Jet Engines and AI Data Centers: The FTAI Aviation ($FTAI) Deep Dive

Traditional lessors clip coupons. FTAI built a cash-printing maintenance monopoly and is now turning retired engines into 25MW power plants for hyperscalers.

When most investors look at the commercial aviation sector, they see a graveyard of capital. It is an industry infamous for cyclicality, massive capital expenditure requirements, and razor-thin margins. The traditional playbook—buying aircraft and leasing them out for decades—yields predictable but structurally low returns.

But what if a company looked at that exact same ecosystem and found a cheat code?

What if, instead of fighting for single-digit margins on the aircraft itself, a company monopolized the single most painful bottleneck for the airline: engine maintenance downtime? And what if that same company figured out how to turn end-of-life jet engines into modular power plants for the world’s most advanced AI data centers?

Enter FTAI Aviation ($FTAI).

Currently trading around $243, FTAI is not a traditional aviation leasing company, though stock screeners might try to classify it as one. It is a highly specialized, vertically integrated industrial operating company. By pioneering a “swap, don’t shop” modular maintenance model for the CFM56 (the most ubiquitous engine in commercial aviation), FTAI has created a sticky, 35%-margin cash machine. Now, with the launch of FTAI Power to feed the insatiable electricity demands of hyperscalers, they are unlocking an entirely new Total Addressable Market.

In this CompoundingAlpha deep dive, we are going to break down the mechanics of the “Module Factory,” analyze the massive optionality of the AI power pivot, and run the DCF scenarios to see if this industrial compounder is still offering a margin of safety today.

Table of Contents

Deep dives are only half the equation. Want to see if FTAI makes the cut? Join me as we put this research into practice and build a high-conviction allocation strategy from the ground up in the CompoundingAlpha Portfolio

Check the Scorecards

Want to see how our research grades out? View our 1-page fundamental breakdowns—scoring every company on Growth Potential, Profitability, Balance Sheet, Return on Capital, Shareholder Yield, Management, Moat, and Execution Certainty

From Diversified Fund to Pure-Play Powerhouse

FTAI Aviation didn’t start as a pure-play aerospace company. It originally operated as a diversified portfolio of transportation and infrastructure assets under the management of Fortress Investment Group. The strategic pivot came as leadership realized the immense, specialized value of its aviation division—specifically its focus on the CFM56 engine, the workhorse of the global commercial fleet.

By carving out its infrastructure assets and internalizing its management, FTAI transformed into a streamlined, high-margin business focused on proprietary Maintenance, Repair, and Exchange (MRE) services and aviation leasing. Today, it commands a multi-billion dollar market cap by acquiring engines, utilizing its proprietary “Module Factory” to drastically reduce airline maintenance costs, and even converting jet engines into aeroderivative power turbines to fuel AI data centers.

The FTAI Corporate Timeline

Founding 2011

Founded as Fortress Transportation and Infrastructure Investors LLC, a diversified vehicle externally managed by an affiliate of Fortress Investment Group. The company targeted high-quality infrastructure and equipment assets globally.

Initial Public Offering May 15, 2015

The company goes public on the Nasdaq under the ticker FTAI.

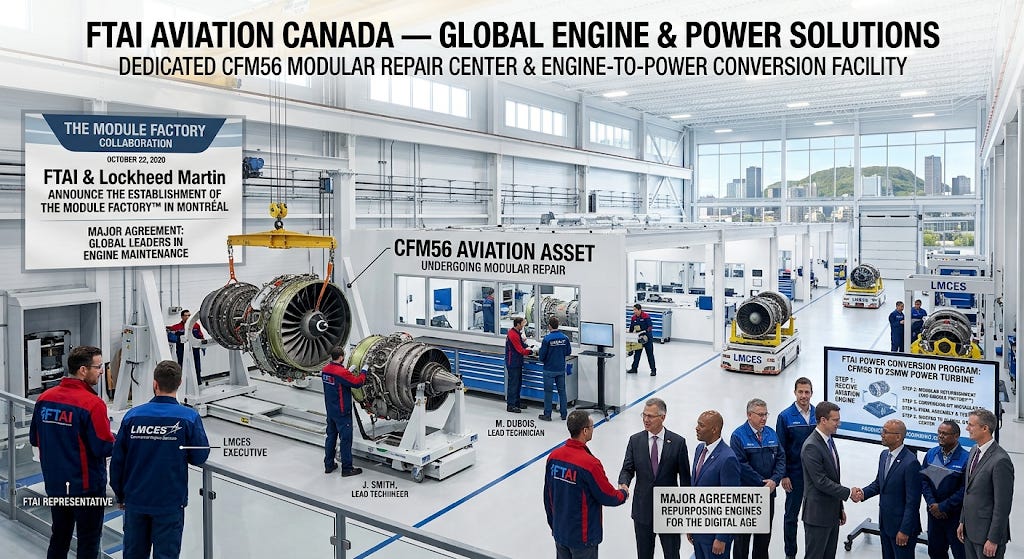

The Module Factory Collaboration October 22, 2020

FTAI announces a major agreement with Lockheed Martin Commercial Engine Solutions (LMCES) to establish The Module Factory™ in Montréal. This dedicated commercial engine maintenance center focuses on the modular repair and refurbishment of CFM56 engines.

Module Factory Operations Begin June 2021

Operations for The Module Factory officially commence. By early 2022, FTAI successfully completes or contracts over 200 module sales and swaps.

The Infrastructure Spin-Off August 1, 2022

In a massive strategic pivot to become a pure-play aviation company, FTAI successfully spins off its energy and infrastructure businesses into a separate publicly traded entity, FTAI Infrastructure Inc. (Nasdaq: FIP).

Corporate Restructuring & Renaming November 11, 2022

Following a shareholder vote, a merger agreement closes that reorganizes the company as a Cayman Islands exempted company. The parent company is officially renamed FTAI Aviation Ltd..

QuickTurn Acquisition January 2023

FTAI expands its internal maintenance capabilities by acquiring the QuickTurn Engine Center in Florida, bringing more of its CFM56 and V2500 engine repair capacity directly in-house.

Management Internalization May 28, 2024

FTAI enters a definitive agreement to terminate its management contract with Fortress Investment Group, paying a $150 million cash fee to become an internally managed company. This move creates immediate cost savings and aligns management directly with public shareholders.

Acquisition of Lockheed Martin Facility September 9, 2024

FTAI Aviation closes a $170 million acquisition of the 526,000-square-foot LMCES facility in Montréal from Lockheed Martin. The facility is rebranded as FTAI Aviation Canada, cementing FTAI’s permanent engine manufacturing and repair capabilities.

Launch of FTAI Power December 30, 2025

Pivoting to address the massive electricity demand from AI hyperscalers, the company launches FTAI Power. This new platform converts CFM56 aircraft engines into 25-megawatt aeroderivative power turbines for global data centers, with production beginning in 2026.

The Economic Engine: Inside the Module Factory

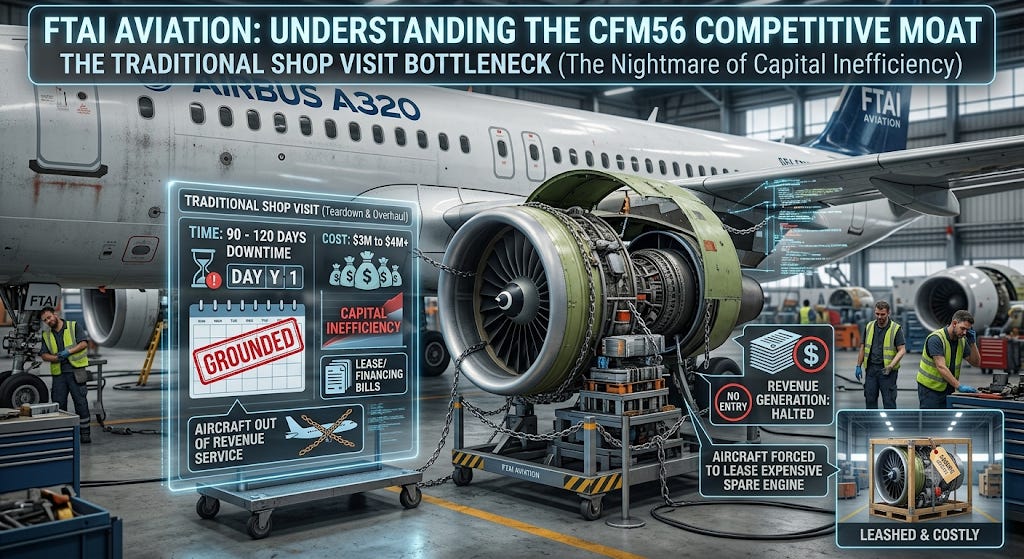

To understand FTAI Aviation’s competitive moat, you have to understand the specific bottleneck they are solving. The global narrowbody fleet relies heavily on the CFM56 engine. When these engines reach the end of their maintenance cycle, they traditionally require a full “shop visit”—a complete teardown and overhaul.

For an airline, a traditional shop visit is a nightmare of capital inefficiency. It typically costs upwards of $3 million to $4 million and takes the engine out of commission for 90 to 120 days. That is three to four months where an aircraft is either grounded (burning through lease/financing costs without generating revenue) or forced to lease an expensive spare engine.

FTAI looked at this process and essentially asked: Why overhaul the whole engine when you can just swap the broken part?

The Modular Swap Model

Instead of treating the engine as a single, monolithic asset, the Module Factory breaks the CFM56 down into its three major constituent modules:

The Fan: Supercharges airflow and produces thrust.

The Core: The high-pressure compressor and turbine where combustion occurs.

The Low-Pressure Turbine (LPT): Extracts remaining energy to drive the fan.

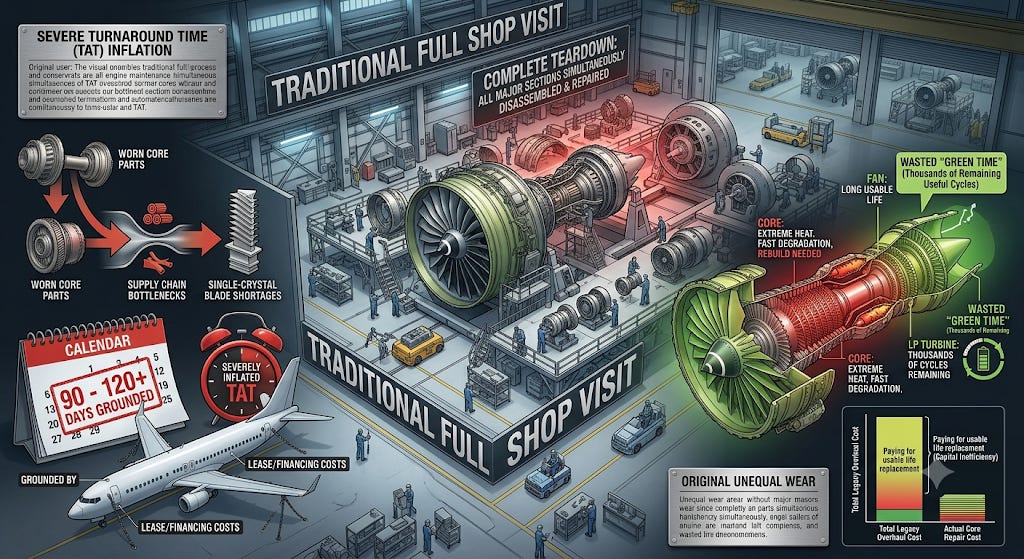

The Traditional Full Shop Visit: When an engine reaches the end of its flight-cycle limit, legacy MROs typically perform a complete teardown. Every major section is disassembled, inspected, and repaired simultaneously.

Severe Turnaround Time (TAT) Inflation: Due to aerospace supply chain bottlenecks and single-crystal turbine blade shortages, traditional heavy shop visits now routinely ground an engine for 90 to 120+ days.

Wasted “Green Time” (Remaining Useful Life): A jet engine does not wear out evenly. The Core (High-Pressure Compressor, Combustor, High-Pressure Turbine) operates under extreme heat and degrades much faster than the Low-Pressure Turbine (LPT) or the Fan. In a traditional full overhaul, an airline often pays to rebuild parts of the engine that still have thousands of cycles of safe operational life remaining.

By acquiring Lockheed Martin’s Montreal engine shop (now FTAI Aviation Canada) and the QuickTurn facility in Florida, FTAI brought the heavy maintenance in-house. They rebuild and refurbish these individual modules ahead of time and keep them “on the shelf.”

When a customer’s engine has an issue—say, the core is degraded but the fan and LPT are fine—FTAI doesn’t do a full shop visit. They simply take the engine, swap out the degraded core for a fresh one from their inventory, and send the engine back to the airline.

The Financial Impact for Airlines

The value proposition of this Maintenance, Repair, and Exchange (MRE) model is massive:

Time: Turnaround times (TAT) drop from months to as little as 5 to 10 days.

Cost: Airlines only pay for the module they swap, dramatically reducing the direct maintenance expense compared to a full overhaul.

Capital Efficiency: Airlines don’t have to carry as many spare engines on their balance sheets, and their aircraft spend more days in the air generating revenue.

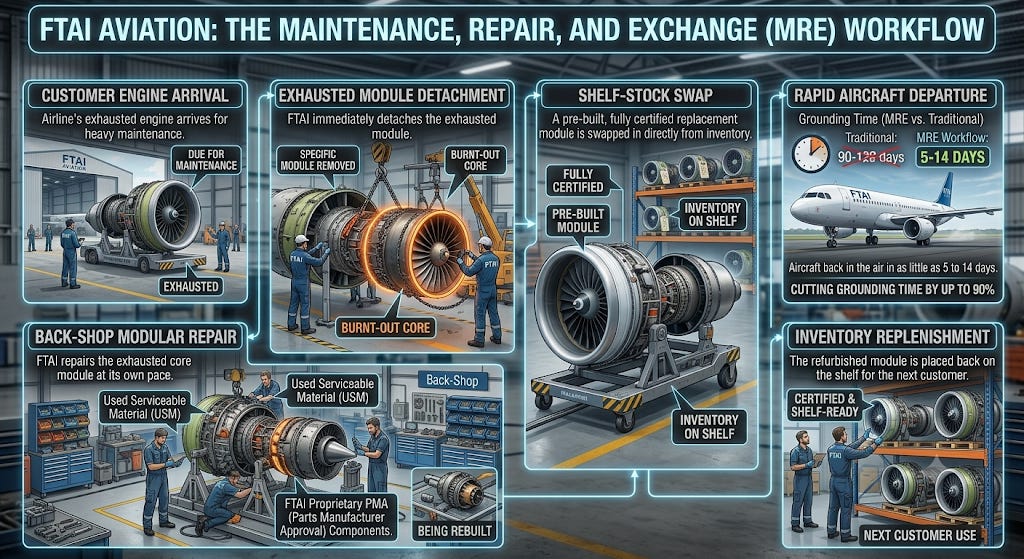

The Maintenance, Repair, and Exchange (MRE) Workflow:

When an airline's engine comes due for heavy maintenance

The engine arrives at an FTAI facility.

FTAI immediately detaches the exhausted module (e.g., the burnt-out Core).

They swap in a pre-built, fully certified replacement module directly from their shelf inventory.

The aircraft is back in the air in as little as 5 to 14 days, cutting grounding time by up to 90%.

FTAI takes the customer’s exhausted core into its back-shop, repairs it at its own pace using cost-effective Used Serviceable Material (USM) or proprietary PMA (Parts Manufacturer Approval) components, and places it back on the shelf for the next customer.

The 2026 Moat Widening: The OEM Alliance

Historically, the original equipment manufacturers (OEMs)—CFM International (a joint venture of GE Aerospace and Safran)—ran a tightly locked ecosystem of licensed repair shops to control the lucrative aftermarket. FTAI operated slightly outside this as a massive independent player.

However, in January 2026, the dynamic shifted. FTAI signed a massive multi-year materials agreement directly with CFM International. This agreement secures direct OEM replacement part supply, thrust performance upgrades, and component repair for FTAI. Rather than fighting FTAI’s growing market share, the OEM has brought them into the fold. This virtually eliminates the risk of parts shortages for the Module Factory and solidifies FTAI’s position as a permanent, OEM-backed pillar of the global aviation supply chain.

The Feeder System: Aviation Leasing

While the Module Factory (Aerospace Products segment) is the primary growth engine, FTAI’s other historical revenue pillar is Aviation Leasing. However, this isn’t a traditional, passive leasing model like those of massive lessors such as AerCap or Air Lease Corp. For FTAI, leasing is a highly strategic, symbiotic counterpart to its maintenance operations.

Historically generating a significant portion of the company’s EBITDA, the leasing segment focuses on owning commercial aircraft and standalone engines (primarily the A320ceo and 737NG families).

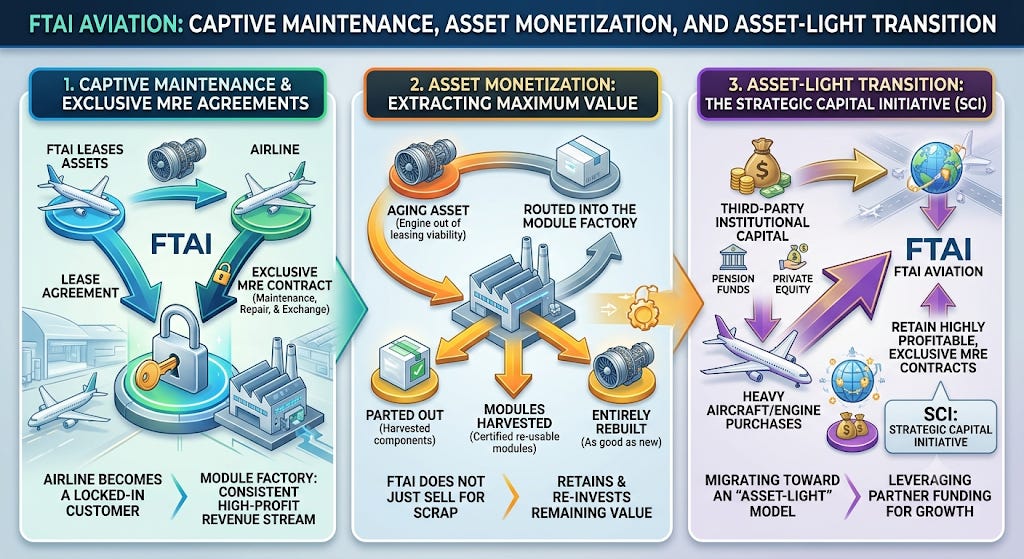

The Synergistic “Spread” Business:

Instead of relying solely on long-duration lease income, FTAI views leasing as the ultimate “feedstock” pipeline for the Module Factory.

Captive Maintenance: When FTAI leases an aircraft or engine to an airline, they frequently tie the lease to exclusive Maintenance, Repair, and Exchange (MRE) agreements. The airline becomes a locked-in customer for the Module Factory.

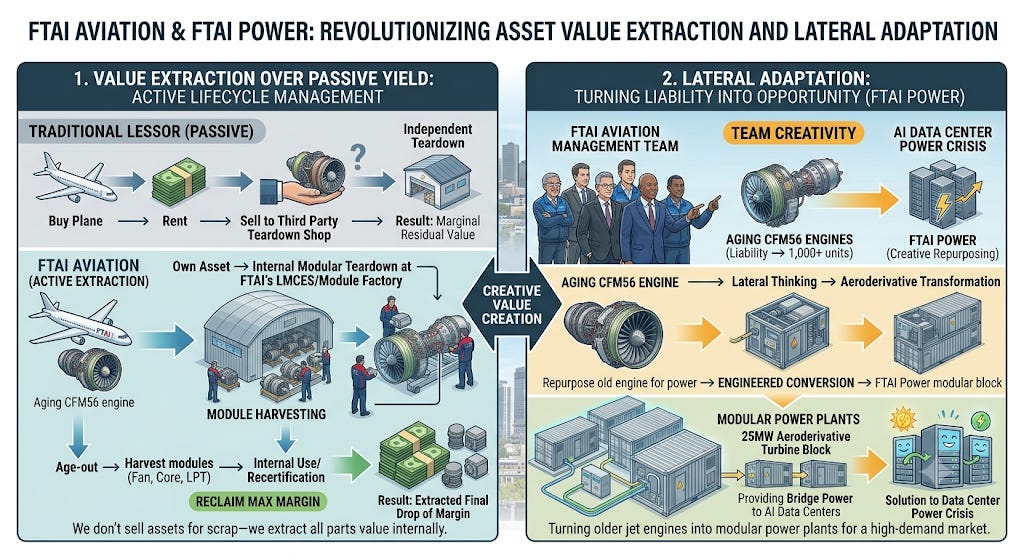

Asset Monetization: As engines age out of leasing viability, FTAI doesn’t just sell them for scrap. They route them into the Module Factory to be parted out, harvested for modules, or entirely rebuilt, extracting maximum remaining value from the asset.

The Asset-Light Transition: FTAI is actively migrating this segment toward an “asset-light” model. Through their Strategic Capital Initiative (SCI), they utilize third-party institutional capital to fund heavy aircraft purchases, while FTAI retains the highly profitable, exclusive MRE contracts.

This creates a closed-loop ecosystem where leasing drives maintenance volume, and maintenance expertise allows FTAI to underwrite lease assets more aggressively than competitors.

The New Frontier: FTAI Power (The AI Data Center Play)

If the Module Factory is the core cash cow, FTAI Power is the massive structural growth catalyst that has drastically expanded the company’s Total Addressable Market (TAM).

FTAI Power represents a bold pivot to solve one of the most critical bottlenecks in the global economy right now: the insatiable demand of Artificial Intelligence hyperscalers.

Data center developers are currently facing multi-year backlogs to secure utility-scale grid connections and heavy-frame gas turbines. FTAI realized they already owned the solution.

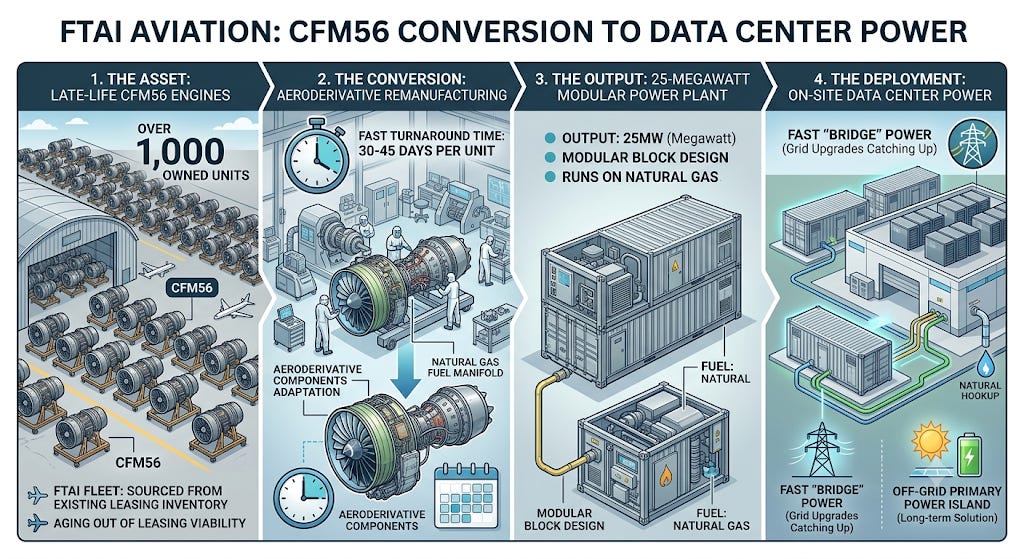

The Aeroderivative Strategy:

An “aeroderivative” turbine is a lightweight, highly efficient gas power turbine derived from an aviation jet engine. They are prized for their modularity, compact footprint, and ability to spin up rapidly.

Here is how the FTAI Power model works:

The Asset: FTAI takes late-life CFM56 engines from its existing fleet of over 1,000 owned units.

The Conversion: Leveraging its massive MRO footprint, FTAI remanufactures the CFM56 core and adapts it with aeroderivative components. This conversion process takes a fraction of the time needed to build a traditional power plant—sometimes as little as 30 to 45 days per unit.

The Output: The result is a 25-megawatt modular power plant that can run on natural gas.

The Deployment: These 25MW blocks are perfectly sized to be deployed on-site at data centers, providing fast “bridge” power while grid upgrades catch up, or serving as long-term off-grid primary power islands.

The Economic Implications:

By adapting the most widely produced commercial jet engine in history (over 22,000 built), FTAI is bypassing the supply chain constraints of traditional power generation. They anticipate producing over 100 power turbines annually once commercial production ramps up in 2026.

Crucially, FTAI is applying its Module Factory philosophy to this new sector. Rather than dispatching technicians to perform complex repairs on a broken data center turbine on-site, they can simply swap the module using their existing distribution network, maximizing uptime for mission-critical AI workloads.

The Architects: FTAI’s Management Team & Philosophy

To understand a company’s trajectory, you have to look at the people steering the ship. FTAI’s management team is particularly interesting because they successfully executed one of the hardest maneuvers in corporate finance: pivoting a diversified, externally managed financial portfolio into an internally managed, specialized operating company.

Key Executives

Joe Adams (Chairman & CEO): Adams has been at the helm since the company’s inception. A veteran of the transportation industry (formerly at Donaldson, Lufkin & Jenrette and a Managing Director at Fortress), he was also the first Executive Director of the Air Transportation Stabilization Board following 9/11. Adams is the strategic architect behind FTAI’s evolution. He recognized early on that owning a broad portfolio of planes was a low-margin commodity business, but owning the maintenance bottleneck for the world’s most popular engine was a goldmine.

David Moreno (President): Recently elevated to President after serving as Chief Operating Officer, Moreno is the execution engine behind FTAI’s strategic acquisitions and partnerships. He played a critical role in scaling the company from a leasing platform to a global engine maintenance provider.

Stacy Kuperus (Chief Operating Officer): Taking over operations from Moreno, Kuperus oversees FTAI’s global aviation footprint, specifically driving performance, efficiency, and operational excellence across the Module Factory facilities.

Nicholas McAleese (Chief Financial Officer): Promoted to CFO in March 2026 (succeeding Angela Nam), McAleese represents the next generation of FTAI leadership. Having joined the company in 2022 to build out its FP&A functions, he brings a deep, granular understanding of the company’s unit economics—vital for a business aggressively scaling two distinct hardware divisions.

Management’s Core Philosophies

If you study FTAI’s capital allocation and operational decisions, a few core philosophies clearly emerge:

Skin in the Game (Internalization): In May 2024, management paid $150 million to terminate their external management contract with Fortress Investment Group. This was a massive signal to the market. By internalizing management, Adams and his team eliminated external fee drag and aligned their compensation directly with shareholder value creation.

Asset-Light Capital Allocation: Aircraft are expensive, depreciating assets. FTAI’s management dislikes tying up balance sheet capital in low-yield hardware. Through their Strategic Capital Initiative (SCI), they utilize third-party institutional capital to fund the purchase of aircraft. FTAI manages the asset, skims a fee, and most importantly, locks in the exclusive, high-margin maintenance contracts for the Module Factory.

Value Extraction Over Passive Yield: Traditional lessors buy a plane, rent it out, and hope to sell it for a decent residual value. FTAI views every asset as a sum of its parts. If a leased engine is nearing the end of its life, they don’t sell it to a teardown shop—they are the teardown shop. They harvest the modules and extract the final drop of margin.

Lateral Adaptation: The creation of FTAI Power is the ultimate expression of this team’s creativity. Instead of viewing aging CFM56 engines as a liability, they looked laterally at the macroeconomic landscape, saw the AI data center power crisis, and engineered a way to turn old jet engines into modular power plants.