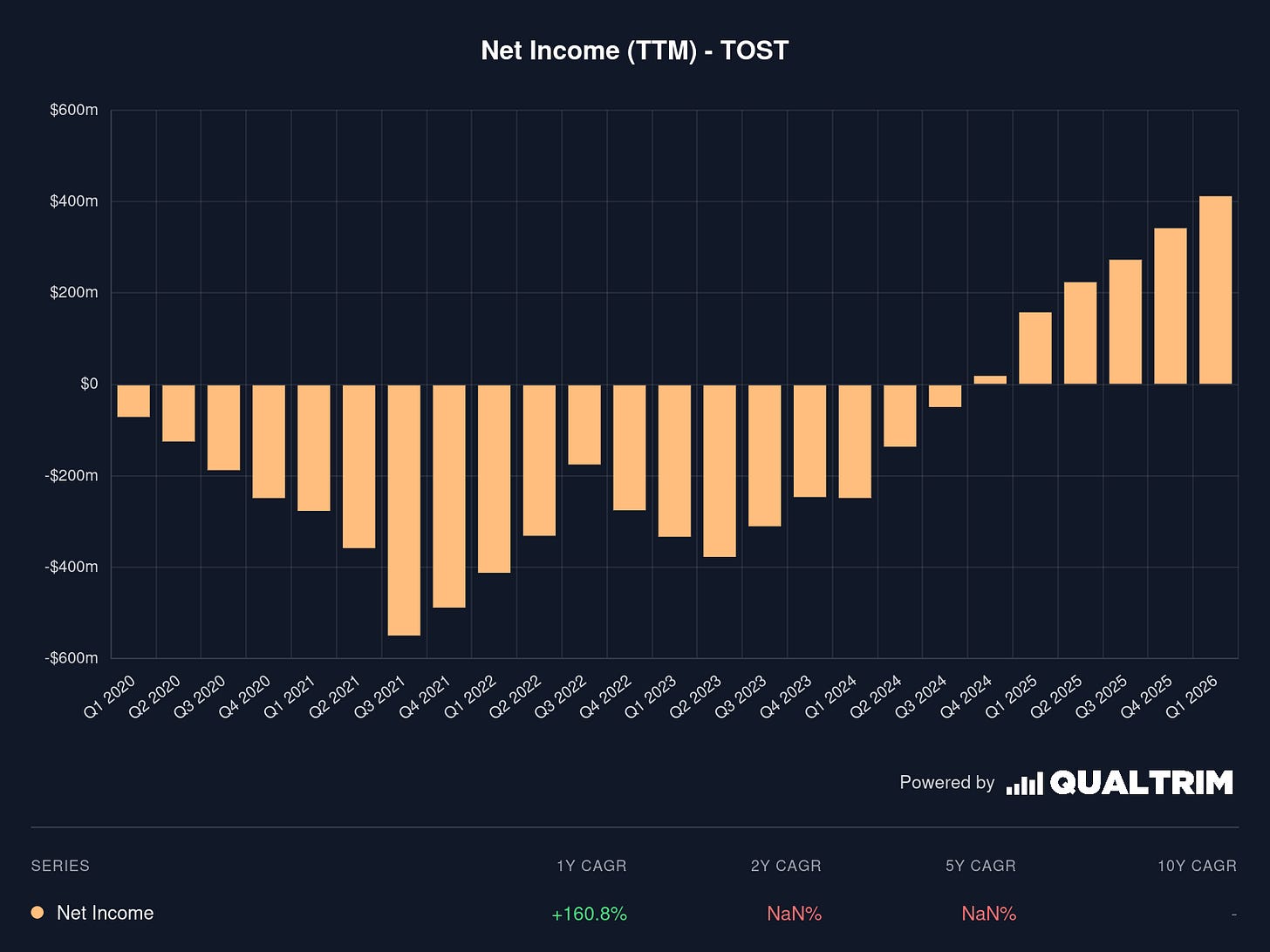

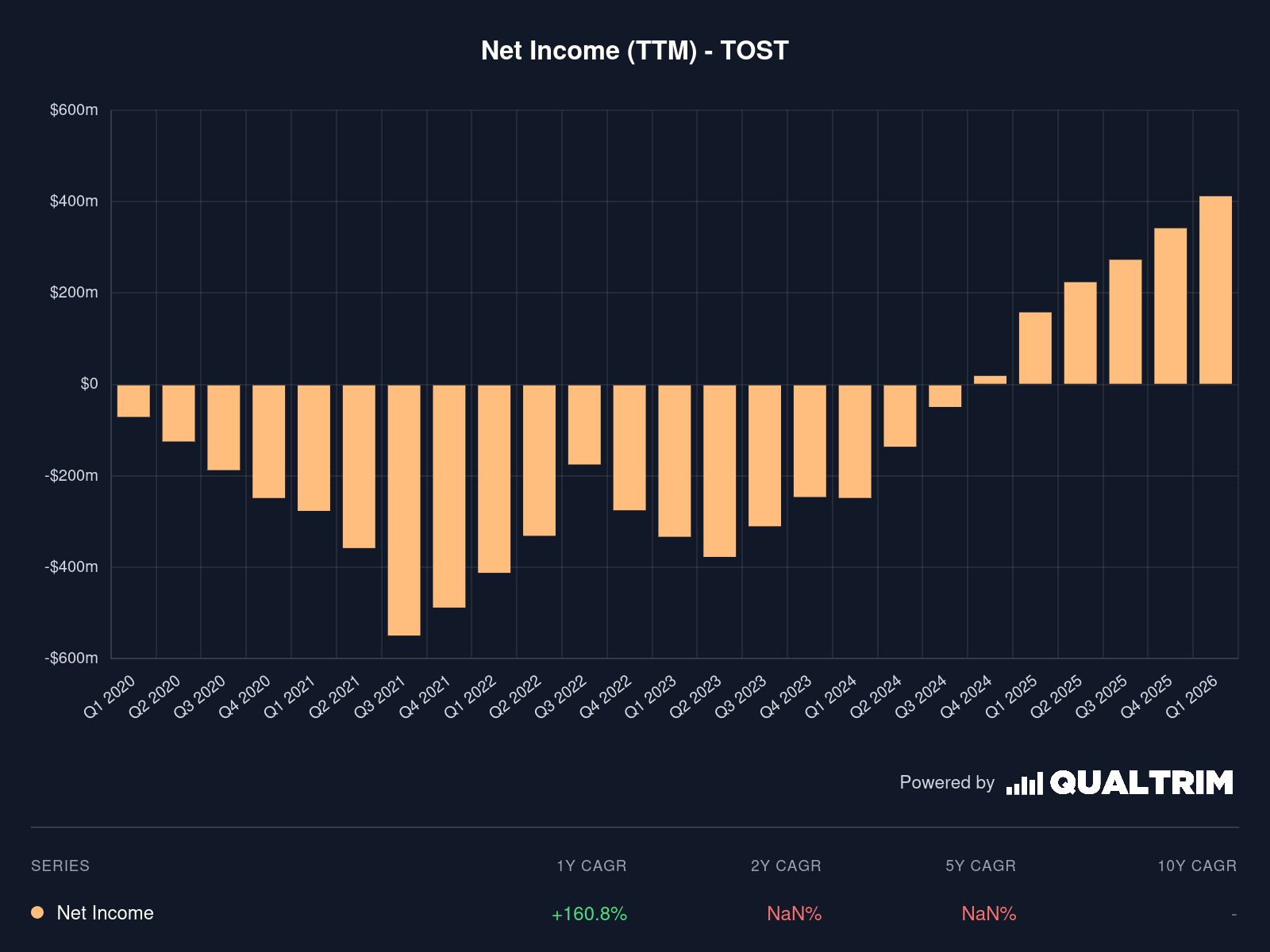

Net Income: Toast posted $342 million in GAAP net income for the full year 2025. In Q1 2026, net income more than doubled year-over-year to $126 million (up from $56 million in Q1 2025), representing a diluted EPS of $0.20.

Adjusted EBITDA: Management has shown fierce discipline in operating expenses. Adjusted EBITDA for Q1 2026 came in at $179 million (up from $133 million the prior year), and they have raised their full-year 2026 guidance to target roughly $800 million in Adjusted EBITDA.

Margin Expansion: Operating income margin expanded significantly in Q1 2026, driven by a 27% growth in core recurring gross profits. Because they rely heavily on automated tools (like the newly launched ToastIQ) for customer onboarding and support, their sales and marketing spend is growing much slower than their revenue.

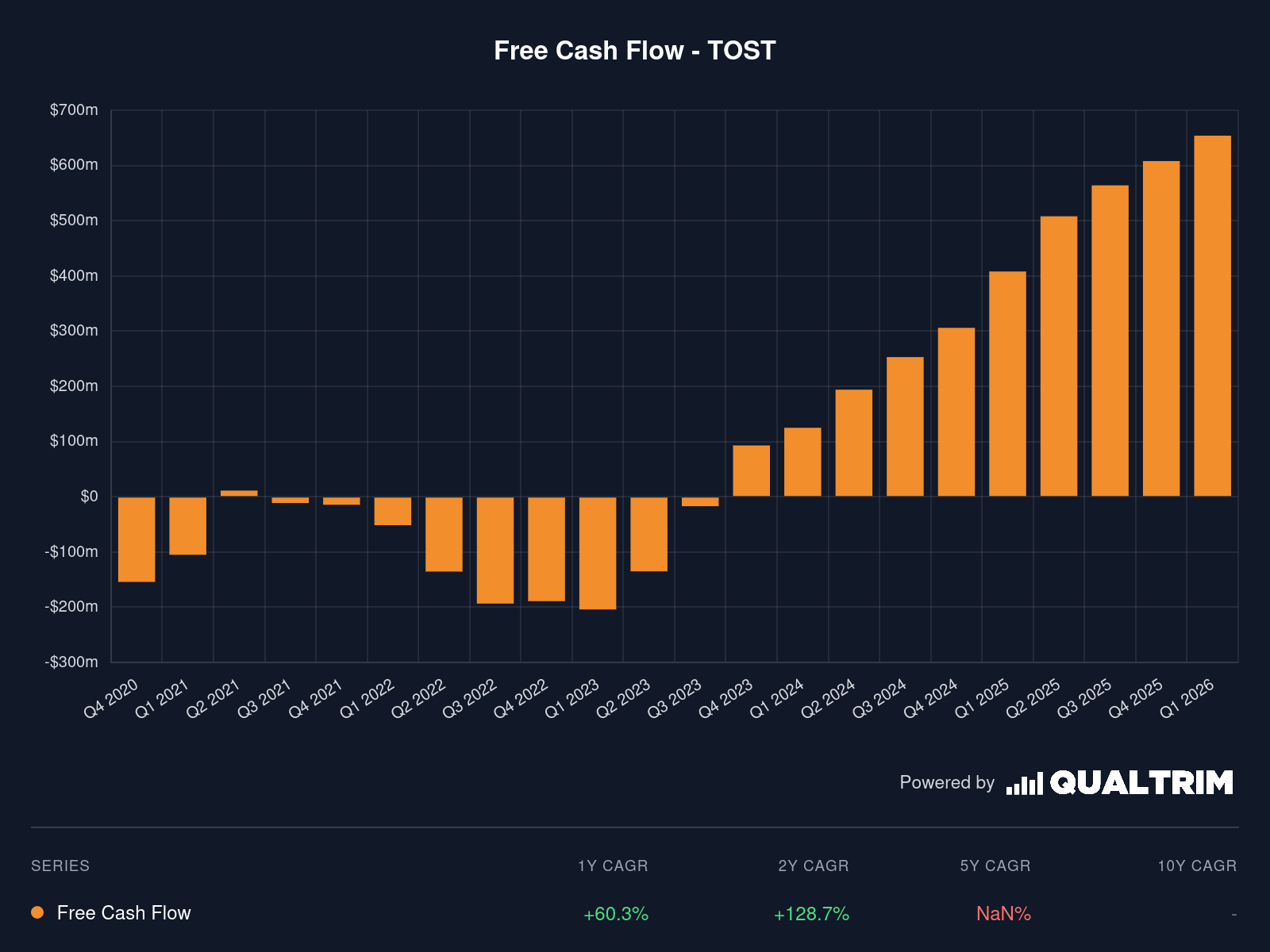

Free Cash Flow (FCF)

Scale is finally translating into spendable cash.

In FY2023, Toast generated just $93 million in Free Cash Flow.

By the end of FY2025, FCF exploded to $608 million.

The momentum continued into Q1 2026 alone the company generated $115 million in FCF, completely self-funding their growth without needing to tap debt markets.

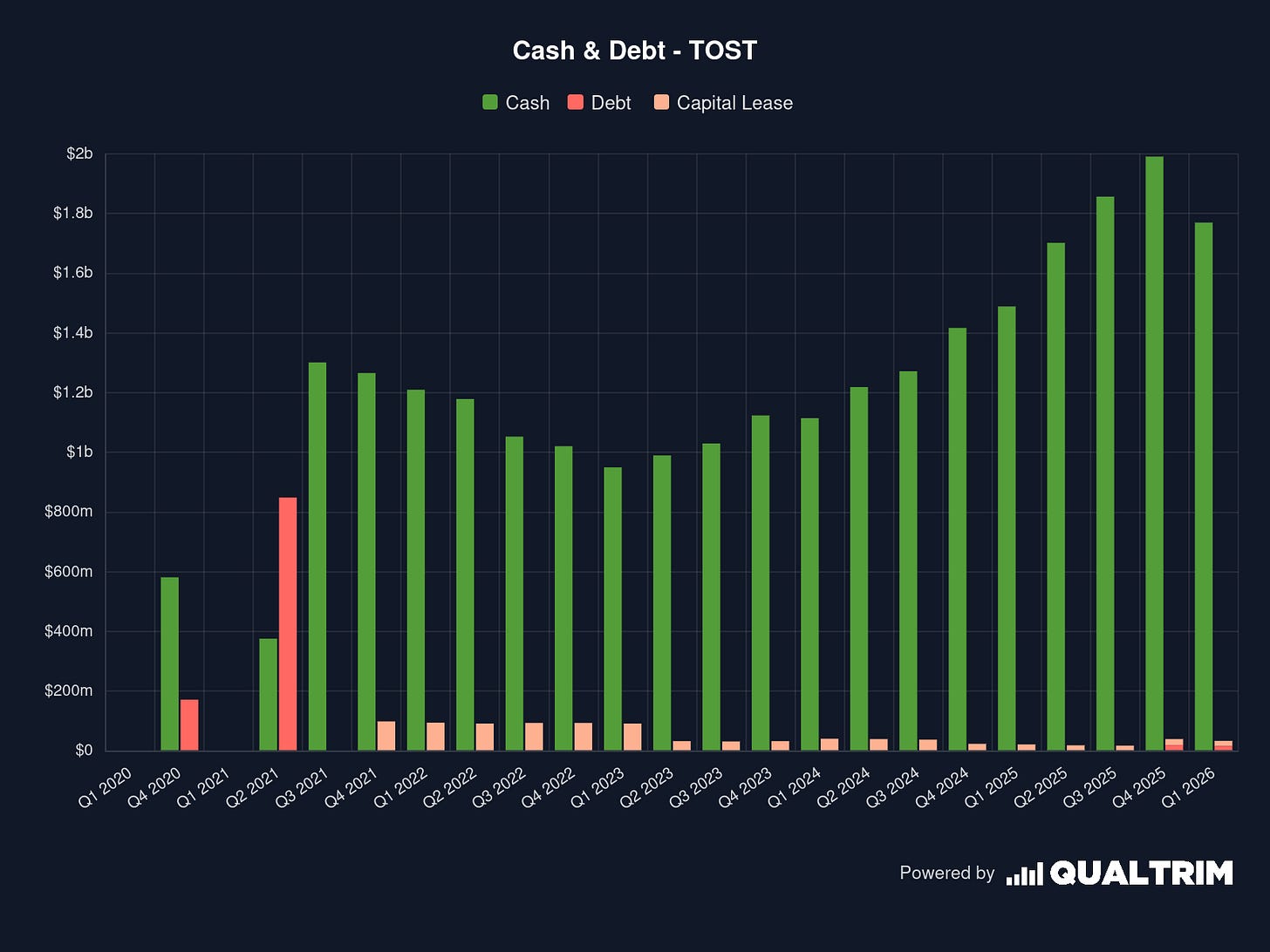

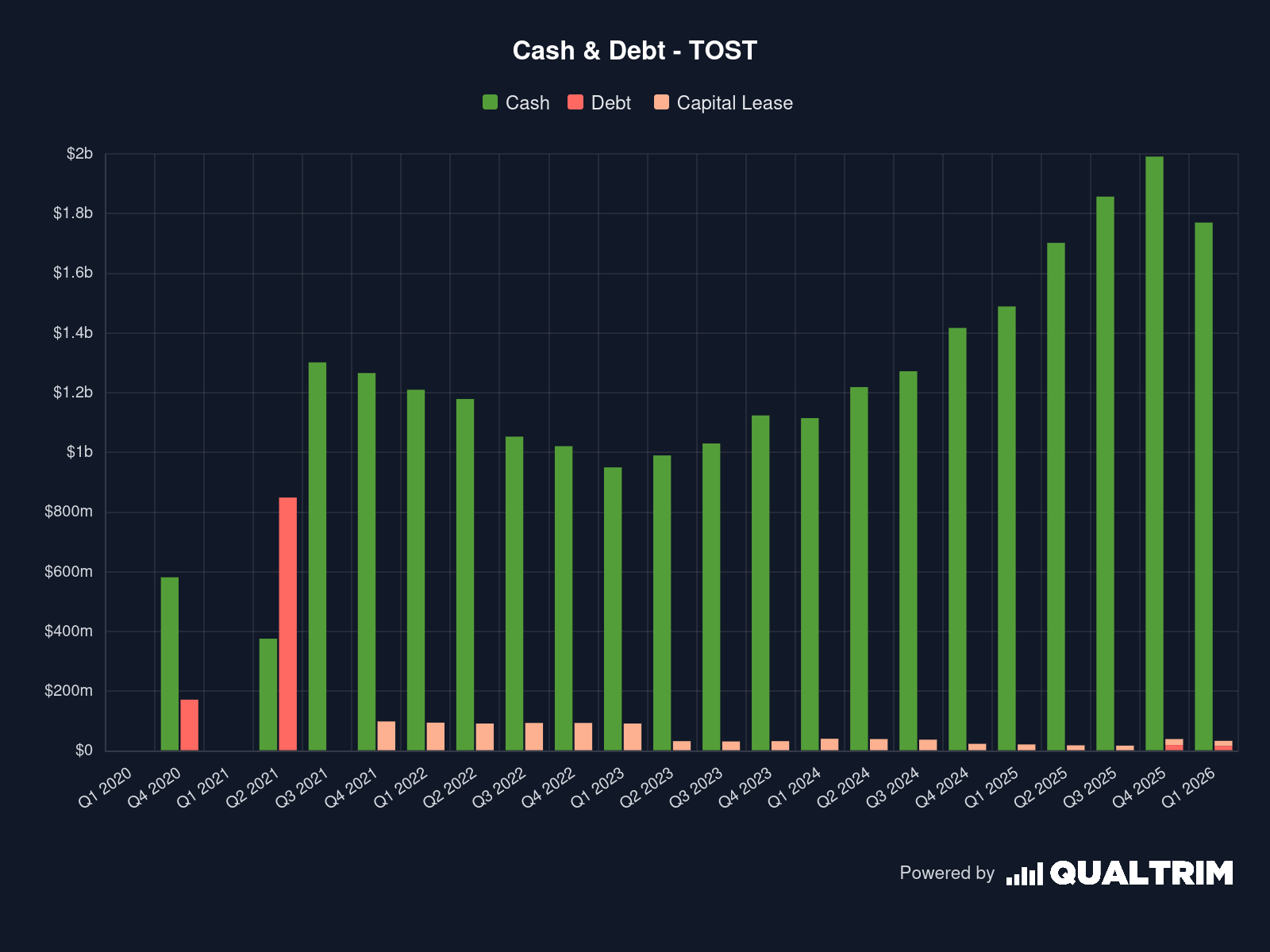

Balance Sheet & Shareholder Returns

Toast operates with a “fortress” balance sheet, heavily de-risking the investment for equity holders.

Liquidity: As of March 31, 2026, the company held $1.77 billion in cash, cash equivalents, and marketable securities, alongside an undrawn $347 million credit facility.

Debt: They carry effectively zero long-term debt, an extreme rarity for a SaaS company of this size.

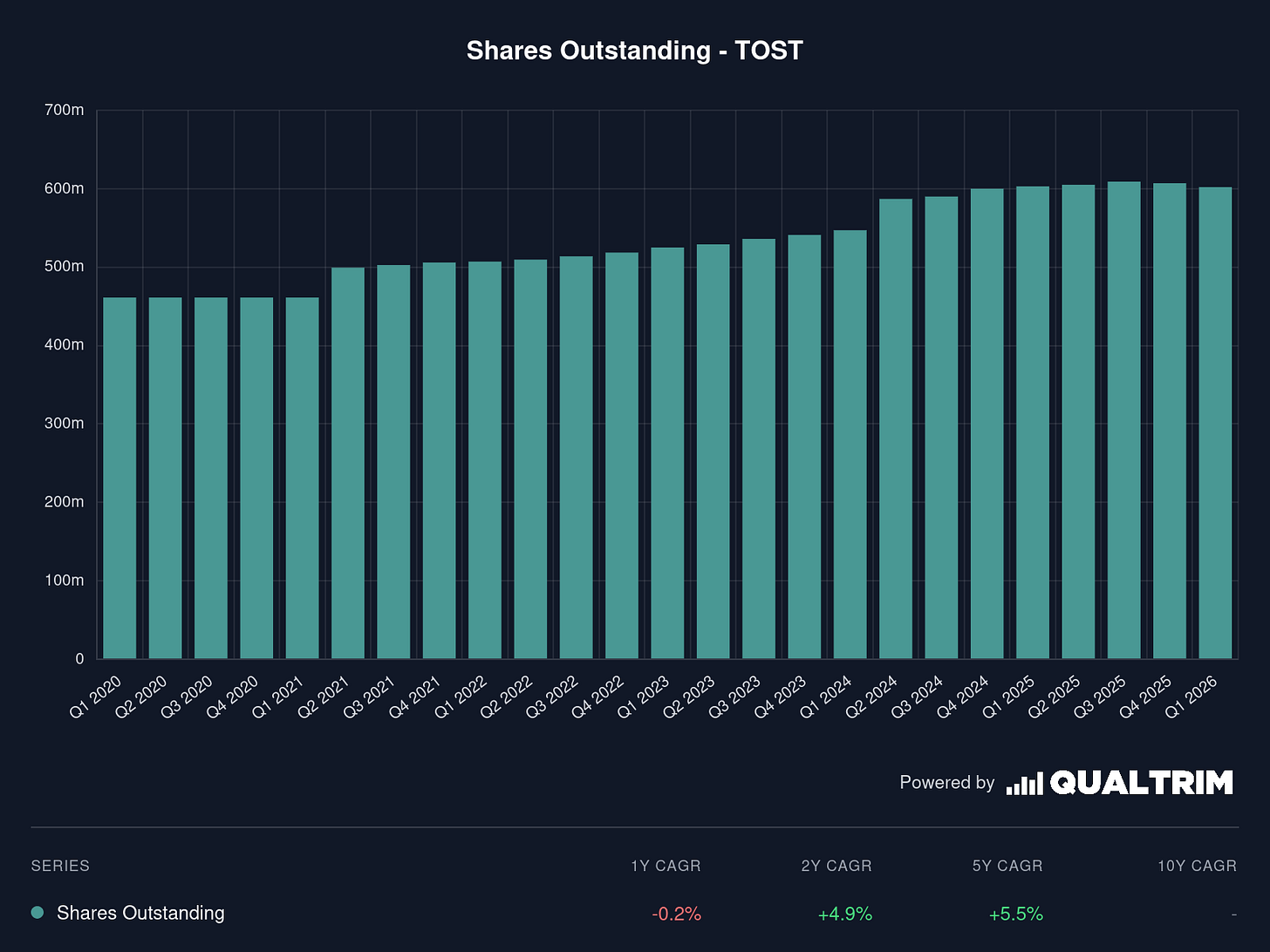

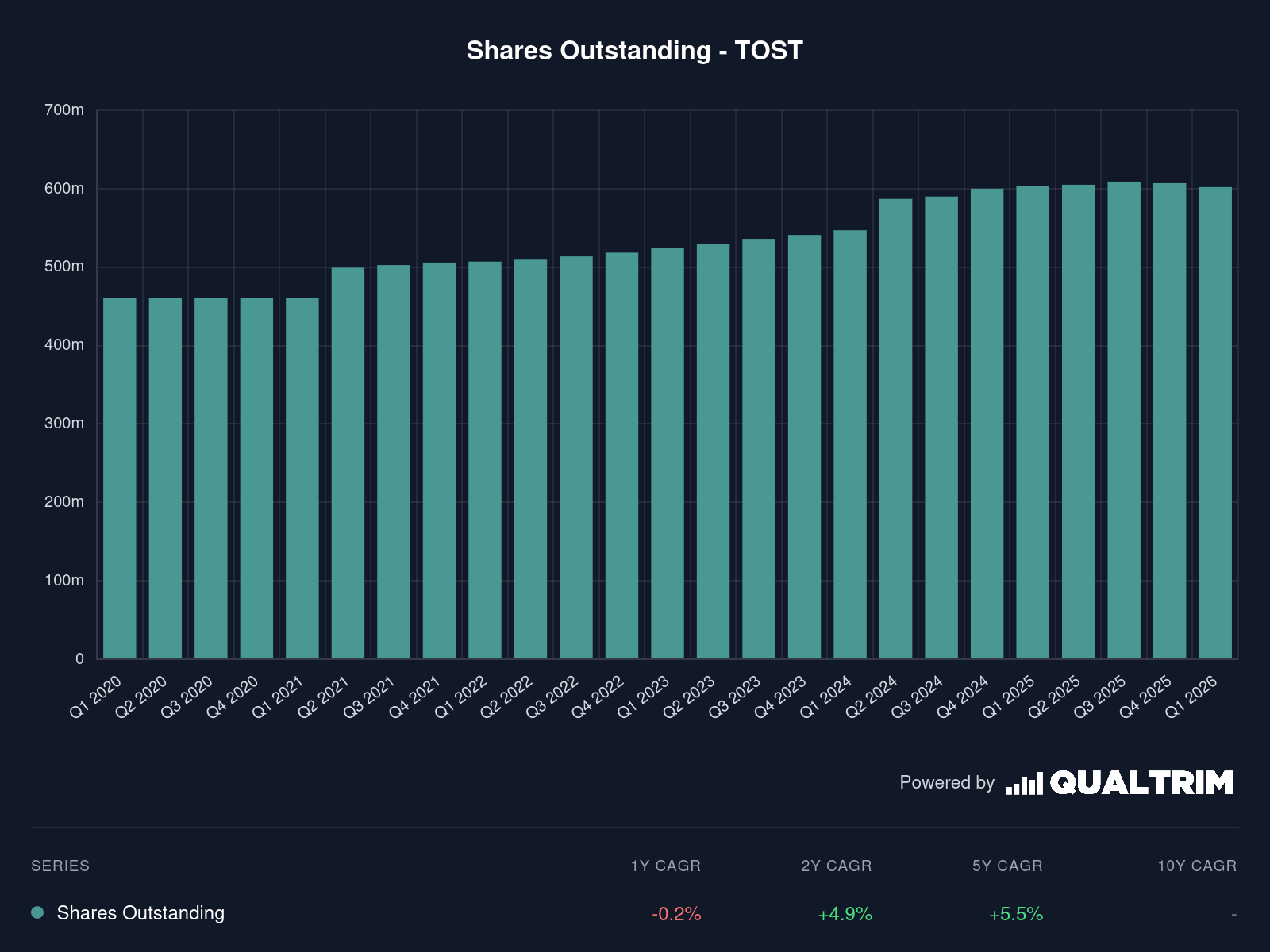

Shares Outstanding & Buybacks: Based on Q1 net income ($126M) and diluted EPS ($0.20), Toast is operating with roughly 630 million diluted shares outstanding. However, management has shifted to an aggressive capital return strategy. Armed with their massive free cash flow, the Board authorized a large share repurchase program, buying back 14 million shares for $378 million year-to-date through early May 2026.

Analyst Insight: The aggressive share buyback is the loudest signal management can send right now. Rather than hoarding their $1.7 billion cash pile or burning it on overpriced acquisitions, buying back nearly $400 million in stock in a single quarter shows management fundamentally believes the public market is undervaluing their future cash flows, and a sign that management is changing its previously dilutive way.

Valuation Framework: Bull, Base, and Bear Cases

To pin down Toast’s intrinsic value, we look at three distinct scenarios modeled using a 5-year valuation framework. Note that while the models utilize the “TTM EPS” label, the earnings metric being tracked is explicitly Stock-Based Compensation Adjusted Free Cash Flow (SBC Adj FCF) per share, which sits at $0.72 today across all scenarios with a current market price of $28.16.

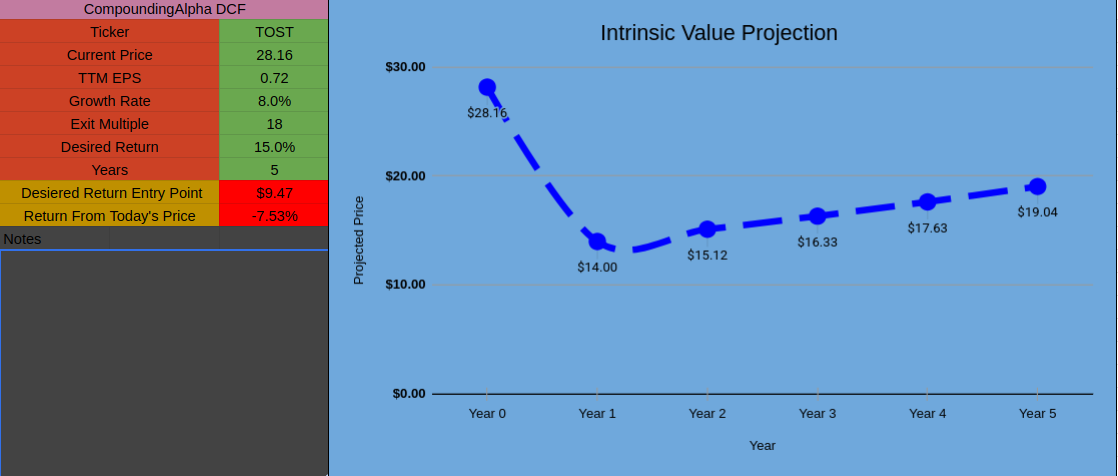

The Bear Case (Saturation & Macro Headwinds)

The bear model illustrates what happens if Toast experiences a sharp slowdown in restaurant additions or a compression of processing take-rates.

Growth Rate: 8.0% CAGR.

Exit Multiple: 18x SBC Adj FCF.

Desired Return Entry Point: $9.47.

Projected 5-Year Price: $19.04.

Expected Annualized Return from Today’s Price: -7.53%.

The Thesis: A broad consumer spending slowdown triggers restaurant bankruptcies, driving up customer churn. Simultaneously, enterprise push failure, hardware supply chain costs cutting into margins, or merchant pushback against payment fees stalls cash generation, forcing growth to stall and the market to de-rate TOST to a legacy utility processor multiple.

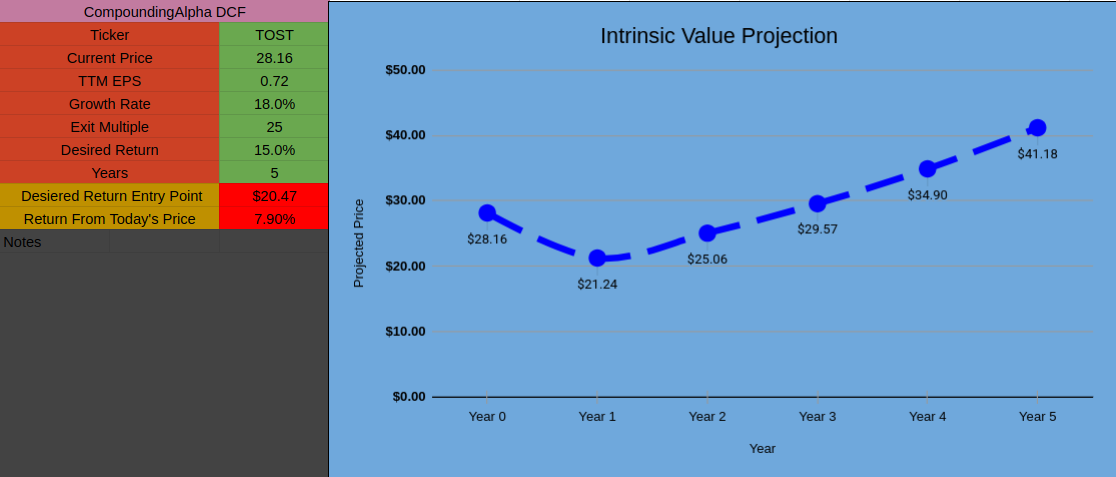

The Base Case (Steady Scaling & Market Clean-up)

The base case scenario balances healthy, structural market share expansion with realistic tech valuation compressions over time.

Growth Rate: 18.0% CAGR.

Exit Multiple: 25x SBC Adj FCF.

Desired Return Entry Point: $20.47 (indicating today’s price of $28.16 is slightly premium if your strict hurdle rate is 15.0%).

Projected 5-Year Price: $41.18.

Expected Annualized Return from Today’s Price: 7.90%.

The Thesis: The independent restaurant engine remains healthy, and Toast continues to win market share from Clover and Square. Growth normalizes slightly as the domestic SMB market matures, and the multiple settles into a standard, mature fintech range.

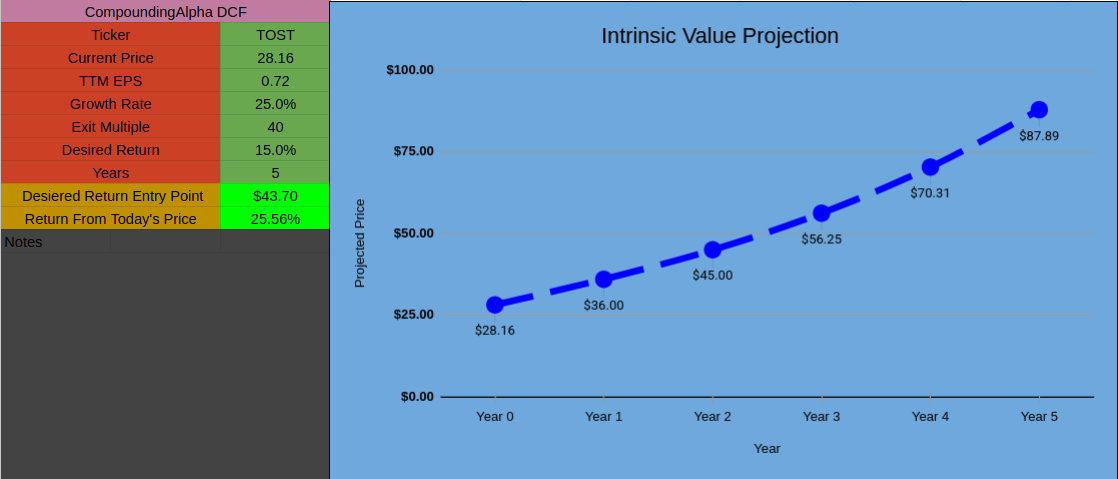

The Bull Case (High Growth & Multiple Expansion)

The bull case reflects Toast achieving full operational leverage, successfully penetrating the enterprise chain tier, and compounding its international ARR footprint.

Growth Rate: 25.0% CAGR over the next 5 years.

Exit Multiple: 40x SBC Adj FCF.

Desired Return Entry Point: $43.70 (meaning the stock is currently trading at a deep discount to its ideal buying threshold).

Projected 5-Year Price: $87.89.

Expected Annualized Return from Today’s Price: 25.56%.

The Thesis: This assumes Toast’s competitive flywheel accelerates. Upmarket enterprise wins lower overall churn, margins expand due to automated scaling tools like ToastIQ, and software add-on attachment rates remain high, easily justifying a premium SaaS multiple.

At a current market price of $28.16, the market is pricing Toast essentially right between the Base and Bull models. For an investor in search of a long term compounder, your downside is structurally protected by their $1.77 billion cash pile and aggressive share buybacks, while the upside to an $87.89 target in the Bull case represents a highly compelling risk/reward ratio.

The Final Verdict

At a current market price of $28.16, Wall Street has priced Toast almost perfectly between our Base and Bull case projections. The market has recognized the top-line growth but is still somewhat conservative regarding how quickly Toast can penetrate massive enterprise accounts or establish its footprint internationally.

For long-term investors, Toast presents a highly asymmetric risk/reward ratio. The structural downside is heavily insulated by a $1.77 billion cash fortress, zero long-term debt, and a management team actively using free cash flow to cannibalize its own shares via aggressive stock buybacks. On the flip side, the upside case to an $87.89 price target is fully supported by concrete operational metrics—namely, an escalating ARR, the rollout of proprietary AI efficiency engines, and an unshakeable platform stickiness that leaves competitors scratching for crumbs.

Toast has successfully graduated from a speculative hyper-growth experiment into an indispensable financial and operational utility. For investors looking to back a dominant market leader with an expand-on-arrival playbook, Toast remains a premium addition to the watchlist.

Check the Scorecards Want to see how my research grades out? View the 1-page fundamental breakdowns—scoring every company on Growth Potential, Profitability, Balance Sheet, Return on Capital, Shareholder Yield, Management, Moat, and Execution Certainty

Compounding Alpha Scorecard: Toast (TOST)

Toast (TOST) represents a highly dynamic cloud vertical SaaS player that has successfully captured the operating system of the restaurant industry. This scorecard maps out a business with exceptional balance sheet strength, top-tier management execution, and strong growth prospects, balanced by areas that are currently stabilizing.

Deep dives are only half the equation. Join me as we put this research into practice and build a high-conviction allocation strategy from the ground up in the CompoundingAlpha Tracking Portfolio.

Coming from outside the restaurant industry, learnt something new today!

Great article. Software is normally not my cup of tea, but this sounds very interesting indeed!